Thank you, bear market. Thanks to a terrible 2022, we have four dirt-cheap dividend payers dishing up to 9%.

These are cash cows I’m talking about. Companies that gush free cash flow and shovel it back to us in the form of big yields.

Earnings are accounting numbers. Cash flow is real life.

And it’s not out of deals, either—in fact, over the past few days, I’ve kept increasingly close watch over a four-pack of cash cows with high yields of up to 9% and deliciously low prices.

But given a still-dangerous market environment, we need to focus on quality. That means we want to focus not just on earnings, but cash.

Show Us the Money

Cash is king for us dividend investors, for three reasons:

- Cash pays for dividends. Dividends are paid out of real cash, not paper profits.

- Cash pays for buybacks, too. Stock repurchases (when done right) help keep shares elevated. And like dividends, they also come out of cash. Thus, a company with a lot of cash can pull levers to deliver income to shareholders and improve the price of their stock.

- Cash don’t lie. Wall Street accountants can “adjust” just about anything—earnings, EBITDA, even revenues. But it’s next to impossible to adjust, modify, or otherwise fudge cash.

Given all that, it’s vital to consider cash when valuing companies in a rocky economic and stock-market environment. And it’s fair to say that, even when accounting for the recent short-term bounce-back in stocks, 2022 remains a rocky environment.

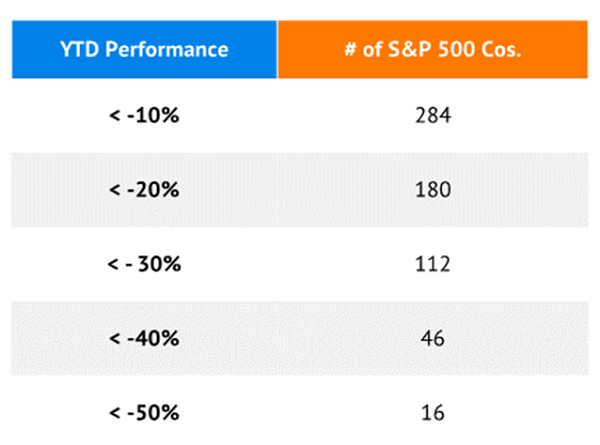

Many, many stocks remain light-years behind the 8-ball.

More than half the S&P 500 remains in the red, and more than a third is off by more than 20%. Sixteen components of this blue-chip index are still trading for half of what they were at the start of 2022.

No good for current shareholders, of course, but a great starting point for bargain hunters like us—as long as we’re careful, and as long as we’re searching through the right lens (i.e., cash).

After all: We want to make sure we’re getting value stocks, not just cheap stocks.

Cash is cash. You can’t really “adjust” it. And free cash flow is especially useful because it tells us how much a company has made after it has paid for things like maintaining and growing the business.

Good news here: There are dozens of high-yielding dividend payers that are trading at tantalizingly cheap P/FCF ratios right now—and thus improving our chances of solid price appreciation over time. Today, I want to highlight four of the most interesting opportunities that are offering us yields of between 4.6% and 9.0%.

Let’s dig in.

3M (MMM)

Dividend Yield: 4.6%

Forward Price/FCF: 9.7

3M (MMM) was once an industrials darling—virtually untouchable thanks to its vast array of products and patents. But the stock simply hasn’t been itself since the U.S.-China trade war blunted the stock in early 2018.

MMM hasn’t seen a new high since.

3M Shares Wallow as Dividend Growth Wilts

More recently, MMM has been weighed down by litigation surrounding perfluoroalkyl and polyfluoroalkyl substances (better known as PFAS) and its Combat Arms Earplug. Particularly worrisome is that free cash flow is off 35% year-over-year so far in 2022, including a 16% dip during the most recent quarter.

MMM shares are off 24% YTD and by nearly a third since June 2021. But while it has gotten cheaper, it’s still not a screaming value—the roughly 10 forward P/FCF is certainly appealing, and the 4.6% yield is high.

Meanwhile, this industrial is projecting scarce earnings growth over the next couple of years. That means there’s little reason to believe 3M’s multiyear trend of slowing dividend growth—and slowing buybacks—will reverse course.

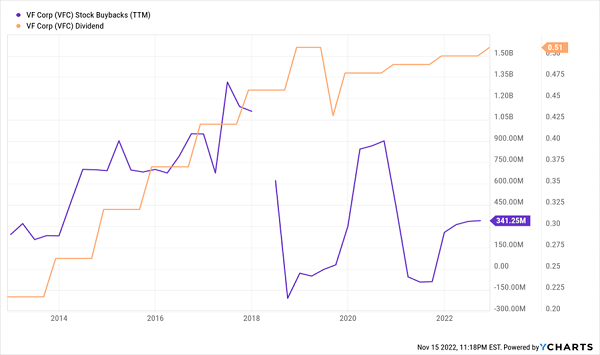

VF Corp. (VFC)

Dividend Yield: 6.2%

Forward Price/FCF: 5.2

VF Corp (VFC) is the parent company of apparel brands including Vans, North Face, Timberland and Supreme. And as I mentioned recently, while the company lowered its 2023 guidance, “this could be an enticing (albeit risky) income-and-eventual-growth play for investors playing the really long game.”

While FCF dipped to $619 million in fiscal year 2022, BofA Global Research estimates that will jump back to nearly $1.1 billion in FY23, then more than $1.2 billion in FY24 and FY25. It’ll do that in part thanks to cost cuts, including eliminating 600 corporate positions.

VFC doesn’t have a history of consistent buybacks, but it has proven it’s willing to spend. My bigger concern is the flattening dividend growth of late. If its cash-flow issues improve as projected, any signs of resurgent generosity should be looked at as an extremely positive signal.

VF Corp Needs to Ratchet Up the Shareholder Spending Again

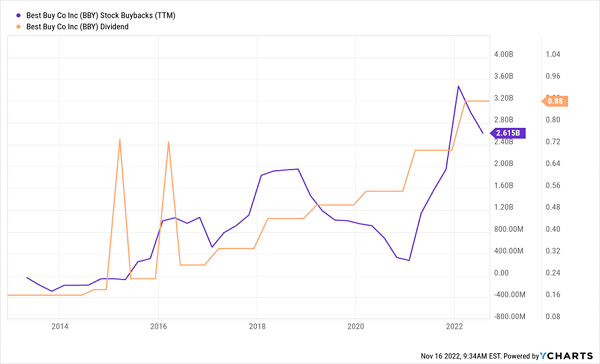

Best Buy (BBY)

Dividend Yield: 4.7%

Forward Price/FCF: 6.7

Best Buy (BBY) is the retailer that just wouldn’t die. Walmart (WMT) couldn’t kill it, nor could its slightly upscale cousin, Target (TGT). Even amateur astronaut Jeff Bezos and his Amazon.com (AMZN) juggernaut couldn’t keep this tech-gear chain down forever.

Now? It’s not just surviving, but thriving as one of the better-looking dividend plays in retail.

BBY is indeed fighting headwinds, including difficult comps. The COVID WFH supply rush is over, and the company is projecting an 11% comparable-store sales decline for the full year. Free cash flow per share for 2022 is expected to plunge by nearly 75%.

That’s OK. FCF is expected to bounce back to more normalized levels in 2023 and 2024, by 250% (to $9.16/share) and 25% (to $11.46/share), respectively. Meanwhile, the generous dividend still only accounts for $3.52/share annually. That should allow Best Buy to keep the pedal down on raising its payout and throwing more money at buybacks.

Best Buy Keeps Tossing More Cash at Shareholders

The sub-7 forward P/FCF is hard to ignore, too.

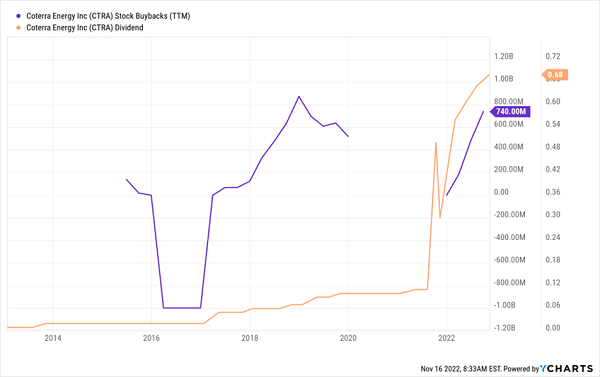

Coterra Energy (CTRA)

Dividend Yield: 9.0%

Forward Price/FCF: 4.1

Houston-based oil producer Coterra Energy (CTRA) is a major player in Texas’ and New Mexico’s Delaware Basin, boasting 234,000 acres. It also has acreage in the Marcellus and Anadarko basins.

Has Coterra benefited from a spike in energy prices over the past few years? Absolutely. But this is also very much a company that has “found its groove” operationally. Truist’s Neal Dingmann recently posted a glowing recommendation, but the money shot (to me) was this:

“The stable production in the Marcellus, Delaware and Anadarko, coupled with design improvements to pad construction and extended drilling laterals help ensure continued, solid cash flows,” he says, adding that “between the ~$500MM remaining on its buyback authorization, and a continued fixed/variable dividend CTRA has the potential to deliver a $1/share shareholder return through 1Q23.”

Listen. At the end of the day, CTRA is an energy stock, which means it’s beholden to energy prices, which don’t stand still. That means it’s a difficult play for retirees that want stable, consistent dividends—again, part of Coterra’s payout is intentionally variable—and buybacks might not always be there.

CTRA Shareholder Rewards WILL Fluctuate

But Coterra is very much emerging as an income/shareholder yield play for those who do want to dabble in the energy space. A low forward-looking FCF valuation sweetens the pot.

Sky-High Dividends For Decades

Our income generators need to be pointed in the same direction as long-term trends. That’ll ensure our big yields today will become even bigger yields tomorrow, and that our nest eggs will grow right alongside my payouts.

That’s a quality you’ll find in bulk in my “Perfect Income” portfolio.

The “Perfect Income” portfolio features some of the most generous, yet stable, dividend investments I’ve found. And while they typically trade at lofty valuations during normal market conditions, Wall Street has thrown the baby out with the bear-market bathwater, giving us a rare opportunity to buy even more shares on the cheap.

The best thing about this portfolio? It’s a set-it-and-forget-it strategy.

- No complex day-trading strategies.

- No gambling on high-risk options contracts.

- And certainly no penny stocks.

This is just simple buy-and-hold investing—done right.

Let me show you the stocks and funds I believe could stabilize many retirement portfolios. Even better, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Click here to get a copy of my Perfect Income Portfolio report … and a few other bonuses!