If you’ve been investing long enough, you’ve no doubt run across the 60/40 portfolio. Maybe you’ve used this approach yourself. Or maybe your financial advisor told you about it (it’s an advisor favorite!).

As the name suggests, the 60/40 portfolio is simply a portfolio that seeks to automatically balance risk by holding 60% in stocks and 40% in bonds.

It sounds sensible enough, but history shows that people who invest by this rule have been leaving a lot of money on the table for a long time:

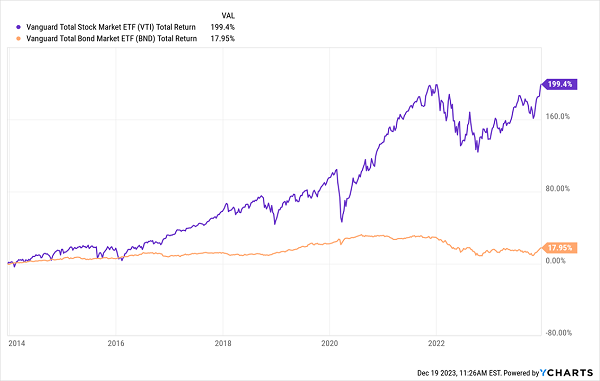

60/40 Portfolio Pays Too High a Price for Low Volatility

One quick glance at US stocks, seen here in purple through the Vanguard Total Stock Market ETF (VTI), and bonds, in orange through the Vanguard Total Bond Market ETF (BND), shows a problem. One of these funds is sleeping on the job.

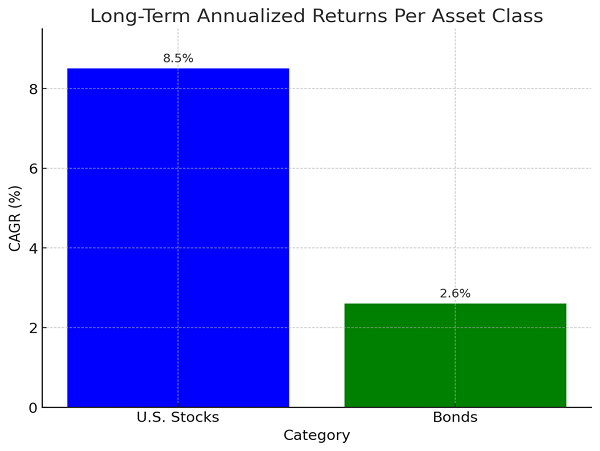

The problem is bonds have had about a 2.6% annualized return over the long term while US stocks have had an 8.5% annualized return over the long term.

Source: CEF Insider

First, this should not shock anyone. Bonds are supposed to return less over the long term—after all, you invest in them to get income. But income is very valuable to many investors, so it tends to have a lower overall return over the long term. The inherently higher risk of US stocks, on the other hand, produces bigger returns.

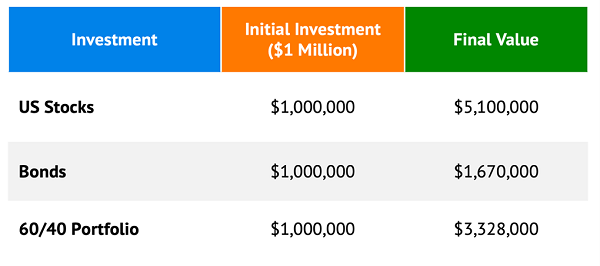

The math here is simple: if we put $1 million in US stocks and wait two decades, we would have $5.1 million in assets, going by the historical returns above. That’s obviously a lot more than the $670,000 profit we’d get by putting that money into bonds. Clearly, a broad bond portfolio is going to wear down our profits, which is why this happens.

The 60/40 portfolio has resulted in a profit, but a profit that is smaller than the stock-only portfolio by an eye-watering $1,772,000!

By putting a heavy weighting toward bonds, we have literally left nearly $2 million on the table in a decade; the longer you devote yourself to the 60/40 portfolio, the more money you’re missing out on.

The Liquid Alternative

The problem with stocks is, well, what if you can’t wait a decade? What if you need income now? There is a simple solution: closed-end funds (CEFs).

While the 60/40 portfolio is the old idea—it’s been around for more than 50 years—of how to get income (by sacrificing total returns), CEFs are a much better idea: turn capital gains into a reliable income stream.

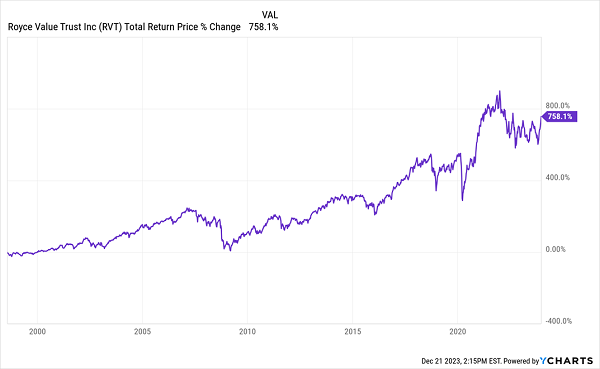

Take, for instance, the 8.3%-yielding Royce Value Trust (RVT), an equity CEF that was launched back in 1986 and has been delivering income ever since.

RVT Converts Stock Gains Into Income

Due to RVT’s high yield, you see your profits in the form of dividends that, in the case of this fund, are paid out monthly.

RVT is no fly-by-night shop, either. Not only has the fund’s history spanned nearly four decades—it was launched back in 1986—it’s one of the larger equity CEFs out there, managing over a billion dollars in assets for investors who can buy and sell their shares whenever they want.

That’s a clear benefit of investing in RVT but here’s the thing: I don’t think this is the best CEF on the market right now. There are literally dozens of better ones. But sometimes it is a strong buy, like when its price goes to a sudden, steep discount to net asset value (NAV, or the value of its underlying portfolio).

Right now isn’t quite that time: even though the fund’s discount sits at 11.8% as I write, it’s actually been cheaper this year, hitting a low of 14.5% at the end of May.

That makes RVT not a bad pick today, but as I write this, about 90% of CEFs trade at discounts, so we’ve got plenty of choices in the bargain bin!

The key takeaway is that once you peer into the CEF universe, you begin to see opportunities not just to capture the profits that 60/40 investors miss. You’ll also discover how to create a diversified portfolio for all markets, as CEFs come from all kinds of sectors, while delivering average yields over 7%.

So let’s toss the 60/40 portfolio in the dustbin—and instead look to the superior future income and gains that CEFs can provide.

Grab These 5 Monthly Paying “Bargain-Bin Dividends”—Yielding 9.2%—NOW

When I said there were hundreds of better CEFs out there than RVT, I meant it. Because my top 5 monthly paying CEFs all rank much higher than this fund, in both yields and upside.

In addition to dropping dividend cash into your account every 30 (or 31) days, these 5 reliable income plays yield an outsized 9.2% today.

Drop $100K into them now and you’ll pick up a cool $767 a month. $500K gets you $3,833 monthly.

And on it goes.

Here’s what really puts these 5 monthly payers laps ahead of the 60/40 portfolio: you don’t have to sacrifice gain potential to tap into their high payouts: all 5 are cheap—so much so that I’m calling for 20%+ price upside over the next 12 months!

Don’t miss your chance to buy these 5 high-yielding monthly payers while they’re still cheap. Click here and I’ll tell you more about them and give you the opportunity to download a FREE Special Report revealing their names and tickers.