Many retirees like the idea of a “50/50” portfolio that’s half bonds and half stocks. There’s even research that shows withdrawal rates of 3% and 4% may be safer with this mix than they’d be with 100% stocks.

That’s all well and good but doesn’t concern me much. I’m a “No Withdrawal” guy. I spent many late nights in college working up Monte Carlo simulations, where we’d run scenarios 50,000 times to figure out the optimal placement of, say, ambulances in a city to minimize the average response time to an emergency. This type of fancy modeling can work well when you’re able to use the law of large numbers to map the likelihood of every possible situation.

But these techniques don’t work well with stocks because we are dealing with a sample size of one. There’s no way to “re-run” the history of the US stock market to determine its average outcome. We have but one look at the past–and we don’t know how indicative that will be of future results.

So I prefer to leave my Operations Research degree in its frame and play it safe (and smart) when it comes to retirement advice. Dividends-only for us income seekers! Mark Twain, who popularized the three types of lies–lies, damned lies, and statistics–would be proud.

Our 9 Stocks and 10 Bonds Yielding 7.4%

Our Contrarian Income Report portfolio would make retirement researchers smile. Then again, maybe not – after one review they might need to find another profession after realizing we’ve completed their work!

As I write we own nine stock investments and ten bond funds in our CIR portfolio. Our 50/50 portfolio yields a generous 7.4%. That should embarrass any egghead who argues whether or not a 3% or 4% withdrawal is the safest maximum rate. These payouts are funded by company cash flows (in the case of our stocks) and income (our bonds) so we needn’t be bashful about spending our cash.

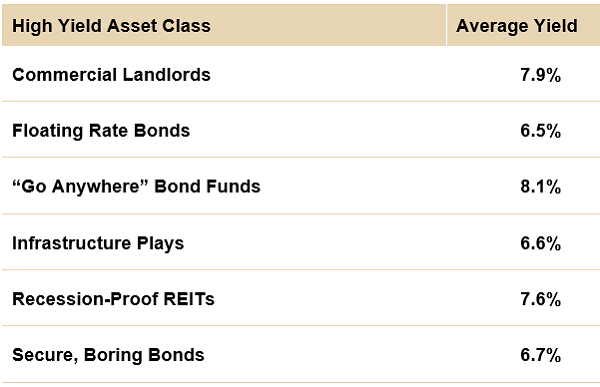

From there, we diversify our capital by spreading it across as many categories as we can. These six “buckets” contain stocks and funds that’ll further break up your 50/50 split:

Commercial Landlords boast dividends that are powered by tens of thousands of individual rent checks. They give us the ability to be real estate moguls from the convenience of our brokerage accounts.

Big banks aren’t as too interested in commercial real estate projects these days due to increasing regulatory requirements. As they’ve stepped away from the industry, boutiques like Ladder Capital (LADR) have stepped in to fill this profitable void.

I first recommended Ladder to Contrarian Income Report subscribers in September 2016. We bought a well-funded 8.3% yield with growth potential. It seemed like a no brainer.

It was. Ladder’s soaring dividend has attracted its share of attention from other income-focused investors. The firm’s charmed payout has helped the stock provide us CIR folks with 60.5% total returns–nearly double the S&P 500 over the same timeframe! (Plus, our yield on cost is 9.9% and climbing.)

Ladder Pays More and Appreciates More, Too

Floating Rate Bonds, meanwhile, are an asset class we purchased to protect ourselves from future Fed rate hikes. By purchasing funds we were able to diversify across 1,000+ holdings with a couple of clicks of the mouse.

Are these still relevant in our portfolio today? Ironically, yes. The last time we had this specific Fed setup, these safe 6%+ paying bonds jumped 20% in the year ahead!

The setup? The likelihood that short-term interest rates (as set by the Federal Reserve) will go nowhere over the next 12 months. With these funds trading for less than 90 cents on the dollar, it makes sense to collect this income despite a now-dovish Fed.

“Go Anywhere” Bond Funds let us cherry pick the best managers who in turn have access to deals that we individual investors never hear about. They get our money, and we in turn receive their expertise.

Their smarts are ours for free, by the way, when we purchase their funds at a discount to their NAVs. In effect, that discount is big enough that it more than “comps” us the management fee. And as savvy contrarians, we always demand discounts.

Brand name bond gurus DoubleLine’s Jeffrey Gundlach and PIMCO’s Dan Ivascyn will run your money fee-free if you know what to buy. And, more importantly, when to buy them. We bought their funds for around 90 cents on the dollar. That 10% discount more than covers their fees.

Infrastructure is perhaps the ultimate retirement bucket because, let’s face it, it would take decades of investment to fix America’s current infrastructure! Unfortunately, as desirable as their business may be, most infrastructure stocks either don’t pay dividends or don’t pay enough to retire on.

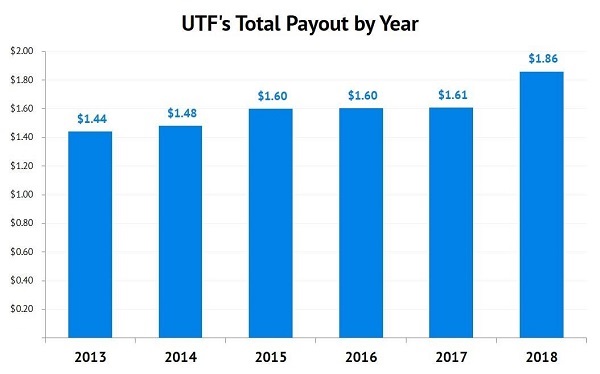

But we can “fix” this income problem by considering excellent funds such as the Cohen & Steers Infrastructure Fund (UTF). It regularly trades for a discount to the value of the assets it owns. And today that’s still the case, with the fund trading for $0.93 on the dollar–a 7% discount!

UTF invests in infrastructure companies that own and operate utilities, airports, toll roads, railroads, and other physical framework. Last year, management raised its monthly distribution nearly 16% (yes, you read right, from $0.134 to $0.155 per month). That’s a more than generous gesture, rarely seen in the sector.

Plus, it’s not unique for this fantastic fund. This is UTF’s third major dividend increase since 2013!

Recession-proof REITs are real estate investment trusts that hold properties which are always in demand. Think hospitals and warehouses stuffed with Amazon packages. These firms collect rent checks and are obligated to dish most of their income to us as dividends (a requirement of their tax-advantaged REIT status).

Finally let’s talk Secure, Boring Bonds. “Preferred stock” funds are a good example of this category. They are bond-like vehicles that help us get paid earlier–and more–than other investors.

Most investors only consider “common” shares of stock when they look for income. These are the shares in a company you receive when you place an order with your broker. You probably know the problem with this approach–common shares in S&P 500 companies pay less than 2% today on average.

Corporations issue “preferred” shares to raise capital. These issues generally pay dividends that receive priority over those paid on common shares. They are also usually higher than dividends on common shares, though the trade-off is that preferreds have less price upside. That’s a tradeoff we’ll gladly make today, with stock valuations high and interest rates in the basement.

Yours Now: An Entire 19-Stock Portfolio With Safe Cash Payouts Up to 11%

Defensive dividend-paying stocks and generous bonds are your “dividend lifeboats” when the markets get rough. That’s because their massive payouts give you more of your profits in cash, rather than paper gains that are here today, gone tomorrow.

But investing is like basketball. The best defense is a good offense, where a 100%+ gain makes up for a lot of mistakes! And all of the buckets I’ve outlined above not only pay 6%, 7% or more–but all six also boast investments with the potential to double your money.

Don’t Miss the Next 109% Gain

Hospital landlord Medical Properties Trust (MPW) is a great example of a recession-proof REIT. As I mentioned earlier, hospitals are constantly in demand. And since 2003, this firm has been acquiring US hospital properties at favorable prices.

The result? A stream of rent checks that have translated into an ever-increasing flow of dividends. But MPW doesn’t always get the respect from Wall Street that it deserves. My CIR subscribers took advantage of a misunderstanding and bought shares in November 2015 when the out-of-favor stock was paying more than 8%.

Its dividend has since become quite popular with retirees. We benefited with 109% gains that we recently cashed in!

How to Collect 8% Yields and Crush the S&P 500

Looking for the next MPW? An 8% payer with 100% upside? Here are 19 ideas for you.

$40,000 in Income on $500k

I’ve got 19 life-changing dividend plays to give you. I’m talking 7% to 8% cash payouts, on average—enough to let you retire on dividends alone with a $500k nest egg, thanks to the $40,000 yearly income stream these defensive superstars give you.

That’s why I call this my “8% No-Withdrawal Portfolio.” I can’t wait to show it to you.

That’s not all, either.

Because I just released a new issue of my Contrarian Income Report newsletter, with fresh updates on the 19 stocks and funds in our service’s portfolio, which hands our savvy CIR members massive yields up to 11%!

I want to send all 19 of these cash-rich plays your way, too. This latest issue just went out to members a few days ago, and your copy is waiting for you now.