A couple weeks ago, on May 3, BlackRock, the world’s largest investment firm, did something that will send a shockwave through our favorite high-yield investments: closed-end funds (CEFs).

The result is likely to be higher prices for CEF investors in the future—and even steadier dividends, too. Most folks missed this change, but it’s only a matter of time until it makes itself known. We’re already seeing it kick in with some of these high-paying funds.

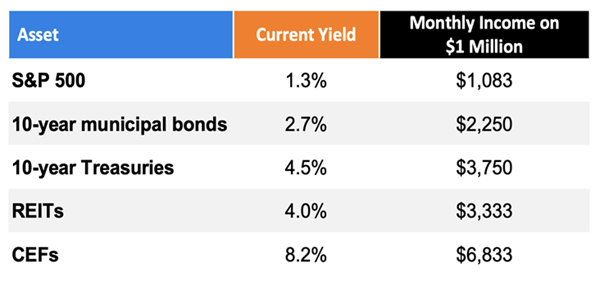

Before we go further, let’s be clear on what we’re talking about: The $400-billion universe of CEFs currently yields an eye-popping 8.2% on average.

How is that possible? Well, remember that the stock market has returned about 8.5% on average over the long term, and corporate bonds now yield about 8%, so there are plenty of places for CEF managers to get returns that can maintain those 8%+ payouts. That’s one reason why income investors, particularly the wealthy, love CEFs.

As you can see above, CEFs are far ahead of stocks, municipal bonds, Treasuries and real estate investment trusts (REITs) on the yield front, even though these funds invest in all of those assets. So how is this possible?

There are many ways CEFs can yield more than the assets they hold, but the critical factor is the discount to net asset value (NAV, or the value of a CEF’s portfolio).

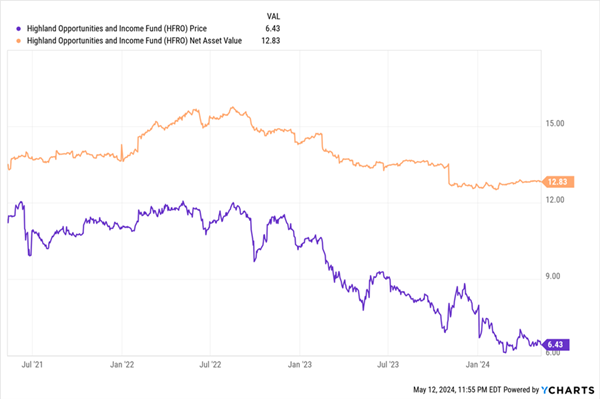

Consider the Highland Opportunities and Income Fund (HFRO), a 7.2%-yielding CEF with $500 million in assets. That yield sounds unsustainable until we dig deeper.

HFRO’s Market Price Trails Far Behind Its Portfolio Value

As you can see, HFRO trades at $6.43 per share (the purple line), but its assets are worth $12.83 (orange line). That means the fund trades at a jaw-dropping 49.9% discount to NAV. It also means that HFRO’s 7.2% yield (based on its market price) is just a 3.6% yield on NAV. That’s important because yield on NAV is what management needs to get to maintain payouts to investors.

In other words, thanks to HFRO’s huge discount, we can get a 7.2% cash flow on our investment, but the fund’s managers only need to earn 3.6% to cover it.

Source: CEF Insider

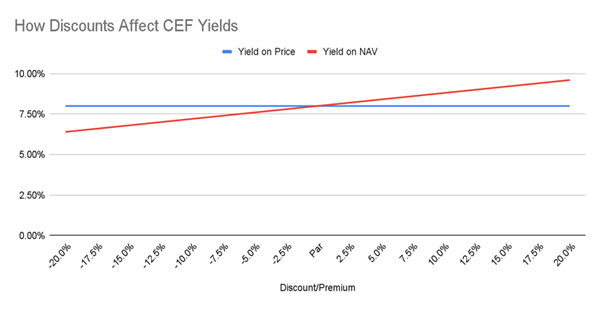

To be sure, HFRO is an extreme example, as CEF discounts rarely go lower than 20%. But the math on this (and all yields on NAV) is simple: a fund that pays 8% only needs to earn 6.4% on its assets if it has, say, a 20% discount. That’s a lot easier than 8%! In addition, investors who buy when a discount is wide can, of course, sell later at a profit, after the discount has narrowed.

Before we go further, note that I’m not recommending HFRO now, but that’s not the case with some other CEFs. Here I’m speaking of those managed by BlackRock. Let’s talk about those now, because they’re at the heart of that shift I mentioned earlier.

BlackRock’s New “Discount Leash”

In a dryly worded press release published on May 3, BlackRock did something that’s likely to have a positive impact on its own CEFs. And, because of BlackRock’s size ($10 trillion under management), this move will likely encourage other CEF managers to follow in its tracks.

BlackRock does have a history of allowing its funds to repurchase shares when they trade at a discount, but this latest move is more targeted than before.

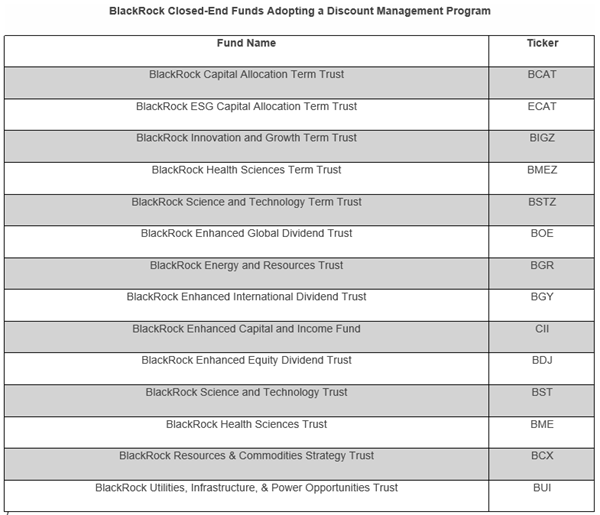

The firm says it will begin repurchasing shares of 14 of its 50 CEFs if their discount to NAV is above 7.5% on average during a three-month measurement period. What’s more, the firm will buy back those shares from investors at a higher price than a 7.5% discount to NAV, offering investors who take up the offer the prospect of instant gains.

The share-buyback plan has launched for the following funds, three of which, the BlackRock Science and Technology Term Trust (BSTZ), its sister fund, the BlackRock Science and Technology Trust (BST) and the BlackRock Enhanced International Dividend Trust (BGY), are holdings in our CEF Insider portfolio:

Source: BlackRock

The bottom line? BlackRock’s buybacks should limit how low these funds’ discounts will go. If the market is efficient, they shouldn’t drop much further than 7.5%.

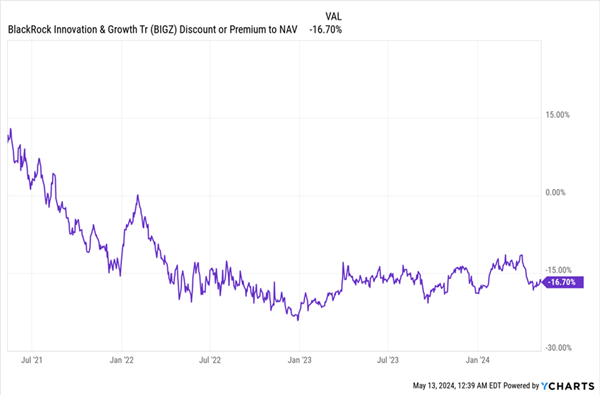

Of course, life is messy and complicated, so these funds might not see their discounts disappear as fast as they should. The BlackRock Innovation and Growth Trust (BIGZ) is an example.

A Perennial Discount—For Now

BIGZ is still trading at a big discount after the announcement, which was in May. In fact, its discount is where it’s been for two years now.

While that made sense before the announcement, it doesn’t anymore, so anyone who buys BIGZ is looking at higher odds of big capital gains on top of the fund’s 8.1% yield. BlackRock’s move will also likely entice other investors to buy BIGZ shares, putting further upward pressure on the price. Until then, those of us who hold the fund now will happily continue to collect its 8.1% dividend.

4 “AI-Powered” CEFs (Current Yield: 7.8%) Set to Soar as Buybacks Take Off

Sitting right in the tracks of this pickup in CEF buybacks are the 4 tech funds I’ve hand-picked for us to reap huge dividends from the AI megatrend.

All four of these tech-driven income plays boast unusual discounts. As buybacks accelerate, those discounts will bubble away like water on a stovetop, driving price gains on top of these funds’ big 7.8% average dividends.

That, of course, comes in addition to the big gains I’m calling for as AI supercharges the economy in the years ahead.

The time to buy these 4 funds is now. Click here and I’ll tell you more about this special “AI-Powered” dividend opportunity and give you a downloadable Special Report revealing the names and tickers of these 4 high-paying funds.