2025 is here and we’ve got a terrific opportunity in front of us: A shot at a very comfortable retirement with around $1.1 million saved. Heck, not only comfortable, but possible without withdrawing a single penny from our savings.

And depending on your circumstances, you may be able to clock out on a lot less.

I know that goes against the narrative that’s been driven into our heads for pretty much our entire lives as investors: That we need to work well into our sixties (and maybe beyond) before breaking free of our commitment to work. But from time to time, we do hear about a few people who prove this isn’t necessary for everyone.

For instance, CNBC recently reported on a former chef and small-business owner who retired in 1991 with just $500,000 invested. Adjusted for inflation, that’s about—you guessed it—$1.1 million today. I know that doesn’t seem like enough to retire on, especially if you stick to the oft-cited 4% rule, which says you can only safely withdraw 4% of your savings in retirement.

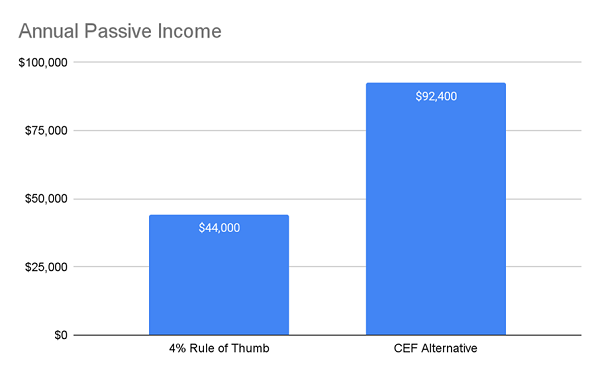

If a couple were to do that on $1.1 million today (in cash), they’d be living on $22,000 per person annually, or about a third of the average American’s salary. That’s $44,000 a year between them.

But if we were to invest in the fund—closed-end fund (CEF), to be more specific—we’re going to look at next, this couple would get $92,400 in dividend income per year without withdrawing from their nest egg at all. It amounts to an 8.4% yield that hasn’t just held steady: It’s grown over the years.

Source: CEF Insider

To be clear, I’m not suggesting you pile all of your savings into just one fund, no matter how good it is. This is just to demonstrate the income-producing power of CEFs, which yield around 8% on average.

And many CEFs pay more than that, with the average fund in the portfolio of our CEF Insider service yielding a retirement-changing 10.1% as I write this. Spread your savings across those, and you could generate $111,100 in dividends on your $1.1 mil. Or you could save less—just around $919,000—to get that $92,400 in yearly dividends.

But for now, let’s just swing back to that single fund I touched on earlier so you can see how it can sustain (and even grow) that 8.4% income stream with ease.

How This “Preferred” Fund Keeps Its 8.4% Payout Rolling Out to Shareholders

The 8.4%-payer in question is the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund (PTA). I know the title is a mouthful, but the key thing to remember is right in that name: PTA holds preferred stocks.

Preferreds are so-called “hybrid” investments: part stock, part bond. Like common stocks, they trade on an exchange and represent ownership in a company. But like a bond, their dividends are usually fixed. Additionally, the value of those dividends is likely to go up as rates fall, since newer preferreds will yield less. Thus, the bigger yields on PTA’s holdings could cause them to be valued higher in the future.

Banks and other financial institutions are the biggest issuers of preferreds, so it’s no surprise to see offerings from Wells Fargo, Citigroup and Charles Schwab among PTA’s top holdings.

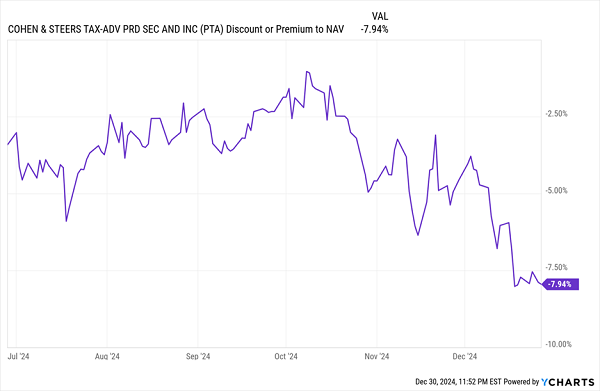

Preferreds’ high yields are the main driver of PTA’s 8.4% payout to us. But they’re not the only thing at work here. Another factor is PTA’s discount to net asset value (NAV), a valuation measure that’s a bit of a quirk of CEFs.

Here’s how it works: CEFs, unlike their ETF cousins, have a fixed number of shares that they can issue, and since those shares trade publicly, the markets can sometimes price a CEF higher or lower than the NAV of its holdings. In PTA’s case, that discount has widened in recent weeks to 7.9% as of this writing, from 2% a few months earlier.

PTA Gets Cheaper

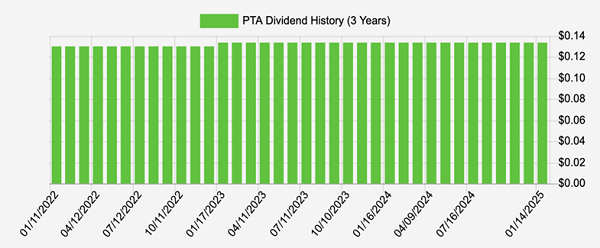

The discount means that, while PTA pays out 8.4% based on its market price (or the yield we get), it only needs to earn 7.8% from its portfolio of preferred stocks to sustain its dividend. Plus, it’s worth noting that PTA raised its payout in late 2023 and has never cut its dividend in its history:

A Consistent, Growing Payout

Source: Income Calendar

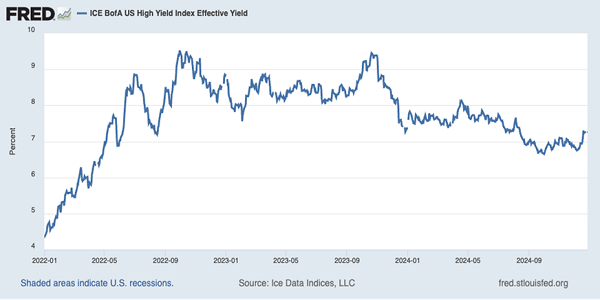

Still, even 7.8% is still a high dividend. How can it be sustained? This chart goes a long way toward explaining that.

High Yield Goes Higher

This chart shows the average yield that high-yield corporate bonds pay out to creditors, averaging 7.3% as of this writing and going over 9% briefly over the last three years while maintaining an average around 8% over that time period.

PTA has had three years to accumulate preferred stocks when interest rates were at these levels. Preferreds aren’t high-yield bonds, of course, but they must offer similar yields because both compete for investment from the same kinds of creditors, such as hedge funds.

This competition means yields on preferred stocks and high-yield bonds tend to be similar. We can see this when we compare the current yields on the corporate-bond benchmark SPDR Bloomberg High Yield Bond ETF (JNK) and the iShares Preferred and Income Securities ETF (PFF), which both pay around 6.5% as I write this.

PTA, with its human managers, has been able to purchase even higher-yielding preferred stocks that boost its overall payouts to shareholders and make its current payout rate very sustainable.

Now, again, we’re not suggesting going “all in” on PTA here. But the takeaway is that high-yield funds like it can play a crucial role in getting us to financial independence faster, especially if we diversify across CEFs with sustainable yields that trade at big discounts to their actual market value.

From Preferreds to … AI!? 5 CEFs Yielding 9.5% as Tech Soars Again in 2025

Artificial intelligence is still in its early stages—and the real money will be made as it continues to move from chatbots like ChatGPT toward integration into the devices and apps we use every day.

As that happens, profits will soar for select companies as operating costs (including, yes, salaries for human workers) are cut.

So no, if you haven’t invested in AI yet, you are NOT too late—provided you buy the right AI investments. Which is where CEFs re-enter the picture.

I’ve zeroed in on 5 AI-focused CEFs that throw off huge 9.5% average dividends today. That’s a big deal because it means we’re getting the lion’s share of our profits in safe, reliable dividend cash.

PLUS, these 5 funds trade at big discounts to NAV, essentially letting us buy the AI stocks they hold—kingpins like Microsoft, NVIDIA and Alphabet—at prices these stocks last saw months ago.

Now, with 2025—and the next leg of AI’s growth—dawning, is the perfect time to buy these tech-savvy dividend payers. Click here and I’ll tell you more about these 9.5%-paying AI funds and give you a free Special Report revealing their names and tickers.