I just read one of the best articles on personal finance I’ve ever seen.

The piece, titled “I Saved Too Much for Retirement: What I Wish I’d Done Instead,” by Martin Dasko and published on Yahoo Finance, warns of a very real danger: “If you save too much for retirement,” Dasko writes, “you could find yourself missing out on your best years, and even end up with a higher tax liability when you stop working.”

Of course, the article also says that it’s better to overprepare financially and warns of how difficult it is to retire on your own (“hire a professional!” the implication goes). But it admits something few financial planners want to: you could really be shooting yourself in the foot if you save too much.

Step 1: Decide Your Yearly Retirement Spending (and Forget the 4% Rule)

The first way to avoid this risk is to identify how much money you need to retire. Most financial planners ask you to multiply how much you spend per year by 25 to get to the right figure. Plan to spend $50,000 annually? You’ll need to save $1.25 million. Want to spend $100,000? Double that.

The reason for this number is that financial planners think you can only safely take out 4% of your portfolio annually without running out of money. This is based on the conclusion of a study that was done in the 1990s—a conclusion the author himself has since disowned.

Truth is, the actual amount you can take out annually depends on what is in your portfolio and how you manage it. If you day trade, then yes, anything above 4% and you’ll run out of money—quite likely below that, too. And if you pay high fees to a financial planner, again, above 4% and you’ll probably run out, as well.

However, if you invest in often-overlooked income alternatives like the closed-end funds (CEFs) I’m about to show you, things can change a lot. Take a look at this chart to see what I mean:

Sticking with $50,000 in yearly spending and our financial planners’ rule of multiplying our forecast retirement spending by 25, you can see by looking at the red line how fetching a higher return on your investment means you can retire on a smaller nest egg.

If we go from a 4% to a 5% return, for example, we need to save $250,000 less, while going up to an 8% return gets us down from a $1.25-million-dollar nest egg to just $625,000, a 50% drop! That also means years, possibly even decades, less time working in an office.

To be sure, financial freedom becomes a lot easier to get when we can generate an 8% return on our nest egg, rather than 4%. So why doesn’t everyone assume 8%? Because, as dozens of financial planners have said to me over the years, it’s impossible.

But that’s just wrong: it isn’t just possible, but thousands of investors are quietly doing it right now.

Converting “Paper Gains” to Hard, Spendable Cash

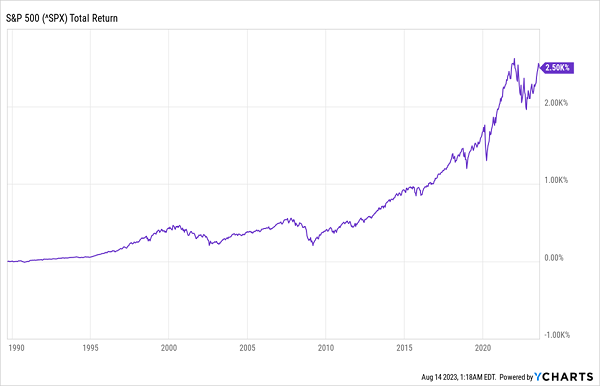

One reason why I think you can count on an 8% return is history. Let’s say you wanted to retire back in 2002, a little more than 20 years ago. Since then, we’ve seen the dot-com collapse, the War on Terror, a few years of higher interest rates leading into the collapse of the housing bubble and the 2008/’09 financial crisis, then years of near-zero interest rates, the pandemic, a spike in inflation and the Ukraine War.

No matter: stocks did what they always do over the long run: they rose:

The Power of Patience

Over the long term (we’re talking 100 years here), the US stock market as measured by the S&P index (this used to be less than 500, but the S&P 500 would be the measuring stick from 1957 onward) has given a 9.4% annualized return. That is a lot—and it also means that if you could get 8% of that in cash, you would have had a secure 8% income stream in perpetuity, plus a bit extra.

However, S&P 500 index funds yield less than 2%, so you have what financial professionals call a liquidity problem: you have a 9.4% return but not a 9.4% income stream. The two aren’t the same; you need something to turn the overall return into income—and to do so without killing the long-term return.

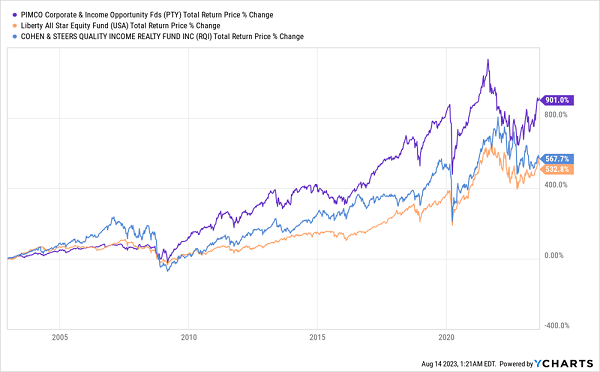

Enter CEFs, many of which are good substitutions for popular index funds. The Liberty All-Star Equity Fund (USA), for example, is a close proxy to the S&P 500; the Cohen & Steers Quality Income Realty Fund (RQI), strongly resembles the S&P United States REIT Index, and the PIMCO Corporate & Income Opportunity Fund (PTY), is a good stand-in for the US corporate bond market.

Big Gains Over the Long Term

Over the last decade these funds have booked strong returns, mostly through dividends. They focus on giving you as much of their return as possible in payouts, which is why they yield over 8% each, with PTY yielding the most at exactly 10%, while USA’s 9.9% yield isn’t far behind, and RQI’s 8.2% yield is also above our 8% threshold.

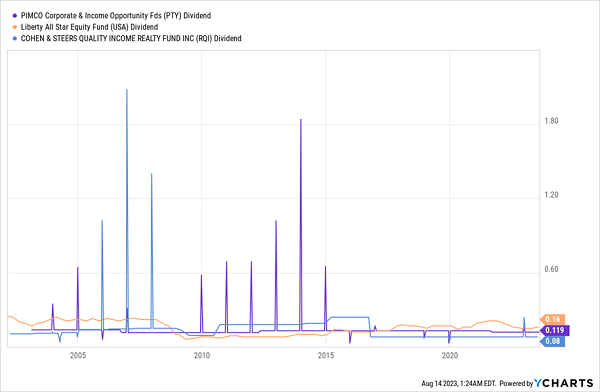

A Long History of Payouts

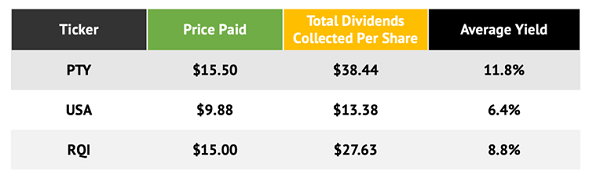

These funds’ focus on “dividend conversion” is also why their payouts tend to fluctuate a bit, and they tend to rely on special dividends to “catch up” on any year’s portfolio gains. Many dividend investors would see this as a weakness, but it’s really a strength, as their managers work to get us as much income as possible. Let’s look at how these payouts played out for an investor who bought these funds back in 2002.

The Power of CEF Income

In other words, an investor who bought these three funds in 2002 would have earned an average 9% income stream for 21 years.

Note that this is 1% more than the 8% I’m calling for now, and that’s for someone who invested through the dot-com bust, the burst housing bubble, the greatest economic recession in nearly 100 years, the largest global pandemic in 100 years, and many more market catastrophes.

No matter. The key takeaway here is that none of those (either on their own or in combination) would have forced our hypothetical CEF investors to return to work—for more than two decades.

3 Big 9.5% Dividends Set to Crush “Spendy” PTY, USA and RQI

The problem with these 3 funds is that they’re all priced at premiums to net asset value (NAV, or the value of their underlying portfolios) much of the time. Heck, PTY’s premium is truly off the charts, at a nosebleed 33% right now!

Imagine paying $1.33 for every $1 of assets a fund holds. Absolutely ridiculous, even for a fund with the famed (in CEF-land) PIMCO name stamped on it.

Luckily there are still lots of deals floating around on high-yield CEFs. And to show you the wealth-producing power of these funds, I’ve put 4 of my very best picks in a Special Report I want to give you today. These 4 CEFs yield 9.5% between them and trade at such steep discounts I’m calling for 20%+ price upside in the next 12 months across the board.