There’s one word that strikes terror into the hearts of mainstream investors: leverage.

But it really shouldn’t—and today I’m going to show you how to make sure you’re using leverage the right way, while minimizing your risk and tapping into some of the biggest gains (and dividends!) available to us today.

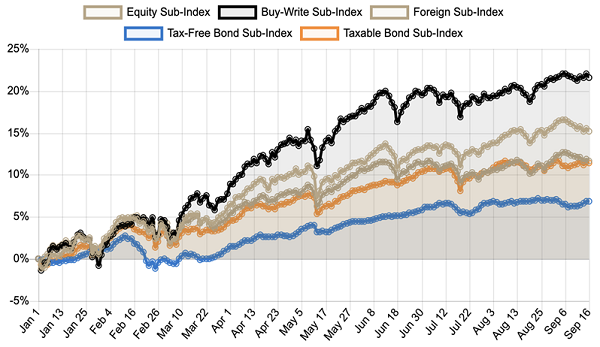

As you probably know, closed-end funds (CEFs) commonly use leverage to amp up their investment returns (and their dividends, which yield 6.5%, on average, as I write this). That’s fed their strong gains this year, as the Federal Reserve has kept interest rates low:

CEFs on a Tear

Source: CEF Insider

The CEF Insider Index Tracker has shown double-digit gains everywhere except in municipal bonds (which is normal, as we buy munis for their stability and tax-free dividends).

And tell this little factoid to the indexing crowd: while these folks preach that active management can never beat the market, equity CEFs are throwing off total returns that outperform the S&P 500’s 20% year-to-date gains. What’s more, CEF owners are getting more of their return as dividend cash (the equity corner of our CEF Insider portfolio yields 7.1% as I write this, compared to a measly 1.3% for the S&P 500).

And CEFs that judiciously apply leverage are set to see stronger gains in 2022, 2023 and beyond. To get at why, and the best way to manage the leverage in your own CEF investments, let’s take a quick look at history. (And note that at CEF Insider, I carefully manage levels according to my strict standards for you, so you can rest assured it’s at the right level for maximum gains and minimum downside in a pullback; more on this shortly.)

A 90-Year-Old Tale

The cloud hanging over leverage stretches back to the crash of 1929 and tales of stockbrokers who borrowed too much cash before the collapse, then leaped out their office windows. This piece of investing folklore has had a long shelf life on Wall Street.

But that was 90 years ago: today, blow-ups due to overleverage are rare, thanks to regulation, more experienced management teams and the availability of incredibly deep research.

You can also make leverage safer by combining variable- and fixed-rate loans. And believe it or not, savvy contrarian fund managers can add even more safety by hedging through derivatives (even though “derivatives” is yet another word that makes many folks quake).

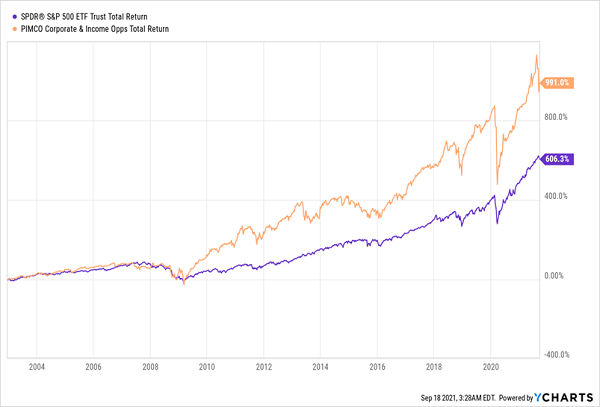

This is exactly what one of the most successful CEFs of our time, the PIMCO Corporate & Income Opportunities Fund (PTY), has pulled off, posting a 991% total return since inception, thanks to the reams of data and exclusive market access enjoyed by its parent company, PIMCO.

PTY Turns Leverage Into Massive Profits

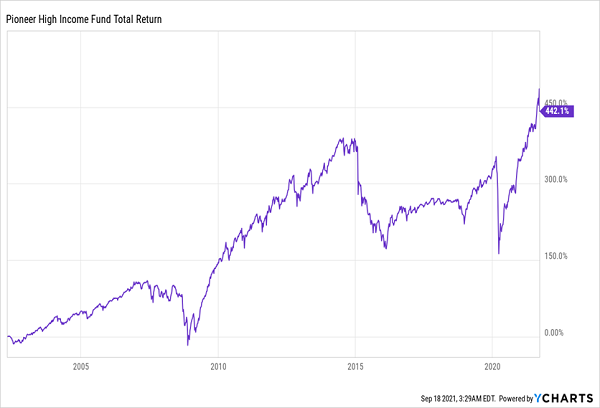

Note, however, that mainstream investors don’t always catch on to this approach, which is something we can use to our advantage. Consider the Pioneer High Income Trust (PHT), which used a complex credit portfolio to earn market-busting returns until the start of 2015, when the fund declined. It then roared back from the start of 2016:

Demand Falls Off a Cliff, Comes Roaring Back

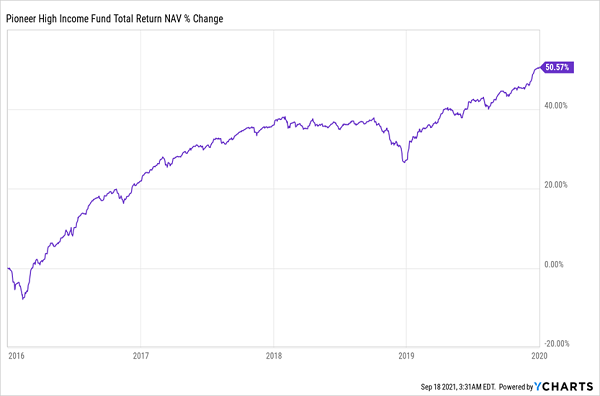

The takeaway here? Buy at the right time and be a contrarian going against where the broader CEF market is. To do this, you need to look closely at how a fund’s actual portfolio is doing; with PHT, its return was impressive from 2016 to the start of 2020:

A Stunning Recovery

This strength is even more impressive when you consider that the Fed raised rates from 2015 to the start of 2019, and rising rates are supposed to work against leveraged funds because they raise their borrowing costs. But PHT soared anyway, which is our first clue that rising rates are often no big deal for CEFs; on the contrary, they often signal a buying opportunity.

That brings me to today’s situation.

At the start of the pandemic, the Fed reacted swiftly to keep borrowing costs low, making leverage incredibly cheap for CEFs. That’s been great for these funds over the last 18 months, of course, but what about when the Fed raises interest rates, which could happen as early as late next year?

If such a scenario unfolds and causes a selloff, it will be a tremendous opportunity for us. The most aggressive expectations are that interest rates will rise from around 0.3% now to less than 1% in 2023, and even the most daring economists see rates staying near 2% for the next several years after that. And 3%? That’s maybe a decade away.

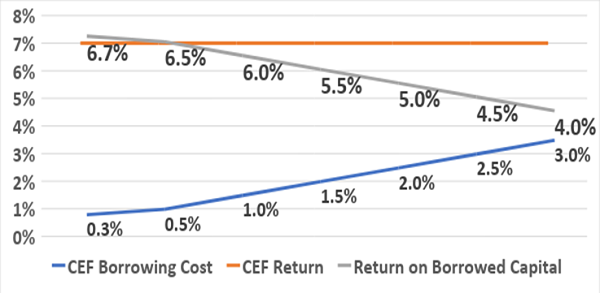

Still, what if they’re wrong and borrowing costs climb more quickly? Well, the returns CEFs will get from borrowing money will still remain positive and investors will still benefit from the leverage, as we saw in the mid-2000s and late 2010s. Let me explain this in a chart:

Lower, but Still Positive, Returns

Source: CEF Insider

As you can see, as long as a CEF’s return on the capital it’s borrowing exceeds its borrowing costs, it’s earning a profit off of these loans. Here I’m assuming 7% overall returns, which is far below the average for equity and taxable-bond CEFs over the last decade.

In other words, even if borrowing money isn’t as lucrative as it used to be, it’s still very lucrative.

This is a good reason why fears of the Fed when interest rates do go up are likely to be pretty minimal: the higher rates will still be very low, by historical standards, and returns in the market are likely to be much higher (again going by the history).

With all that in mind, we can clearly see that any rate-driven worries over CEFs are likely to widen their discounts and, as they do, inflate their dividends. When that happens, we’ll be ready to jump in.

Yours NOW: 5 Bargain CEFs Yielding Up to 8% (with 20% Upside!)

Of course, we really love it when CEFs take their gains—leverage-driven or not—and hand them to us as dividends. And CEFs do this for us on the regular, with outsized payouts of 6% 7%, 8% and higher, often paid monthly.

And how’s this for the safety of investing in CEFs: according to my latest research: 96% of CEFs that have been around for 10 years or more made money in the last decade! And when you cut out CEFs in the energy sector, that percentage jumps to 99%.

A 99% win rate! It just doesn’t get any more reliable than that.

The bottom line is that if you’re investing for the long haul, you must have CEFs in your portfolio. These funds, with their high dividends, proven safety record and unusual discounts are the key to generating a safe, high income stream, no matter what the economy throws at us.

I’ve hand-picked 5 CEFs I see as perfect buys for you right now. This 5-fund “instant portfolio” contains CEFs from across the economy. They yield 6.5%, on average (with the highest payer throwing off an outsized 8% payout). Plus, all 5 are trading at bargain valuations now (a situation that won’t last in the zero-rate world we’re still living in).

The bottom line? I’m calling for 20%+ price upside from each of these 5 funds, in addition to their huge dividend payouts.

I’ve put everything you need to know in an exclusive investor report that I want to share with you now. Go here to read it and get full details on these 5 unsung 6.5% income plays.