I know it’s easy to get discouraged by the lack of bargains (not to mention the pathetic yields) available to us today, after stocks bounced back from the tariff-driven selloff.

But I have good news on this front: We still have plenty of places to hunt for big yields, even in this “pricey” market.

We just have to step a bit beyond mainstream choices—specifically to closed-end funds (CEFs), of which there are about 400 or so on the market. As I write, these funds, which are as easy to invest in as any ETF, yield around 8.7% on average.

But it’s the valuation story (source of the price upside we demand in addition to those big dividends) that’s particularly compelling here—and that side of things often gets overlooked as investors zero in on CEFs’ outsized dividend payouts, many of which are paid monthly.

Plenty of These 8%+ Dividends Are Bargains Now …

As I write this, the average CEF trades at a 4.6% discount to net asset value (NAV, or the value of its underlying portfolio). And that’s just the average. Many CEFs are cheaper.

CEFs can offer these discounts because they generally can’t issue new shares to new investors after they launch. The result is that the fund’s market price can trade above or below NAV. When it’s below, we say it’s trading at a discount.

This will all likely sound very familiar to you if you’re a member of my CEF Insider service, as discounts to NAV are key to our strategy there. But sometimes we see a discount so extreme that it jumps off the page—here I’m talking bigger than, say, 16 or 17%, where most CEF markdowns bottom out.

When we see a discount bigger than that, we have to look more closely to see if it’s an overlooked bargain or if it’s cheap for a reason.

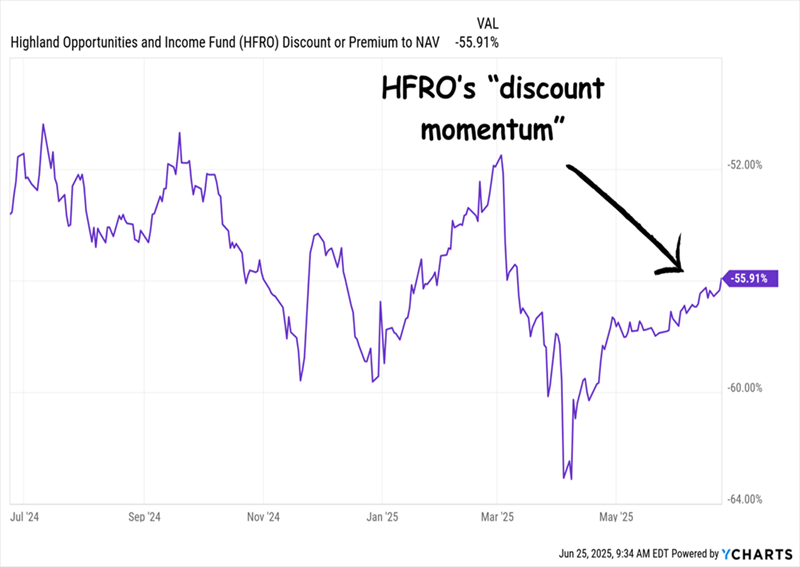

… But This 56% Discount Breaks the Mold

Which brings me to the Highland Opportunities and Income Fund (HFRO), which yields 8.9% today and also pays dividends monthly. The fund also ticks our diversification box, as it holds its nearly $900 million in assets tied up in a mix of stocks (about two thirds of the portfolio) bonds and real estate loans (nearly the other third), and the remainder in cash.

Most of this is tied up in NexPoint real estate assets, with a mix of equity and debt for NexPoint’s single family homes investment, NexPoint Storage Partners, NexPoint Real Estate Finance and NexPoint Hospitality Trust.

But the number that really leaps off the page is the discount, which clocks in at 56% as I write this.

HFRO’s Extreme Discount

That makes HFRO the most discounted CEF out there—and in fact one of the cheapest I’ve ever seen, though it is slightly less of a bargain than it was during the April selloff, when its discount fell below 60%.

It’s the erosion—but clear momentum, as you can see at right in the chart above—that makes this fund worth a look today, as a shrinking discount tends to pull up a fund’s market price along with it.

And there’s something else that happens when a CEF trades at a discount—and especially a deep discount: It makes the payout safer. HFRO’s 8.9% yield, for example, is calculated based on the (deeply) discounted market price. But when you calculate yield based on NAV, it comes out to a lot less: just 3.9%.

In other words, HFRO needs to earn 3.9% to maintain its current payouts, which is a ridiculously low bar in today’s markets, where the average high-yield corporate bond yields over 7% and S&P 500 stocks post an annualized return of 10% in the long run.

Now this might sound a little too good to be true to you, and it partly is. Last time I wrote about HFRO, I noted that much of the fund’s investments were in properties that the fund’s management company, NexPoint, holds. Here’s what I said then:

“If we look at HFRO’s top holdings, we see that its management firm, NexPoint, has invested significantly in NexPoint properties … While NexPoint may see NexPoint assets as the best places for HFRO’s investments, I’m concerned that these haven’t, in fact, helped investors much.”

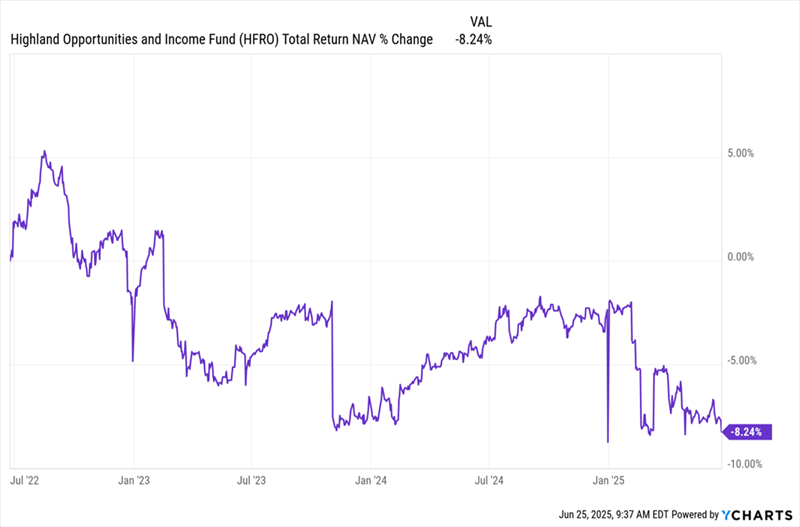

That admittedly sounds a bit harsh. But when I was writing then, HFRO had returned just 4.4% in 2024 on a total NAV basis (or going by the performance of its underlying portfolio, including dividends collected and reinvested), after slipping in value over the preceding two years. And in fact, HFRO’s total NAV return is still in the red over the last three years.

HFRO’s Rough Run

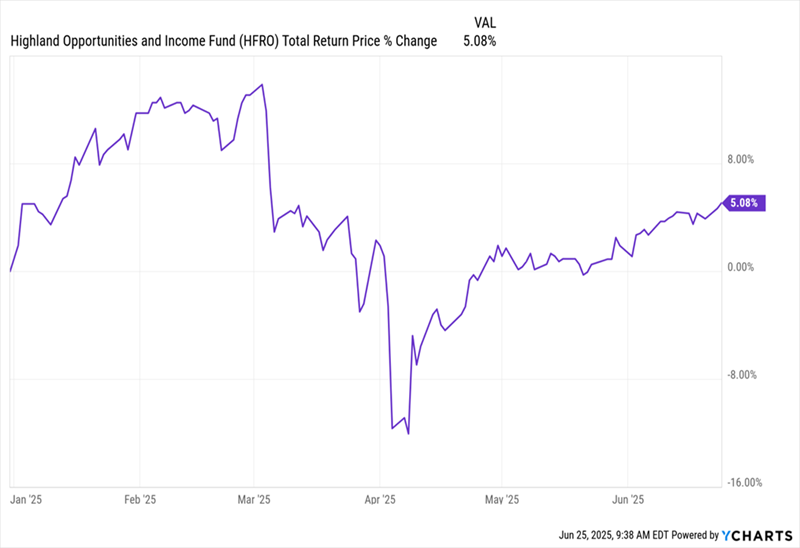

In light of that, HFRO’s extreme discount makes some sense. But at this point we need to ask: “Just how low can a discount go? Surely over half off is a bargain, right?” And I have to admit, this tempts me to dip a toe into HFRO. But this chart shows that it’s not quite the right time.

HFRO’s Total Return Rises …

Year to date, HFRO’s total return (based on market price) is up, thanks to that narrowing of the discount we just talked about. But it only started to build momentum at the start of May, after a big dip in March and April. Another market selloff could cause that dip to recur.

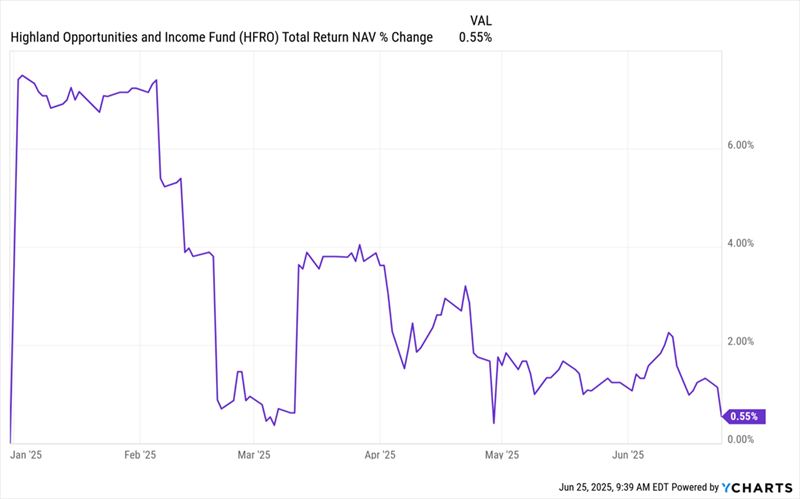

… But Its Portfolio Lags

Here we see that HFRO’s total NAV return rose markedly at the start of 2025, when corporate bonds in general got a boost, but we’ve seen that momentum fade, and now the fund’s total NAV return is nearly flat year to date.

In addition, the fund’s total NAV return trails the popular index fund for high-yield corporate bonds (a reasonable benchmark for HFRO—in orange below), which is up 3.5% in 2025. It trails the benchmark over the last decade, as well, having broken away from it in late 2023.

HFRO Trails the Bond Benchmark

So, it seems clear at this point HFRO isn’t a buy today. If its discount gets wider, it may indeed be worth a look. Until then, I continue to see it as speculative, and we’re happy to continue to keep watch on it from a distance.

These 10.2% Monthly Payers Are REAL Overlooked Bargains (and Urgent Buys)

As I said earlier, the CEF market is 400 funds strong. That’s just the right size for us: Big enough that there are always deals to be had—but not so big as to overwhelm us in our search.

What’s more, over 300 CEFs pay dividends monthly, which is pretty much unheard of in ETFs or S&P 500 stocks. So, with average CEF yields around 8%, we’ve always got a shot at locking in cheap 8%+ monthly dividends here.

I’ve zeroed in 5 of the very best monthly dividend CEFs, and between them they pay huge 10.2% dividends now. And all 5 are TRUE bargains, to boot.

They’re ripe for buying today, and I can’t wait to show them to you. Click here and I’ll walk you through all 5 of these monthly income generators and give you a free Special Report revealing their names, tickers and my research on each one.