What if I told you we’ve got a shot at grabbing 2 cheap funds that kick out huge dividends—I’m talking 7.5% and higher—and those payouts are tax-free too?

What I’m talking about might be the last bargain available to us in this (overheated) stock market. Stocks’ roll higher since the Liberation Day tariffs were put on hold has meant fewer income opportunities from S&P 500 names (as yields and share prices move in opposite directions).

That’s added even more appeal to the tax-free dividends (two, in particular) we’re going to talk about below. They deal in municipal bonds, which are issued by state and local governments to fund infrastructure projects. “Munis” also tend to offer healthy yields, typically 200 basis points above those on a 10-year Treasury note.

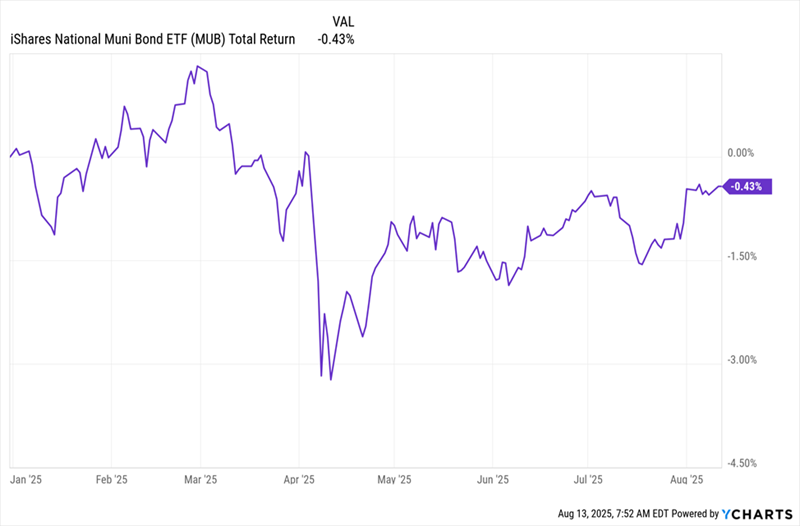

Our opportunity starts with munis’ performance. As I write this, the S&P 500 has returned around 10% this year. But look at munis’ benchmark ETF, the iShares National Muni Bond ETF (MUB), and you’ll quickly see that it’s flat.

Munis Rebound After Selling Off (But They’re Still Cheap)

Sure, the April “tariff tantrum” was a better time to buy munis (and everything else!). But our buy window is NOT closed, due to the lag that still exists between munis and stocks.

The reason for this gap is simple: Blue chips—or better still, the high-yielding closed-end funds (CEFs) that hold them—are great for long-term growth. But some of us need cash now—and this is where muni bonds come in.

Trouble is, individual munis are tough for everyday investors like you and me to access, plus MUB only yields around 3% today. By purchasing our munis through a CEF, though, we can net a much bigger payout, as we’ll see shortly.

Moreover, we demand a human manager for our munis because these pros get tipped off when the best new bonds are issued. Buying through an ETF means we don’t get that personal (and profitable!) touch.

For these reasons, we go with CEFs for our muni-bond buys. Before we go further, though, let’s put that muni-bond tax break in perspective, because it’ll almost certainly mean a lot to you.

According to Eaton Vance’s tax-equivalent yield calculator, for a California resident in the top tax bracket, a 5%-yielding muni bond is worth an 8.2% yield on, say, a US Treasury, or 10% from other debt instruments, like corporate bonds.

And here’s the thing: Even if you don’t pay high taxes, you can still buy muni-bond CEFs now that they’re being overlooked, then sell when stocks get volatile and investors hunt for alternatives. While you wait, you’ll collect a big, tax-free dividend.

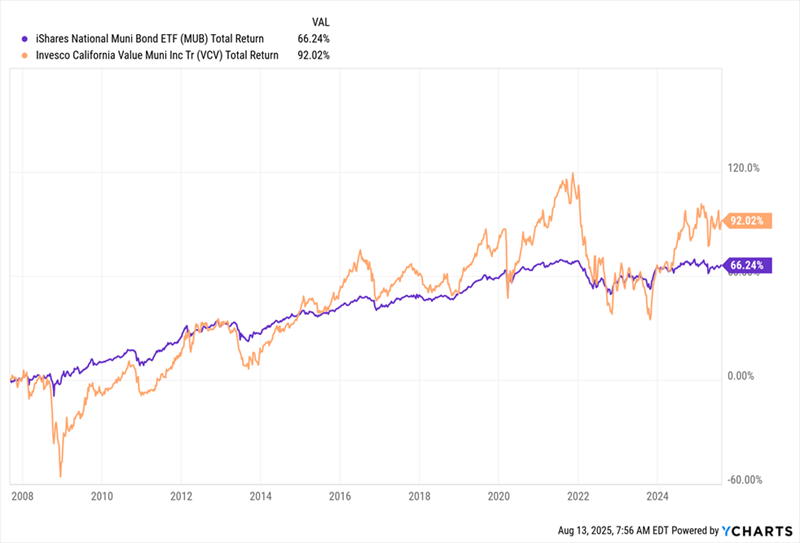

Take, for example, a CEF called the Invesco California Value Municipal Income Trust (VCV), which crushes MUB on the yield front, thanks to its 7.5% yield (and that’s before the tax break). Moreover, VCV (in orange below) has crushed MUB (in purple) since the muni benchmark’s inception.

VCV Beats MUB Over the Long Haul

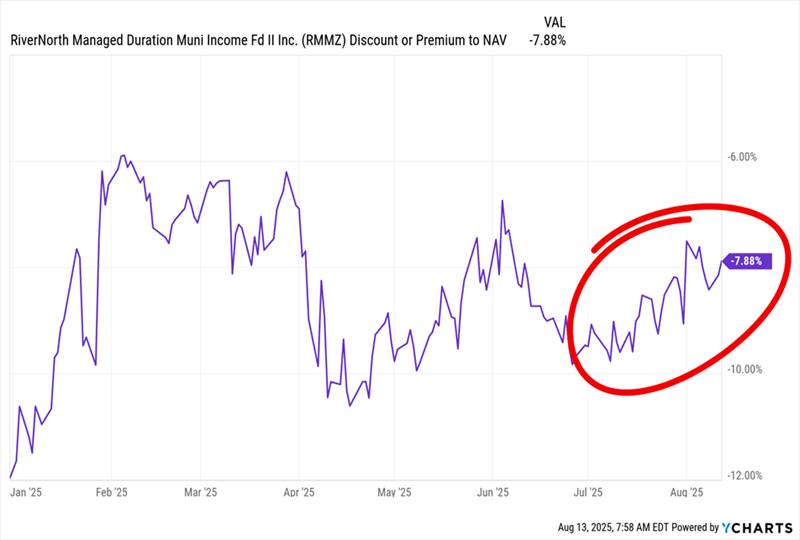

Moreover, with muni-bond CEFs, you don’t have to limit yourself to state-specific funds like VCV. For a national choice with a bigger dividend, consider the 8%-yielding RiverNorth Managed Duration Municipal Income Fund II (RMMZ).

That fund’s payout tops those of both MUB and VCV. Plus, this fund’s discount is in the “sweet spot”: still wide, at 7.9%, but trending narrower—putting upward pressure on the share price.

A Discount With the Momentum We Love

That discount means RMMZ trades for less than its portfolio is worth. And the chart above tells us that this deal isn’t likely to last. See how the fund’s discount has been narrowing after widening earlier this summer? That’s because investors have been anticipating lower interest rates.

Those rate cuts haven’t landed yet, but when they do, RMMZ will benefit because newer munis will be issued tied to those lower rates. That will make the fund’s portfolio of already-issued (and higher-yielding) munis more valuable. And that is likely to drive more interest from investors, narrowing RMMZ’s discount even more.

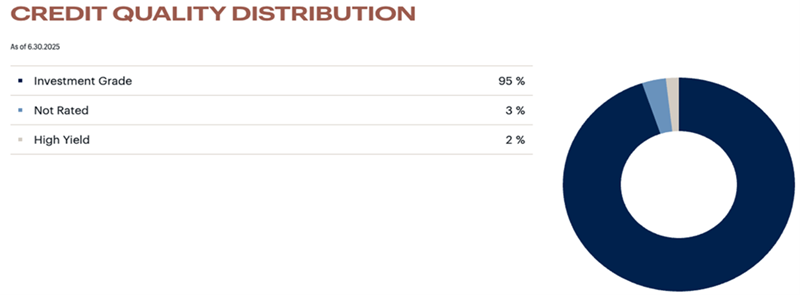

And for more safety, consider this:

Source: RiverNorth

As you can see, the fund’s portfolio is almost entirely investment grade. While a lot of CEFs reach into speculative high-yield bonds, RMMZ doesn’t. So you can sleep well at night as you collect your dividends—and wait for rate cuts to draw more attention to tax-free muni-bond CEFs, including this well-run fund.

What Beats a Reliable 8% Muni Dividend? A 10.2% MONTHLY Payer!

These two tax-free muni-bond CEFs are, hands-down, terrific choices to anchor your income portfolio.

But they’re just the start. Because relying on just one asset class—even if it is a “low-drama” one like tax-free muni bonds—is a recipe for disappointing performance (or worse!).

That’s why I urge all investors to go further, and my 10.2% Monthly Dividend Portfolio is a simple, powerful way to do so. As the name says, it’s throwing off massive dividend—10.2%!—and every single fund inside pays you every month.

That makes this potent collection of income plays perfect for covering bills or reinvesting for faster compounding.

Even better, these funds are unusually cheap now. That gives you an excellent shot at price upside as their discounts vanish. And you’ll be well-paid (every month!) while you wait.

Don’t miss out—this could be the best investment move you make all year.