A 7.7% payer we watch very closely just did something weird for a stock with such a high payout: it hiked its dividend—for the 29th straight year!

Most folks will tell you a 7.7% payer with a dividend that consistently grows is a myth at best—or a “yield trap” at worst. But these hikes are just another mark on the calendar for this company’s investors.

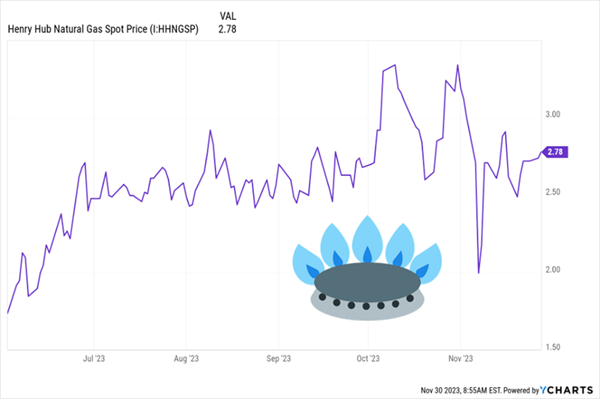

Its latest hike—and forecast of more of the same in 2024—came out in a press release from the company late last week. The firm is a little-known (at least here in the US) natural gas shipper. It’s a savvy buy as gas prices bump along the bottom—but start to rise from the sub-$2 lows we saw earlier in ’23:

“Natty” Starts to Simmer …

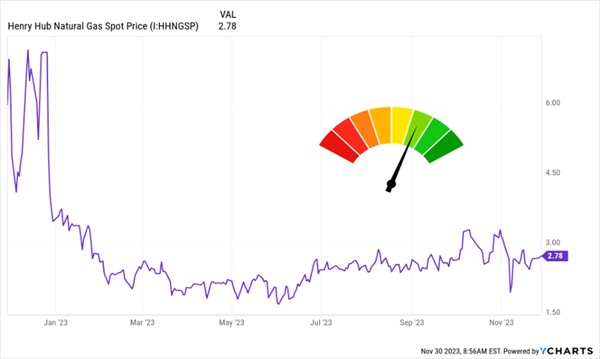

I get that this chart might make you think that we’re late to the party here. So let’s extend our view to one year back:

… And There’s Plenty of Room to Run

This, in other words, is a smart time to buy, when prices are still low but are on a sustained upward grind. You’ve no doubt heard the old saw that “the cure for low prices is low prices.” Well, this is that saying in action.

Which brings me back to that growing 7.7% “natty dividend.”

The company dishing that rich payout is Canada’s Enbridge (ENB), which has 74,000 miles of pipelines stretching across North America. It flies below the radar here in the US, but it shouldn’t: it moves about 20% of the gas used here every year.

Its “US invasion” continues: on September 4, Enbridge announced it’s buying three US utilities. When the deal closes in 2024, it will tack seven million customers in Ohio, Utah, Wyoming, Idaho and North Carolina onto the 15 million it serves north of the border.

Beyond that, ENB also has about $8 billion (Canadian) committed to in-service and under-construction renewable-power projects (and the transmission networks that serve them).

It’s a combo of scale and diversification we love to see. But before we go further, if you’re suspicious of a 7.7% payout in the volatile energy sector, I get it. But here’s the thing: even though ENB’s stock is influenced by gas prices, the business is a tollbooth, charging customers for every thermal unit of gas that flows down its pipelines. That cuts its sensitivity to prices and essentially makes it a “pseudo-utility.”

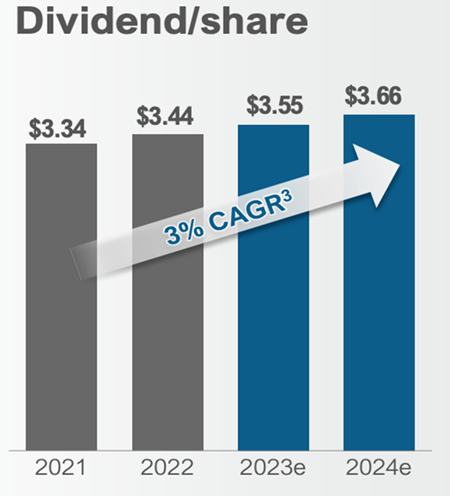

Rising “Tolls” Support Dividend—and Business—Growth

Because Enbridge has already built out its infrastructure, the pipelines hardly need any maintenance, so the “tolls” either flow out to us as dividends or fuel the company’s growth through acquisitions—which go on to grow the dividend!

Put it all together and we have three key sources of upside and payout growth here. First, the coming “rate rollover”: As interest rates decline in ’24, high-yielding plays like ENB will attract a lot of investors who get “shaken loose” from Treasuries and other so-called “safe” investments. Enbridge’s borrowing costs will also fall—indeed, the company forecasts a $4.1-million drop in that column in 2024.

Second, we can expect a further rise in gas prices, as “natty” moves closer to the $3.60 or so it’s averaged over the last five years. Finally, there’s that string of payout hikes, which have rolled on through the tire fire that has been the early 2020s.

Source: Enbridge 2024 financial guidance

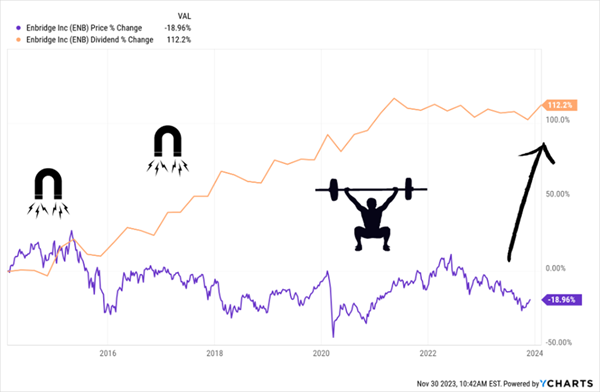

Yet despite all this, Enbridge’s share price has fallen far behind its dividend, which has more than doubled in the last 10 years:

Enbridge’s Dividend “Lag” Proves It’s Cheap

Now I know this dividend-growth chart might look unusual, so let me clear a few things up:

- Enbridge’s “Dividend Magnet” is due: If you’ve been reading my columns, you know that dividend growth is the No. 1 driver of share prices—where the dividend goes, the share price follows. So when a gap like the one above opens, it’s a buying opportunity.

- That 19% loss is misleading because it’s on a price basis. Factor in ENB’s high dividend—something screeners like Yahoo Finance and Google Finance do not do—and you see that shareholders enjoyed a 39% return in that time.

- Currency exchange skews the picture: The only reason why the orange “dividend” line above isn’t a beautiful staircase is because ENB pays dividends in Canadian dollars. More on this below.

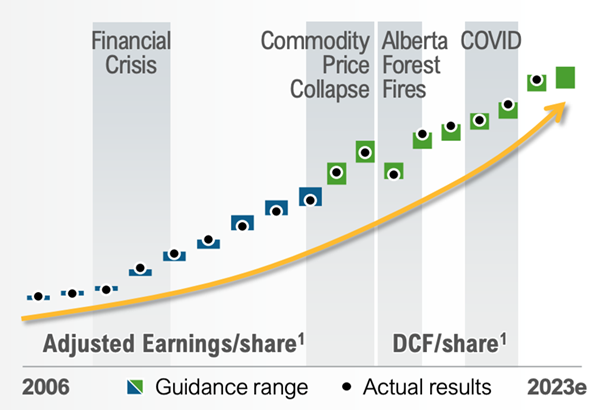

Moreover, this dividend is well covered: right now, Enbridge pays 65% of distributable cash flow as dividends, which is fine because its infrastructure is built out. It is a cash cow.

It expects that ratio to stay the same next year, and it’s calling for $5.40 to $5.80 in distributable cash flow (DCF) for 2024, the midpoint of which is up 3% from a year ago. And management has dead-eye aim when it comes to meeting guidance, no matter what car crashes the economy serves up (grey areas below):

Enbridge Goes 17 for 17 on Meeting Guidance

Source: Enbridge Q3 earnings presentation

Let’s wrap with the currency tailwind we touched on a second ago. Now that the Fed is essentially done with rate hikes, currency traders will look ahead. As the greenback falls with rates, it will give a lift to Enbridge, which reports its earnings in Canadian dollars. That’s yet another catalyst for this off-the-radar (for now) 7.7%-paying “pseudo-utility.”

Alert: This Top 2024 Pick Pays a Growing 14% Dividend

ENB is one of my top buys for 2024, no question. Any sustainable payout growing as fast as that of the “natty king” simply must make the list!

But it’s far from alone.

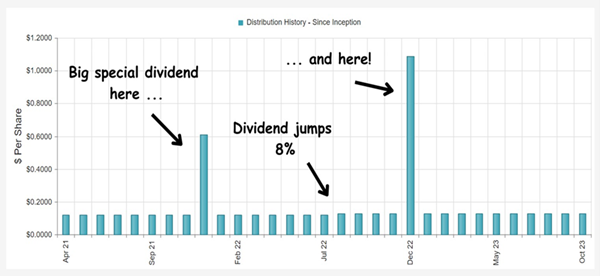

Another of my top picks for 2024 kicks out a current yield that almost doubles ENB’s 7.7%. It’s a smartly run bond fund that pays dividends monthly, recently raised its payout and has dropped some hefty special dividends on investors, too.

A “Once-in-a-Generation” 14% Dividend Opportunity

Source: CEF Connect

What’s more, that immense payout is delivered by a manager who Morningstar previously named Fixed Income Manager of the Year, and who has also been inducted into the Fixed Income Analysts Society Hall of Fame.

To say he knows the bond world is an understatement—and now we can get him working for us. Don’t miss this opportunity. Click here to learn more about this 14%-yielding income play and get a free Special Report revealing my latest research on it.