Do retirement solutions come any better than a safe 8% dividend, paid monthly?

This is what we contrarian income seekers love about the Aberdeen Asia-Pacific Income Fund (FAX). It pays 8% annually, dishes its dividend every month and, thanks to the debt situation in China, trades at a 7% discount to its net asset value (NAV)!

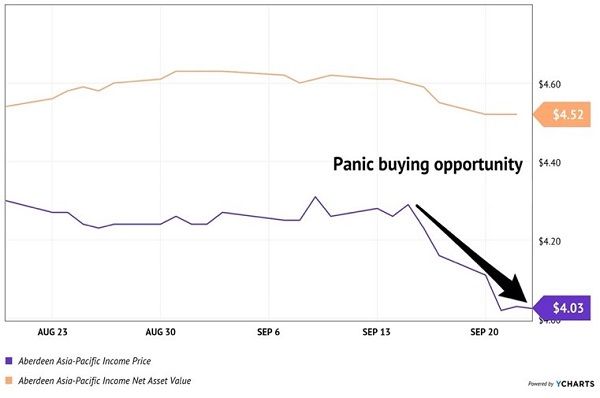

Last week, we pointed out a “mini-panic” buying opportunity in FAX. Its price had suffered, but you wouldn’t know it by looking at the fund’s NAV—the value of its bonds minus debt—which has barely budged over the past month:

NAV Was Steady, Pullback Was Price Only

Its price had been punished because armchair market observers fear Evergrande and the Chinese credit markets. When discount windows widen in CEFland due to this kind of short-term price panic, it’s usually a buying opportunity.

Perceived risk is not actual risk, however, and those selling because of headlines are overreacting. Rookies to Asian debt markets are wrong about FAX’s Chinese credit risk.

Rather than looking to “internet randos” for advice on the China situation, we went straight to the source. Most investors—even professional money managers—don’t do their homework. Not us. We hustle. We’ll talk to anyone and everyone who may have a perspective that could help us out…

…Especially Adam McCabe, arbdn’s (formerly Aberdeen) Head of Fixed Income for Asia and Australia! Here is the transcript of our recent and very timely discussion:

Brett: Adam, thanks for taking the time to catch up with us. As I mentioned last month when we first spoke, we repurchased FAX for our Contrarian Income Report portfolio in February 2019 and have enjoyed 25% total returns including dividends (8.6% annualized).

We are big fans of the $0.0275 monthly distribution and the “retire on dividends” lifestyle that FAX provides.

During our last interview, few US investors knew about Evergrande, the Chinese real estate group. Now there is armchair speculation that this could be China’s “Lehman moment”—drawing an analogy from the 2008 financial crisis.

What are you expecting from Evergrande?

Adam (Aberdeen): While we expect a restructuring of Evergrande, we believe that this will proceed in a more orderly manner than the market currently fears. Risk aversion is extreme, with the market pricing in a default rate of approximately 30%. We feel that this is an opportunity for investors to look past near-term volatility and uncertainty.

Fair enough, but should we fear debt contagion? In other words, should we be worried that Evergrande is the first “debt domino” that triggers more defaults?

We think that the financial contagion scenario is unlikely. The objective of the policies which have caused the Evergrande situation are to improve the financial stability of the property sector because it is so important to China’s economy. Ninety percent of Chinese families own property, which accounts for 70% of their household wealth.

I monitor US yield spreads closely and, despite the recent volatility in the equity markets and Evergrande headlines, they remain rather tight. This tells us that the bond market here [in the US] is not concerned about the September (and now October) swoon being anything other than seasonal volatility.

How are the spreads on Chinese yields looking? Are the riskier bonds seeing a spike in yields?

As the tightening liquidity conditions in the Chinese real estate sector in general, and for Evergrande specifically, bring economic and systemic risks to China, there are incentives for the administration to contain the systemic threat. We believe that the Chinese administration will continue to ensure there is sufficient liquidity in the financial system, with monetary easing a prominent feature. This easing will likely see Chinese government bond yields decline.

Your thinking about China aligns well with mine. What percentage of FAX’s portfolio will be supported by this government policy?

As of August 31, FAX holds about 7% in renminbi denominated government and government-related bonds, which will likely be supported by these policy actions.

Thanks for breaking down the mechanics of the Evergrande unwind with us, Adam.

FAX was an amazing bargain two-and-a-half years ago, trading for just 84 cents on the dollar. The fixed income world has wised up a bit since, so FAX’s discount window had narrowed from 16% then to just 7% now. Hopefully you bought the dip that we highlighted last week!

If not, no worries. There are more 7%+ dividends trading at discounts today.

But I don’t expect these “dividend deals” to last for long! October is often our “last call” for the bargain bin. Remember, stocks took off starting last November and never looked back. I’m expecting a similar seasonality this year.

So don’t wait, buy these discounted dividends now. Click here and I’ll highlight these monthly payers, including their names, tickers and my recommended buy prices.