This retirement portfolio pays 12.4%. Which means, on a million-dollar stake, these stocks dish $124,000 in dividend income alone.

That’s fantastic, needless to say! But are these stocks safe enough to actually retire on?

After all, we’re not looking to collect a 12.4% yield and lose it in price. Heck, we’re not interested in losing capital at all. We want the 12.4% with stocks that are at least steady.

Most common stocks would be in trouble if they paid 12.4%. But these are business development companies (BDCs), which yield so much because they have a special carve out from Uncle Sam.

Think of BDCs like private equity for the average Joe. These companies provide capital to small and midsized private businesses that many banks won’t even look at. That’s pretty similar to how private equity works—but unlike PE, you and I don’t need a million dollars to sniff the action. We can buy as little as a single share, which will typically run 20, 30, maybe 40 bucks.

Of course, it’s a high-risk business, so BDCs tend to command higher rates of interest—which BDCs then turn around and distribute as higher dividends. Hence the 12.4% average payout I mentioned.

These BDCs are required to pay up! BDCs, like real estate investment trusts (REITs), were a creation of Congress to spur investment. And like REITs, they are obligated to pay out at least 90% of their taxable income to shareholders in the form of dividends.

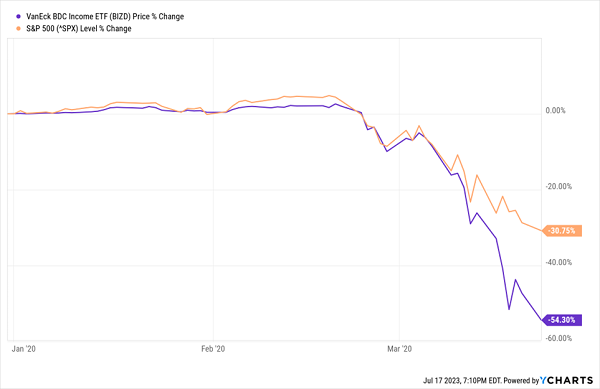

It’s a tough business, though. BDCs’ business is small businesses, which are extremely sensitive to economic conditions. Take the COVID bear market, for instance—as bad as things were for the blue chips of the S&P 500, they were far worse for business development companies and their tiny portfolio holdings:

BDCs Were Hollowed Out When COVID Struck

The BDC industry has largely recovered, of course, and it’s joining the broader market in rebounding this year. A big part of that is what’s happening with interest rates—namely, while long-term interest rates (what BDCs borrow at) have been rising, short-term interest rates (what many BDCs’ floating-rate loans to portfolio companies are pegged to) have been even more explosive, helping fatten margins.

Enter: The risk.

The Federal Reserve has pushed the “pause” button on its year-plus-long rate-hiking spree. That’s not as much of a concern for BDCs as what comes in the indefinite thereafter—an eventual reversal of rates. Lower short-term rates can threaten both BDCs’ profitability and their dividend coverage, which is often aggressively tight, leading to frequent, ahem, negative dividend adjustments over time.

So, while it’s easy to be lured in by BDCs’ high headline yields, we want to make sure we’re prioritizing quality—otherwise, those yields, and our stock prices, will be heading lower whenever Fed Chair Powell turns dovish again.

With that in mind, let’s take a scrutinizing eye toward these three BDCs, which currently deliver yields averaging 12.4%.

Blue Owl Capital Corporation (OBDC)

Dividend Yield: 9.7%

Discount to NAV: 7%

Blue Owl Capital Corporation (OBDC) might sound a little familiar but not quite ring a bell. That’s because just a couple weeks ago, it rebranded from its previous name Owl Rock Capital Corporation (and ticker, ORCC).

New name, but same aims.

Blue Owl originates, executes, and manages both debt and equity investments in U.S. middle-market companies, typically with annual EBITDA of between $10 million and $250 million, and/or annual revenue of $50 million to $2.5 billion at the time of investment.

Currently, Blue Owl boasts 187 portfolio companies, spanning roughly 30 industries such as internet software and services, manufacturing, healthcare providers and services, consumer products, even aerospace and defense—the kind of diversification you’d want out of a private equity fund.

And it’s built for a rising-rate environment, too. The lion’s share (71%) of the portfolio is first lien senior secured debt, with another 14% in second lien senior secureds. Across its entire debt portfolio, all but 2% of its loans are floating-rate in nature—meaning increases in short-term rates have been fuel for the fire.

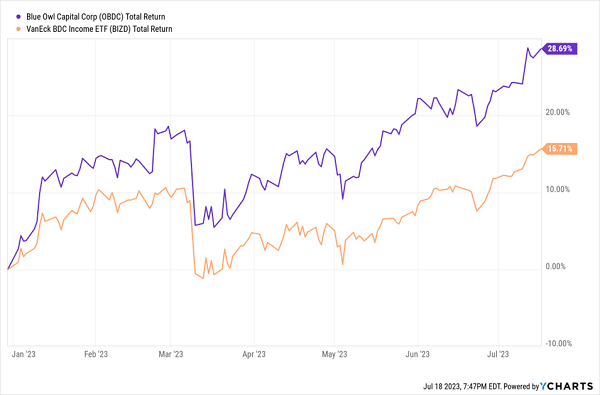

Blue Owl Has Soared Past Its BDC Peers in 2023

And despite that outperformance, OBDC is trading at a 7% discount to its NAV.

The flip side? An eventual drop in short-term rates could disrupt Blue Owl more than others. I’d expect OBDC could still weather that, but I wouldn’t count on OBDC collapsing—this is a well-run firm

Still, OBDC is an excellent operator. Blue Owl leans toward established companies with experienced management, strong competitive positioning, and positive cash flow. The result is one of the highest credit qualities among BDCs, with non-accruals at less than 1% of the portfolio.

Retirement investors will like Blue Owl’s dividend management, too. The company pays out a high core dividend—currently 33 cents per share, which translates into a roughly 9.3% yield. However, it also pays out 50% of net investment income in excess of the core dividend as supplemental dividends—a few cents’ worth of top-up that gets OBDC closer to 10%. Thus, investors can still rely on a high payout, but at the same time, OBDC has a little flexibility to pull back on payouts in difficult times without cutting its core dividend.

BlackRock TCP Capital Corporation (TCPC)

Dividend Yield: 12.7%

Discount to NAV: 12%

With BlackRock TCP Capital Corporation (TCPC), an externally managed BDC, we’re getting an even higher yield and a deeper discount to NAV. We just want to make sure we’re not getting more headaches, too.

BlackRock TCP Capital’s advisor, Tennenbaum Capital Partners (TCP, an indirect BlackRock subsidiary), primarily invests in the debt of middle-market companies with enterprise values of between $100 million and $1.5 billion.

TCPC has a healthy 143 portfolio companies, and like ODBC, they’re spread across a wide range of industries. That said, TCPC does have several industries with double-digit exposure—internet software and services, diversified financial services, diversified consumer services, and software—while many of its other industrial weightings are relative sprinkles.

Source: BlackRock TCP Capital Corporation first-quarter investor presentation

Also like OBDC, BlackRock TPC is heavily invested in first lien (76%) and second lien (12%) senior secured loans, and the vast majority (94%) of its debt portfolio is floating-rate in nature. TCPC has recovered decently enough from the COVID downturn as a result.

Indeed, after cutting its payout by 16% during summer 2020, it finally started ticking up its payments, with dividend hikes in both December 2022 and June 2023—the 34-cent dividend now sits just 2 cents off pre-COVID levels. In the meantime, TCPC recorded record net investment income of 44 cents per share, which is well more than what it needs to cover that payout.

Perhaps the only other worry here (other than an eventual drawback in interest rates) is credit quality. Yes, TCPC has a very low (<1%) level of non-accruals, but “stressed” investments are in the high single digits.

FS KKR Capital Corporation (FSK)

Dividend Yield: 14.7%

Discount to NAV: 21%

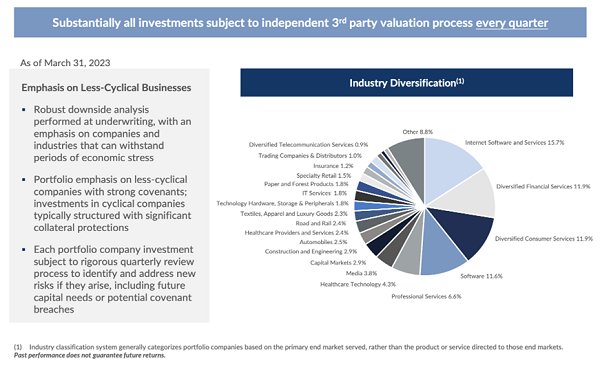

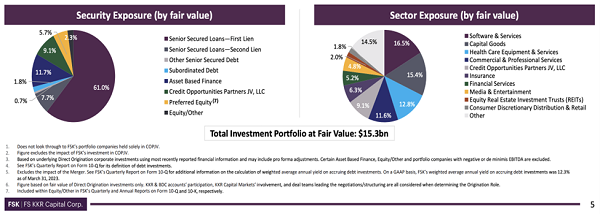

FS KKR Capital (FSK) provides financing to private middle-market companies, primarily by investing in senior secured debt (69%), though it also deals in subordinated debt, preferred equity, equity and other means of financing.

Its 189 portfolio companies are spread across a fair number of industries, though again, there are several heavy chunks—software and services, capital goods, healthcare equipment and services, and commercial and professional services are all double-digit weightings. It also has high-single-digit exposure to Credit Opportunities Partners JV, a joint venture with South Carolina Retirement Systems Group Trust that invests capital across a range of investments.

Source: FS KKR Capital Corporation first-quarter investor presentation

So, we have a massive dividend that’s yielding close to 15% to present, and it trades at a discount of more than 21% of its net asset value! And despite being a historically weak operator, FSK’s net investment income has exceeded expectations the past couple of quarters.

Better still: The company expects to pay 6-cent quarterly supplemental dividends on top of its 64-cent quarterly core dividend throughout the rest of the year.

Also, as I pointed out a couple months ago, FSK insiders are growing bullish on their own cooking.

FS KKR isn’t as tethered to short-term rates as the previous two BDCs, but its floating-rate share is still high, at nearly 90%. So it still could falter should interest rates turn tail. But where FS KKR differs from a downside perspective is credit quality. Nonaccruals are a much higher 2.7% at fair value. So if we do see a weaker economy or even a recession in the rest of 2023 or 2024, FSK’s portfolio could be more exposed than some of its higher-quality peers.

Give Me 4 Minutes, I’ll 4X Your Retirement Income

The whole point of a high-yield retirement portfolio is not having to worry about ups and downs, whether it’s the stock market, the economy or Jerome Powell’s mood. So while these yields are nice, I don’t want to keep looking around the corner for the next Fed move, wondering if my dividends will be safe next month.

Fortunately, I don’t have to—and you don’t, either.

My “Perfect Income” portfolio attacks retirement investing from a different angle. Rather than trying to time the market and chase trends, we target high-yield holdings (roughly 4x the S&P!) that walk their own path, no matter what the Fed, Congress or the rest of the world throws their way.

So, what makes these dividends “perfect”? Well, they have to have a few things in common:

- They DO pay consistently, predictably and reliably.

- They DO survive—and even thrive—in market crashes.

- They DO deliver double-digit returns, with safe, secure investments.

- They DO require minimal management time—just a few minutes every month!

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!