Look, rate cuts are only weeks away now—likely starting in September. And there’s one terrific way to tap them: high-yielding municipal bonds!

I know most folks think “munis”—issued by state and local governments to fund infrastructure projects—are boring.

It is, frankly, a ridiculous opinion. Tell me what’s “boring” about an investment that kicks out a 7.7% tax-free dividend!

To be sure, there are a couple quibbles you might have with munis.

For one, they’re tough to buy individually. But that’s really not a problem: ETFs offer one way in, but a much better way—and the only road to 7.7%+ dividends—is through closed-end funds (CEFs) like the three we’ll break down in just a second. The other quibble? Muni-bond payouts, while steady, rarely seem to grow that much.

Until now.

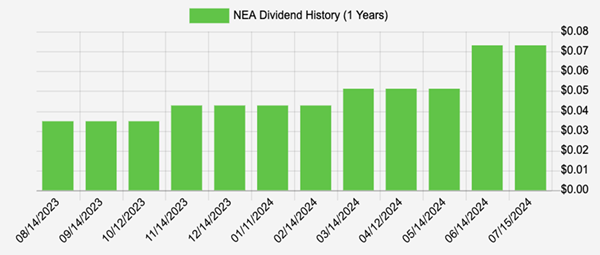

7.7% Payer’s Dividend Creeps Higher—Then Surges

Source: Income Calendar

That’s the one-year dividend chart of the Nuveen AMT-Free Quality Municipal Bond Fund (NEA), a holding in my Contrarian Income Report service. It’s the payer of that 7.7%-yield figure I’ve been talking about up to now.

Truth is, that 7.7% yield is actually pretty fresh: It jumped to that level thanks to the monstrous 37% payout hike management recently brought in (and you can see on the right side of the chart above). Before that, a yield in the “mid-fives” was more the norm for NEA, and other tax-advantaged muni-bond CEFs.

NEA wasn’t alone in its payout hike. Many other muni-bond CEFs dropped double-digit increases in June—an absolute earthquake in muni-bond land. And bear in mind that NEA’s 7.7% payout is before the fund’s tax advantage comes into play.

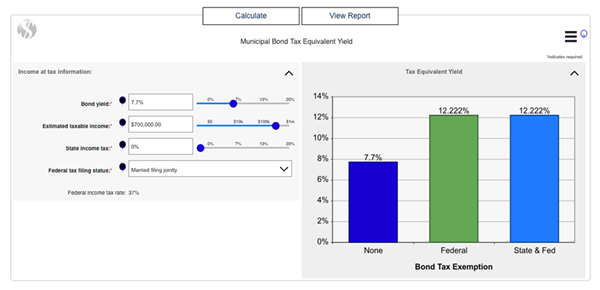

With the big jump in yield we’ve seen at NEA and friends, those yields are now in the double digits for those in the top tax bracket:

Source: Raymond James taxable-equivalent yield calculator

A 12.2% taxable-equivalent yield. Twelve. Point. Two. Percent!

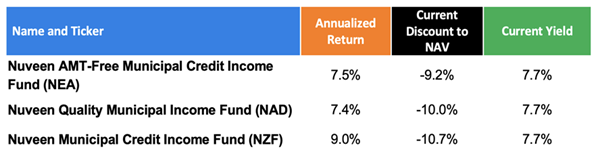

NEA’s stability and high (tax-free) income is why we hold the fund and its “cousins,” the Nuveen Quality Municipal Income Fund (NAD) and Nuveen Municipal Credit Income Fund (NZF), in Contrarian Income Report.

(Well-connected Nuveen is our go-to manager when it comes to munis, as the firm often gets the first call when new issues roll out—something ETFs can’t match.)

This trio has done just what we asked them to, “returning their yields” and then some since we bought. Our first pickup was NZF in April 2023, when it yielded 4.3%. We followed up with NAD and NEA in October 2023, when they yielded 5.8% each.

Here’s where things stand today:

CEF Discounts, Fed Will Drive Future Gains

But that’s the past. What can we expect from our muni-bond CEFs from here? Well, we’ve got two things working in our favor:

- Our CEFs’ discounts to net asset value (NAV, or the value of their underlying portfolios, which we can see in the table above), and …

- The Federal Reserve.

Let’s take those discounts first.

CEFs, unlike ETFs and mutual funds, tend to have more or less fixed share counts for their entire lives. As a result, they often trade at different levels in relation to NAV—and often at discounts.

That’s certainly the case with our three muni-bond plays, whose discounts all sit right around 10% as I write this—so we’re essentially buying for 90 cents on the dollar!

It gets better—and this is where the Fed comes in.

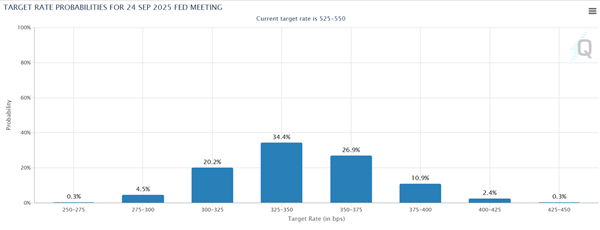

Truth is, inflation is coming off the boil, with the latest personal consumption index (PCE), the Fed’s favorite inflation gauge, coming in at just 2.5% in June down from 2.6% in May. That pretty much locks in a September rate cut, and futures traders agree, setting 81% odds of a quarter-point cut at the Fed’s September 18 meeting.

Heck, some even see a chance of a half-point cut! And the majority now see six (or more) “quarter-pointers” in the bag by September 2025:

Source: CME Group

That’s great for bonds (including munis). As rates fall, bond prices will rally. That’ll be a tailwind for all bond CEFs. And even if by some weird circumstance the Fed holds off a bit longer, that’s fine. The longer they wait, the faster rates will fall.

There’s only one thing that’s keeping me from pounding the table on this trio today: Following the announcement of their big payout hikes, all three have seen their prices bounce:

Dividend Hikes Send Muni-Bond CEFs Higher

I still expect this trio to “return their dividends” going forward, but if you want to add more price upside to that return (and we do!), hold out just a bit longer and be ready to buy these high-yielding payouts on the next dip.

Exclusive: How to Build a Monthly Income Stream With Yields Up to 10.5%

Many folks don’t realize it, but many CEFs, including NEA, NAD and NZF, pay dividends monthly rather than quarterly. Try finding that in ETFs and regular stocks! It’s virtually impossible.

I don’t know about you, but I’d much rather get cash in hand every 30 (or 31) days than have to wait three long months. It matches up with our monthly bills (particularly good for retirees) and lets us reinvest our payouts faster.

Even better, thanks to CEFs, you can get monthly payouts and high yields! With my top 3 monthly payers to buy now, you can pocket payouts up to 10.5%.