There’s an obvious reason why we love closed-end funds (CEFs): the dividends!

CEFs’ payouts average around 7% as I write this, and there are plenty paying well into the double digits. One fund we’ll touch on below, for example, yields more than 16%. A payout like that gets you $2,000 a month in dividends on just $150,000 invested.

But, as we often discuss in my CEF Insider service, when picking CEFs, we always need to look past those big yields.

We also need to examine the discount to net asset value (NAV, or the value of the fund’s portfolio) because buying a CEF at an unusually wide discount can net us strong price upside as that discount bounces back to normal, pulling the price up with it. Conversely, buying at a premium can tie a lead weight to the value of our investment.

And there’s another aspect of CEFs it pays to keep a close eye on—two, actually: whether a CEF regularly conducts rights offerings or tender offers.

We’ll break down the jargon in a second. First, to get a clear picture, we need to bear in mind that CEFs are, as the name implies, closed (or almost closed, as we’ll see below). That means your ownership stake can’t be diluted by management issuing more shares after the fund’s IPO. This is a problem with other high-yield assets, like business-development corporations (BDCs).

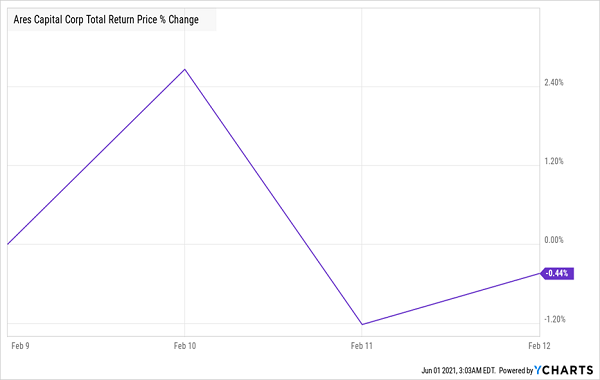

Ares’ Share Issuance Depresses the Stock

When Ares Capital Corporation (ARCC) issued new shares in February, the stock price immediately fell. While this wasn’t as big of a drop as some BDCs suffer when they issue new shares, it’s annoying if you happen to buy before the issuance. CEFs don’t have that problem.

Tender Offers Can Boost Your Shares Overnight

While CEFs cannot just issue more shares to increase the share count and dilute your stake, they can tweak the amount of shares available in two ways. One is through a tender offer and the other is through a rights offering.

Let’s start with a tender offer, because it’s particularly nice for us. An example of a tender offer would be if a fund announces on, say, February 22 that it will buy up to 10% of the shares currently owned by investors at a discount of 2% to the fund’s NAV. So if the fund is trading at $10, management would buy back your shares at $9.98, if you wish to sell.

Why would you sell at a discount? Let’s say the fund is trading at a 12% discount to NAV, so its current market price is $8.80. That means you can offload your shares at a price much higher than the current market price instead of waiting for the fund’s discount to disappear on its own.

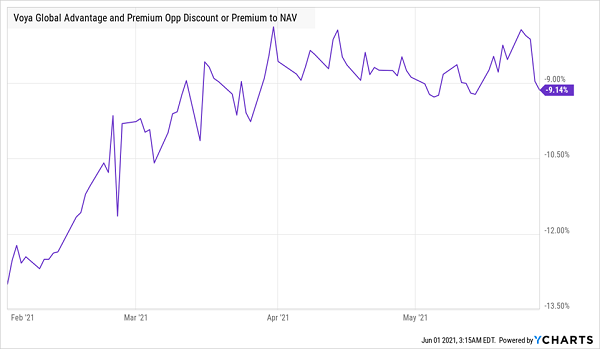

I didn’t pull this scenario out of thin air, by the way. The Voya Global Advantage and Premium Opportunities Fund (IGA) did exactly this in February 2021. Here’s what happened to its discount:

Tender Offer Narrows IGA’s Discount—and Boosts Its Price

As the discount narrowed, it pulled IGA’s share price up 7.7%, to around $9.60, closer to the value of the tender offer. Management, then, can hold on to those shares, thus lowering the total number of shares outstanding and increasing the size of each shareholder’s stake.

So even if you didn’t sell your shares to management during this offer, you still saw some nice gains thanks to those who did—and you could comfortably hold your CEF, knowing management would give you windows of opportunity to sell back your shares if you wanted to (Voya and many other CEF managers make these offers pretty regularly).

Be Wary of Rights Offerings

While tender offers shrink the total amount of shares, rights offerings do the opposite and expand the total number of shares, thereby reducing each investor’s stake in the fund. This is why CEFs are not, technically, fully closed; they can introduce new shares through rights offerings, but only to current investors. And we do need to be wary here, because management has a stake in a rights offering, as increasing the number of shares results in more assets management controls—and thus can charge fees on.

While there are some cases where a rights offering makes sense (say, with a fund that has been massively outperforming and is focused on an asset class that is hard to buy otherwise), in most cases they’re a poor deal for investors because they weigh down the share price.

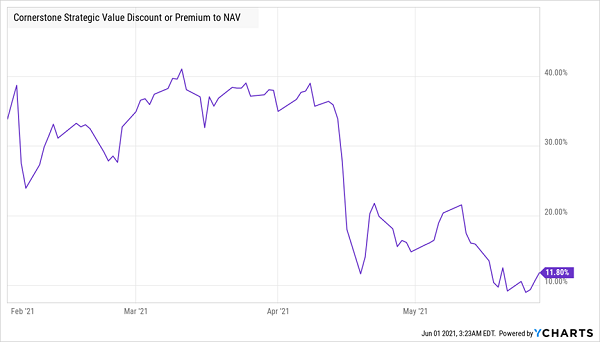

Let’s take, for instance, the Cornerstone Strategic Value Fund (CLM), the 16% yielder I mentioned off the top. CLM completed a rights offering in May 2021, in which it gave shareholders the opportunity to buy additional, new shares in the fund at a 7% or higher premium to its NAV—that’s right, the new shares weren’t sold at a discount. That offering closed on April 16, and you can see what happened to the fund’s premium when it did.

Rights Offering Slashes CLM’s Premium …

The ability to get new shares at a 7% premium was a steal at a time when the fund was trading at a near-40% premium. But it also meant the market price of your shares fell in the interim, as they declined to meet the offering price:

… And Takes Down the Share Price

Funds that frequently do rights offerings are often at a risk of having their market prices fall as a result, so when picking CEFs, it’s a good idea to check their history before you buy.

Alert: These 5 CEFs (Yielding 7.3%!) Are the Best Bargains on the Market Today

CEFs are, hands down, your best option today, as the market drifts higher, making S&P 500 stocks pricey and those same stocks’ dividend yields almost nonexistent!

CEF-land is a different place, though. Here, most funds trade at discounts, some ridiculously so, like the 5 CEFs I’ll tell you about right here. Each of these 5 funds trades at a completely ridiculous discount to NAV, setting us up for nice 20%+ price upside in the next 12 months.

Best of all, they yield 7.3% on average.

In other words, based on my forecasts, a $100K investment in these funds today could hand you $20,000 in price gains by this time in 2022, plus another $7,300 in dividends!

Full details are waiting for you right now. Go here and I’ll share everything I have on these 5 dividend machines with you—names, tickers, buy-under prices, full dividend histories and more.