Wall Street still treats utilities like income relics. Big mistake.

The same wires and substations that power your home now feed NVIDIA’s data centers—and our portfolios. These “boring” utilities are morphing into AI toll collectors, handing us up to 10.4% dividends while vanilla investors chase momentum stocks.

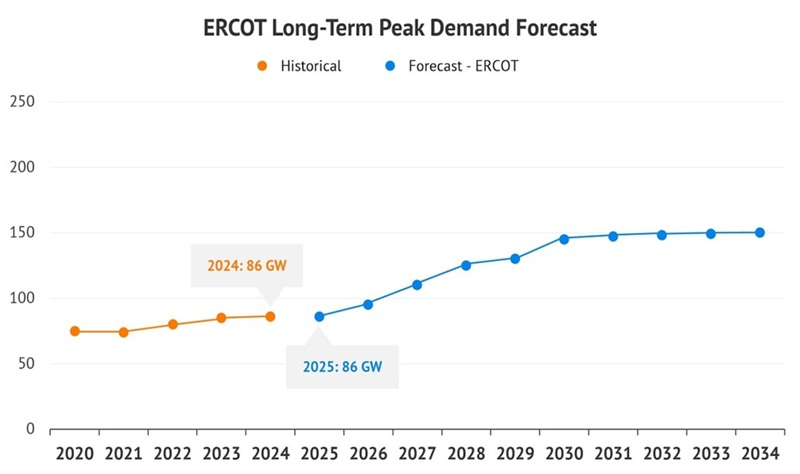

Take Texas, for example. The grid is strained. The population is popping. New residents, factories and AI campuses are all plugging into the state’s aging grid at once. The math is no longer “mathing” and it’s about to get worse. ERCOT projects power demand will jump 62% by 2030—yikes!

And Oncor, the state’s largest utility, believes that is way too conservative. Its interconnection queue shows 186 GW of requests waiting to plug into the grid—more than double today’s peak demand (118% more!) and enough to power every home in Texas twice over!

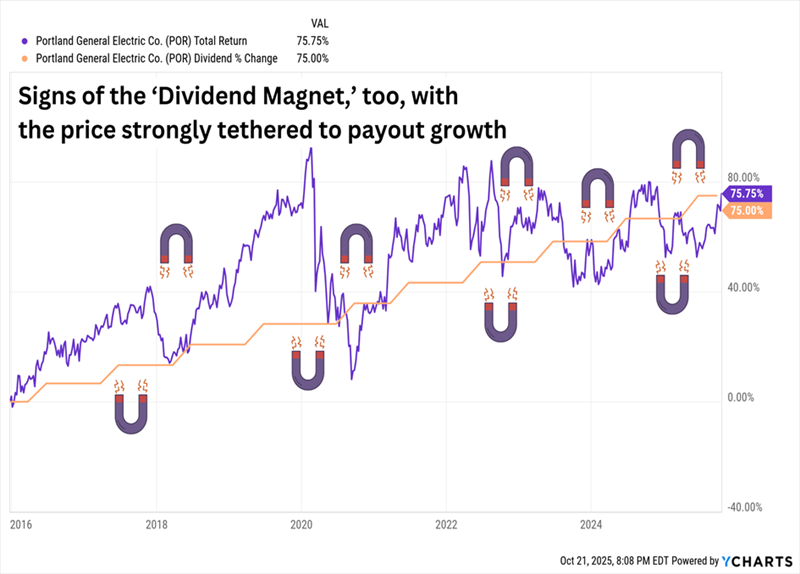

Texas isn’t the home of the only strained grid. Let’s head to the Northwest and visit Portland General Electric (POR, 4.8% yield), which provides electricity to 1.9 million customers across more than 50 cities in Oregon. Thanks to early AI grid work, this near-5% payer is one of the few “boring” utilities with genuine growth voltage.

This West Coast Utility Delivers Even-Keeled Price and Dividend Growth

“PGE” is gearing up for the AI revolution. Recently, it announced that it’s using a new AI-enabled flexibility tool that will free up more than 80 megawatts for datacenter interconnections next year. Here’s a little detail, courtesy of digital business mag Utility Dive:

“PGE partnered with the California-based startup GridCARE, which uses AI, detailed hourly demand modeling and optimized flexible resources like batteries and onsite generators to find spare capacity. The added flexibility allows PGE ‘to interconnect multiple data center customers years earlier than initially expected,’ the companies said.”

Oregon, and Portland specifically, is currently a decent-sized datacenter market, though many other states are seeing a more rapid rate of expansion. In the meantime, PGE is ramping up investments in its own infrastructure; however, some of those costs are to mitigate the state’s growing risks for severe wildfires.

Fire risk keeps investors away, but a near-6% yield and single-digit P/E make

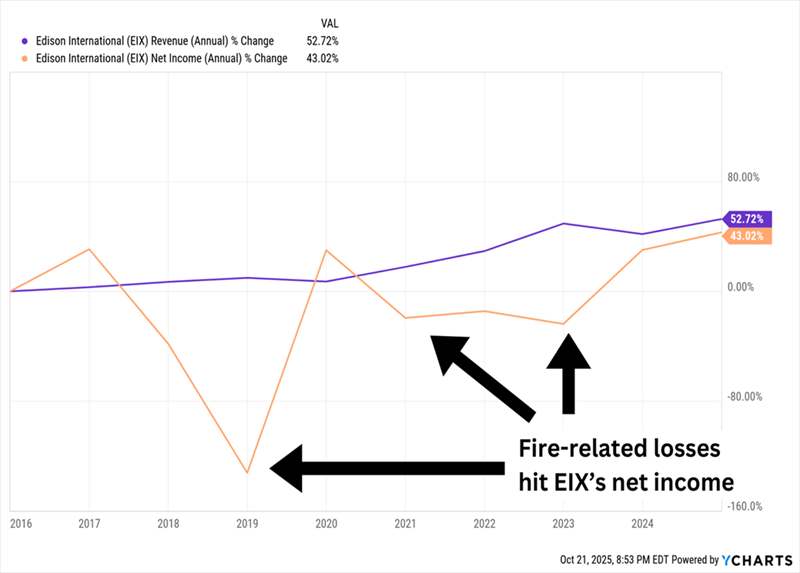

Edison International (EIX, 5.9% yield) a classic contrarian setup. One positive legal surprise and this scorched stock could light up. Edison serves more than 15 million customers and generates much of its electricity from renewable sources including solar, wind, and hydro. EIX also has an unconventional second business: a global energy advisory division.

EIX’s forward price-to-earnings (P/E) ratio sits at just 9; that’s less than half the sector. Its price/earnings-to-growth (PEG) ratio of 0.6 signals it’s on sale, too. (Any PEG of less than 1 is considered undervalued.)

Edison is cheap for a reason, but that reason is no secret. While PGE might have wildfire risk, EIX has known wildfire exposure—specifically, it has spent years fighting litigation over wildfire damage and has paid multiple billion-dollar-plus settlements.

Fire Has Repeatedly Burned Edison’s Bottom Line

Edison could still be on the hook for billions more related to the Eaton fires. It looked like EIX was due for some relief in September, when the California Legislature passed SB 254, creating a wildfire fund continuation account that Edison and other state utilities could tap for future wildfires—but the $18 billion figure was weaker than expected, leading S&P Global to lower its ratings on Edison’s various debt issues.

The flip side? EIX is big on renewable energy, its SoCal residential base is huge, it has an otherwise strong balance sheet, and it pays nearly 6%, dwarfing the sector average. Positive surprises about any Eaton liabilities could jolt the stock to life. So, Edison remains a much bigger high-risk, high-reward gamble than the average utility.

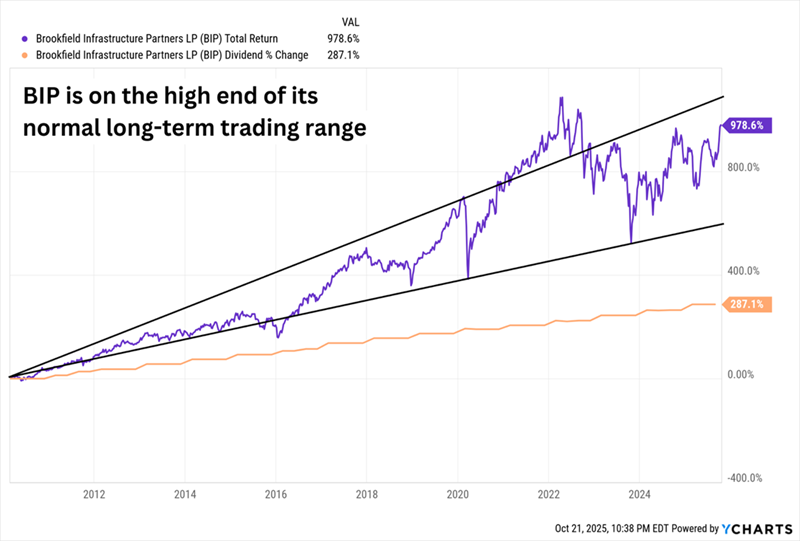

Canada’s Brookfield Infrastructure Partners LP (BIP, 4.9% yield) the global toll collector for the AI age—power lines, pipelines and 100+ data centers. BIP blends stable cash flow with growth tailwinds we usually pay tech multiples for.

And BIP’s assets give us two ways to leverage the AI megatrend.

For one, Brookfield boasts 8.6 million electricity and natural-gas connections, 4,500 kilometers of natural gas pipelines, and 83,700 kilometers of electricity transmission lines. But it also has a data segment that includes 312,000 operating towers and rooftop sites, 28,000 kilometers of fiber optic cable and more than 100 datacenter sites.

The problem (or advantage, depending on one’s point of view) of Brookfield is we’re getting a little bit of exposure to a lot of different things. That’s the nature of a conglomerate. But while the assets are infrastructure in nature, it’s not a very defensive stock—the flip side to that is BIP will often give us buyable dips.

However, It’s Not in One Now

Broadly, though, BIP is a well-paying stock that has raised its distribution for 16 consecutive years. I say “distribution” because it’s structured as a master limited partnership. Now, 99.9% of the time, that’s a drawback given that MLPs force us to deal with Form K-1 come tax time, but Brookfield is special—it has a mirror corporate structure, Brookfield Infrastructure Corporation (BIPC), that pays out qualified dividends instead. Alas, those shares only yield about 3.7% right now.

We can get even sweeter yields out of the utility space by investing via closed-end funds (CEFs).

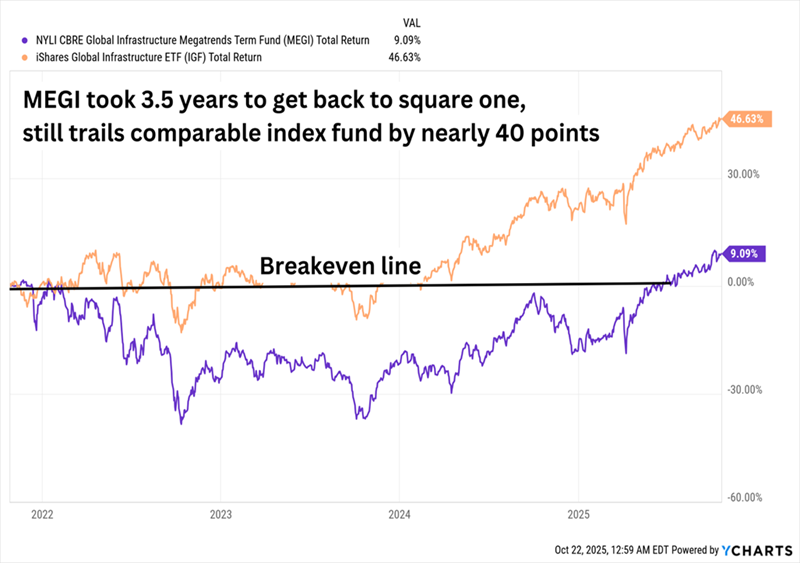

Consider the MEGI NYLI CBRE Global Infrastructure Megatrends Term Fund (MEGI, 10.1% distribution rate), for instance. This mouthful of a fund is somewhat similar to BIP in that it’s not a true utility fund. But we’re still getting a heaping helping—55% of assets are allocated to utility companies such as Essential Utilities (WTRG), PPL Corp. (PPL), and PG&E Corp. (PCE). But we also get double-digit exposure to transportation, communications, and midstream/pipelines. We even get some preferred stock.

And thanks to liberal use of leverage (24% currently), we get a fat double-digit yield.

What we don’t get is much in the way of return.

Even Plain-Vanilla ETFs Have Trounced This Pseudo-Utility Play

Like with Brookfield, this global infrastructure CEF is a little too broad. I hesitate to recommend it here or in my Contrarian Income Report. However, I do keep my eye out for deep discounts on MEGI that we can take advantage of in Dividend Swing Trader. The price is currently just OK—yes, it trades at a decent 7% discount to net asset value (NAV), but that’s not even cheaper than its longer-term average discount of more than 12%.

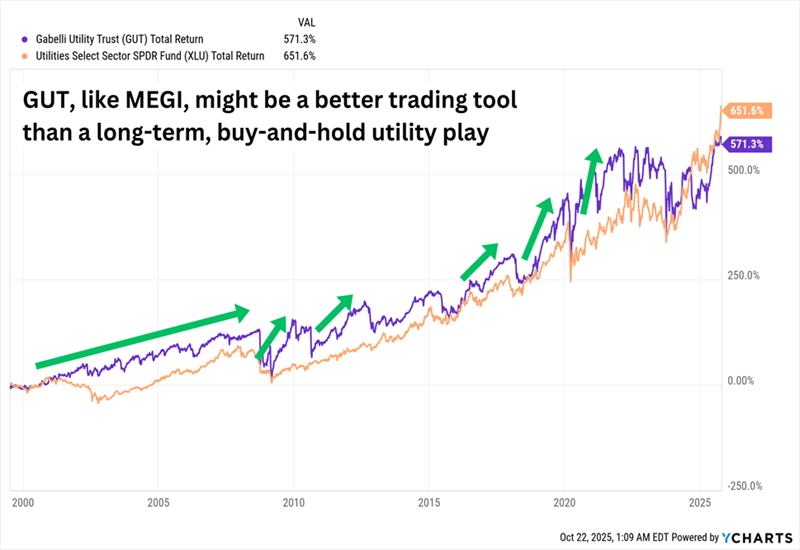

We get much better utility exposure with the Gabelli Utility Trust (GUT, 10.4% distribution rate). This still isn’t a pure-play utility-sector fund, but now we’re at close to 70% utilities (including EIX and POR), and another 15% or so in utility-esque telecom stocks like Deutsche Telekom AG (DTEGY) and Vodafone Group (VOD).

Long-term, GUT has been much more competitive with rank-and-file sector ETFs, though its moderately levered nature (15%) and exposure to other sectors has made it more volatile over time. So, like with MEGI, our best bet is to be patient and pounce on dips.

Gabelli’s Fund Trails Long-Term, But Timing Is Key to Outperformance

But it’s almost a foregone conclusion we’ll never get truly bargain prices on GUT. Shares currently trade at a wild 83% premium to NAV, which is somehow a smidge cheaper than its long-term average premium of around 90%. The cheapest it has traded over the past year or so is at a 50% premium to NAV.

Wall Street chases AI stocks that might go higher. We’ll take the utilities that power them—and collect a sure 10.4% while we wait.

Your Next Life-Changing Dividend (an Incredible 11% Payout) Is Right Here

CEFs are generally the right way to go if you want sky-high and steady payouts—we just don’t want to pay through the nose like we would be with GUT.

And we don’t have to.

Let me give you the inside scoop on one of my top current dividend recommendations. It’s another CEF, and it …

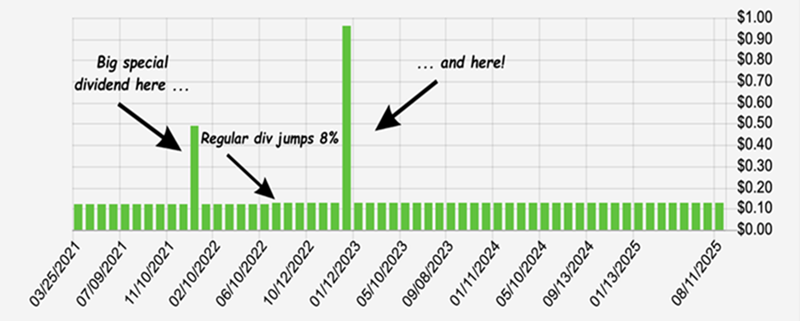

- Pays us an 11% yield

- Pays us a growing distribution over time

- Pays us each and every month

- Even pays us fat special dividends from time to time

Take a look at this happy dividend chart:

This is nothing short of a life-changing payout that could hand you a sweet $11,000 in dividends every year, on every $100,000 investment you make.

I want to share all the details on this unique income fund with you now—and give you the chance to try Contrarian Income Report yourself, too.