You and I both know there’s a problem with the sugar high the stock market’s been on. Does it mean we should dump some of our beloved dividend stocks and try to buy them back at lower prices?

We’ll talk income strategies and market timing in a minute. First, let’s talk about these concerning behaviors exhibited by America’s odd couple, Mr. and Mrs. Market.

First up, we know a correction is coming. When a group of folks on a Reddit message board can drive one stock—GameStop (GME)—up 1,700%+ in a month, you know the market has become a bit unhinged.

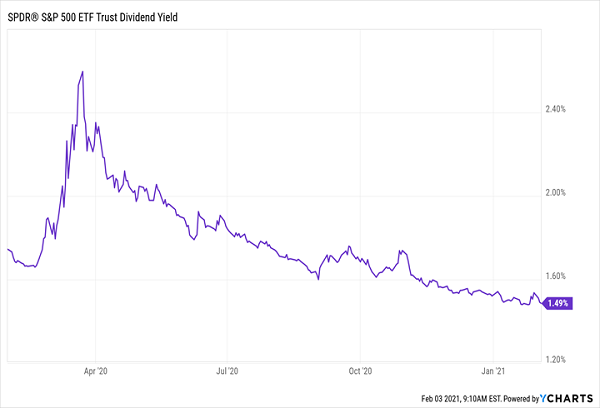

But if we sell now and sit in cash, we’ll be stuck watching inflation erode our nest egg. And if we go ahead and add to our positions in S&P 500 stocks today, we’ll be buying at a lower dividend yield than we would have just a few months ago:

The (Dividend) Curve Gets Flattened

This is where the ETF industry comes in to “help,” peddling low-fee “high yield” funds. Don’t take the bait!

Let me show you why dividend ETFs are generally a bad deal by breaking down two you may have heard about. Then I’ll show you two much better options that get you dividends 2X to 3X bigger: I’m talking 6%+ yields here, plus strong price upside, too.

The best part is that these alternatives—an often-snubbed asset class called closed-end funds (CEFs)—hold the same stocks as their ETF cousins, and many of the same stocks you likely hold in your own portfolio now. So we won’t be wandering into obscure-asset land to get these hefty payouts.

Sell These 2 “High-Dividend” ETFs Now …

The first “high dividend” ETF we’re going to look at is the Vanguard High-Dividend ETF (VYM).

With a name like that, you’re probably expecting at least a 5% yield, right? Well, VYM’s actual yield is … wait for it … 3.1%.

Sure, that’s better than the go-to S&P 500 index fund, the SPDR S&P 500 ETF Trust (SPY) and its pathetic 1.5% payout. And VYM holds the same blue-chip names as SPY, with Johnson & Johnson (JNJ), Coca-Cola (KO) and Verizon Communications (VZ) filling out its top-10 holdings.

But if you’re looking for a livable income stream, keep looking. To get $40,000 in yearly dividends (enough for many folks pay their bills with dividends alone—and avoid selling into the next crash), you’d need a nest egg of $1.2 million!

That’s a lot of saving—and let’s be honest, most of us will never get there.

Other so-called “dividend” ETFs aren’t much better. Like the ProShares S&P 500 Dividend Aristocrats ETF (NOBL), which holds the 66 S&P 500 firms that have raised their dividends for 25 years or more. Dividend favorites like AT&T (T), Procter & Gamble (PG) and McDonald’s (MCD) all make the list.

While that all sounds great, this ETF’s yield is worse than VYM’s, at just 2.1%. So you’ll need NOBL’s quarterly payout to grow steadily for many years to build up the yield on a buy made today to, say, 6% or more.

There’s just no reason to do that when you can start with a 7.4% average payout today with the two CEFs below.

… And Look to These 2 “Real” High-Yields Fund Instead

The thing I love about CEFs is that, unlike ETFs, which really only pay us through price gains (due to their meager dividends), CEFs have three ways to fill our pockets:

- Big dividends: 6%+ yields are common in CEF-land, and one of the funds I’ll reveal in a second pays a lot more. That means you can save up a much smaller nest egg than $1.2 mil to get that $40,000 dividend stream we mentioned a second ago.

- Discounts: Unlike with ETFs, CEFs can, and do, trade for less than the value of their portfolios. This measure, called the discount to net asset value (NAV) is available on any fund screener and makes our play simple: buy when a discount is unusually wide, then ride the shrinking discount to gains as it reverts to normal.

- Price appreciation: As with ETFs, a CEF’s market price will, of course, rise as the value of its portfolio goes up.

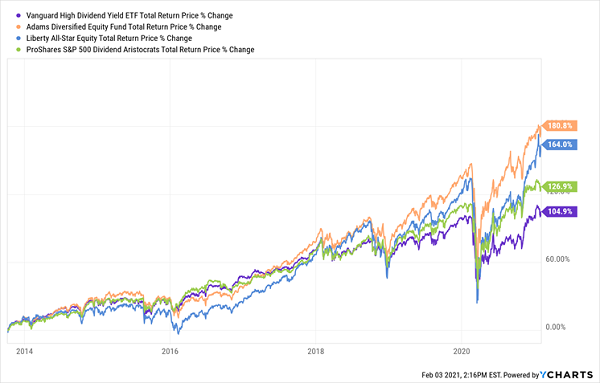

To see these three points in action, let’s look at two CEFs—the Liberty All-Star Equity Fund (USA) and the Adams Diversified Equity Fund (ADX)—that hold many of the same stocks as VYM and NOBL, but otherwise couldn’t be more different.

Let’s start with performance.

As you can see, our two CEFs (in orange and blue below) have crushed the two ETFs on a total-return basis (including dividends) in the last 10 years. And both have bounced back higher since the March 2020 crash:

High-Yield CEFs Roll Over the ETF Competition

Those gains were driven by solid performances from their portfolios and, in USA’s case, a shrinking discount. Five years ago, the fund traded at a 14% markdown that’s been whittled down to 3% as I write this.

And, yes, both hold many of the same stocks you’ll find in VYM and NOBL. ADX’s largest holdings include Microsoft (MSFT), Apple (AAPL), Amazon.com (AMZN) and Alphabet (GOOGL). USA gives us a similar look, with names like Visa (V), UnitedHealth (UNH) and PayPal (PYPL) among its largest positions.

Now let’s talk dividends.

Both funds do have somewhat unconventional dividend policies—but these strategies work in your favor because they help both funds ignite their NAVs and, by extension, their market prices.

Let’s start with ADX, which pays most of its dividend as a year-end special payout. That means your dividend does fluctuate a bit from year to year, but management is committed to paying you a 6% minimum yield every year, and it usually pays more than that, including in 2020, when its year-end distribution brought its yield in at 6.8%, as of the date of its November announcement. (Note that ADX yields 5.8% now, as its price has risen in the rebound.)

This flexibility pays off for us because it lets ADX free up cash for management to go bargain hunting when it sees an opportunity, which has helped drive that strong total return we saw earlier.

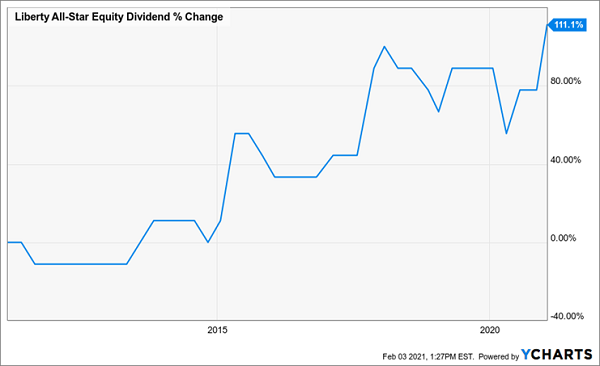

USA’s dividend strategy is similar: the fund says that it will pay 10% of its NAV per year as dividends. And as you can see below, that policy has resulted in a steadily growing payout for USA unitholders:

USA’s Dividend Doubles

Finally, let’s debunk the other knock on CEFs—that their fees are too high.

It’s true that these two CEFs charge more than their ETF cousins, but their fees are still lower than those you’d pay on most mutual funds: USA’s fees are 0.99% of assets, while ADX’s are 0.65%.

(NOBL, for its part, charges 0.35%, which is absurd for a fund that automatically tracks just 66 companies! VYM’s fee is 0.06% of assets.)

But every return chart I show you is net of fees. And if we can get performance that outruns comparable ETFs and pays us 6% to 10% dividends, we’re happy to pay a bit more for it!

Get $3,330 a Month—Every Month—With This 8%-Paying Portfolio

The big dividends you get from ADX and USA could be a boon for your retirement portfolio, but we can go further still, grabbing ourselves an even higher dividend (an 8% yield, to be exact) that comes your way every month!

It’s not a pipe dream: my 8% Monthly Dividend Portfolio gives you just that.

A payout that big gets you $40,000 in dividend income every year, broken out into nice, predictable $3,300-a-month installments (give or take a few bucks).

Do whatever you want with it: pay your bills as they come in. Or, if you don’t need all the income right away, reinvest it and grow your nest egg (and income stream!) even more.

Full details are waiting for you now. Go here and I’ll give you a tour of my 8% Monthly Dividend Portfolio, including the methodology I use to pick the safest, highest-yielding monthly paying investments, the tickers to buy now and everything else you need to get started.