We’re in a weird time where interest rates are at (or at least near) a peak—but most people haven’t realized it yet. When they finally come around, one group of closed-end funds (CEFs) is likely to soar (and pay us double-digit dividends, too).

I’m talking about bond funds, and the “double-digit dividends” part is already well underway, with yields on some corporate-bond CEFs held by my CEF Insider service breaking over 12%. (An added bonus: most bond CEFs pay dividends monthly, too.)

By the way, it’s not just me talking here: it’s the world’s biggest asset manager, a firm that, due to its sheer size and deep research resources, has access to next-level insight no one else can compete with.

A $9.4-Trillion Bond Player Is Telling Us to Buy Bond CEFs Now

That would be BlackRock, which manages an astounding $9.4 trillion of assets. On the last earnings call, BlackRock President Rob Kapito said something interesting, pointing to “around seven trillion in money-market accounts that is ready when people feel that rates have peaked to flood the fixed-income market, and we need to position ourselves to capture that.”

In other words, there are a lot of savers that BlackRock wants to move from putting their money in high-interest savings accounts into funds holding municipal and corporate bonds.

Obviously, BlackRock is pitching to make more money here, but they aren’t the only ones to benefit—it’s a great strategy for savers, too, because as interest rates decline, bond prices will rise.

At the same time, rates on high-interest savings accounts will fall, pushing more of that “sidelined” cash into the fixed-income market, as Kapito says.

And before you ask, we favor bond CEFs because we want human managers managing our portfolios, not algorithms, because deep analysis is critical to successful bond investing (as are the personal connections only an active manager can provide; they get us access to the best new issues when they’re released).

That’s why investing with a firm like BlackRock is a great strategy with corporate bonds. But you don’t have to go with this dominant firm: other, smaller managers have strong histories, too:

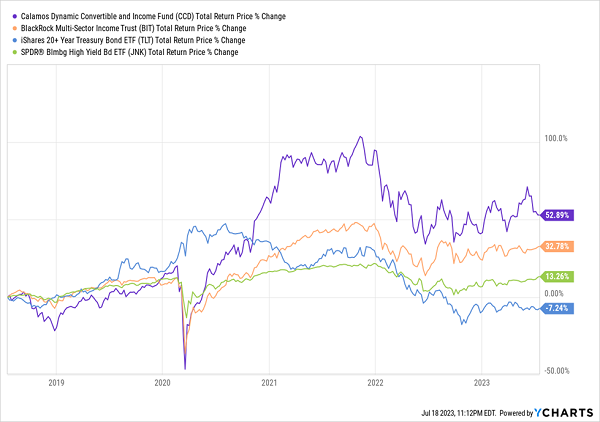

Income and Profits With Actively Managed Bond CEFs

Here you can see the Calamos Dynamic Convertible and Income Fund (CCD) and the BlackRock Multi-Sector Income Trust (BIT), two corporate bond–focused CEFs with big yields: CCD pays out 11.1% and BIT pays out 10.3%. So for every $10,000 in these funds, you’re getting about $87.50 a month on average, every month. That’s a six-figure income on just a million dollars.

Not only are these funds paying out large income streams, but you can see they handily beat holding long-term US Treasuries (the light blue line above, down 7.2% in the last five years) and the benchmark high-yield bond ETF, the SPDR Bloomberg High Yield Bond ETF (JNK), up just 13.3%.

And the better bargain here is somewhat surprising: BIT, despite its BlackRock pedigree, trades at a slight discount to net asset value (NAV, or the value of its underlying bond portfolio) as I write this, while the lower-profile Calamos fund sports a 2.7% premium. This just goes to show the mispricings that crop up regularly in the CEF market (which we always aim to capitalize on in CEF Insider.)

A Proven Record of Safety

But what if we have a recession, like the one everyone expected last year? According to Moody’s, the default rate on bonds would rise to 4.9% in 2024 because (you guessed it) bad economic times will make companies insolvent. That sounds high, but let’s dig in deeper.

That 4.9% actually relates to speculative-grade bonds, not all bonds. Most people don’t know that! They see the headline and, understandably, grow concerned. But only 23% of bonds are speculative grade, according to S&P Global. That means the economic worst-case-scenario is that 1.13% of all bonds default. To put that in context, five of CCD’s 455 bonds would default, for a total loss of NAV of about 2%.

So yes, CCD could see its portfolio decline 2% in the next two years due to defaults. But even that unlikely scenario would be dwarfed by the double-digit income stream CCD shareholders would be getting.

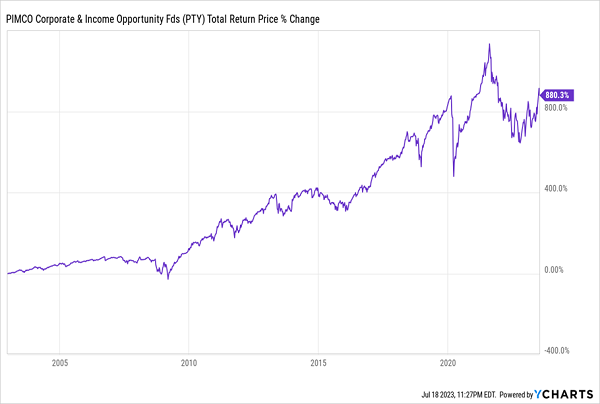

If you want even more safety, however, there are other options, such as investment-grade corporate bond funds that avoid distressed debt altogether. The PIMCO Corporate & Income Opportunity Fund (PTY) is one such example, and it has an enviable track record, booking nearly 900% profits since inception back in 2002.

Safe, Profitable PTY

The hitch? PIMCO is perhaps the only CEF manager with more cachet than BlackRock—cachet that translates into higher premiums on their funds. And right now, PTY sports a 30% premium. This one never trades at a discount, but now would be a good time to keep it on your watch list—and consider a buy when that premium drops, say below its five-year average of 23%.

My Top 2 Bond CEFs Are Cheap and Yield 9.5%+ (With Dividends Paid Monthly)

My top 2 bond CEFs to buy now sport huge 9.5% and 10.7% payouts, respectively, and they both pay dividends monthly!

They’re in a Special Report I’ve assembled that gives you a unique “mini-portfolio” of CEFs yielding 9.1% on average. In addition to these two stout bond-holding “battleship funds,” you also get details on two more CEFs holding the best blue chip stocks, including Visa (V), Coca-Cola (KO) and Amazon.com (AMZN).

Taken together, this quartet gives you an instantly diversified bond-stock setup that’s perfect for the “rate-topping” market we’re in now.

Plus, all 4 of these income plays are cheap today—so much so that I’m calling for 20%+ price upside from them in the next year.