Jerome Powell is preparing a wonderful holiday income dish for us.

The economy is running hot and he’s cutting rates anyway. Oh baby! “Lame Duck Jerry” is finally starting to cook.

But vanilla investors aren’t having it. They’re sprinting from the table! Recession fears dominate the headlines, even though the data scream otherwise.

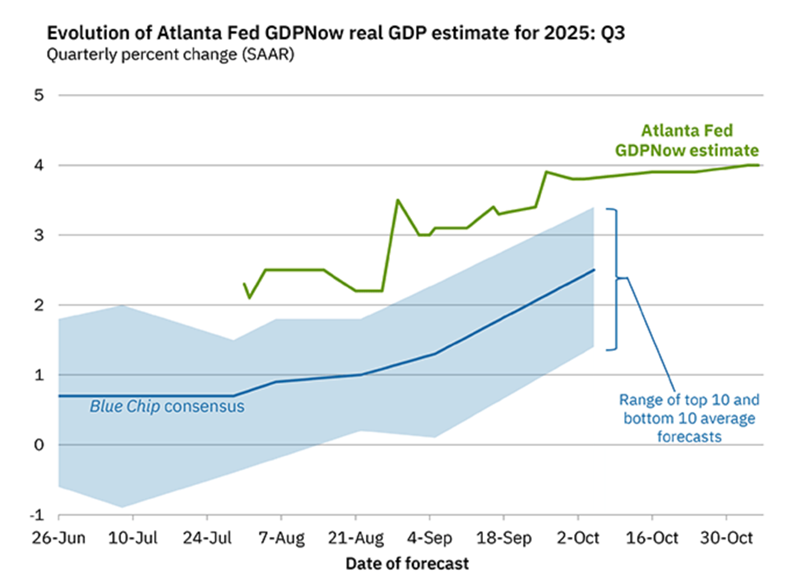

The Atlanta Fed’s thermometer has GDP at a sizzling 4%. Four percent! In today’s AI-fueled, efficiency-obsessed economy, the old recession playbook simply doesn’t apply.

AI is eating traditional white-collar work. Business models from 2019 no longer apply in 2025. Some sectors are struggling while others hit new strides. It’s a winners-and-losers economy—and investors are still squinting at discolored, outdated AAA maps!

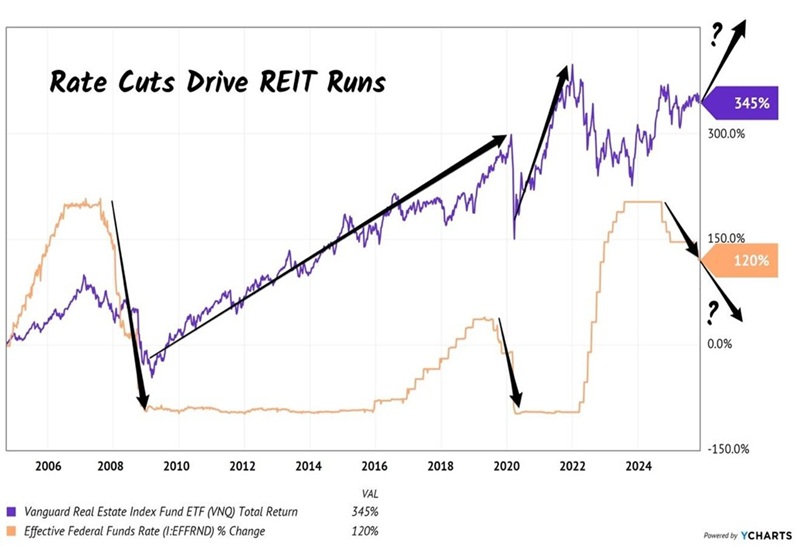

But one maxim still rules: As rates fall, REITs rise.

Over the last 20 years, we’ve had two major rate-cut cycles. Both kicked off monster REIT bull markets. The new cycle could be the biggest yet because unlike 2008 or 2020 the economy is growing, not shrinking.

Rate Cuts Kick Off REIT Bull Markets

Meanwhile, that “safe 4%” money-market yield everyone fell in love with? It’s going away. Every Fed cut pushes more idle cash into the market, searching for yields with actual staying power. REITs, obligated to hand 90% of their income to us, thrive in times like these.

And select mortgage REITs (mREITs) are set up for big payouts and price gains. These financial “landlords” own government-backed mortgages that rise in value as long-term rates fall. This is an interest-rate trade rolled up in a dividend wrapper. Tasty.

While vanilla investors fret over imaginary recessions, Annaly Capital (NLY) licks its chops. Few companies benefit more from falling rates than NLY.

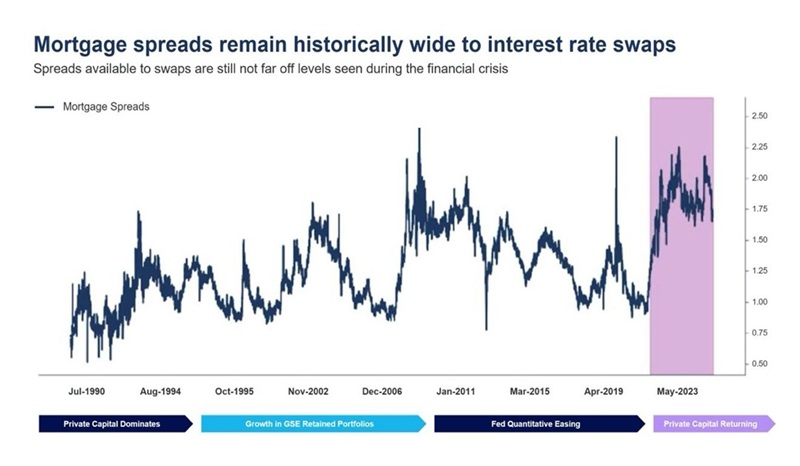

And we’ve only seen mortgage spreads this wide a few times in the last quarter-century. Each time, NLY rallied.

Why? Annaly leans in when others panic. Management buys high-quality government-backed (“agency”) mortgages when spreads explode. It buys low then waits for yields to normalize, which boosts book value. So, of course, its stock takes off.

The normalization has already begun, with mortgage rates falling from north of 7% to the low 6s. Every tick lower boosts the value of Annaly’s portfolio (yields down, bond prices up!). And these are Fannie and Freddie-guaranteed bonds (“agency” paper)—no credit risk.

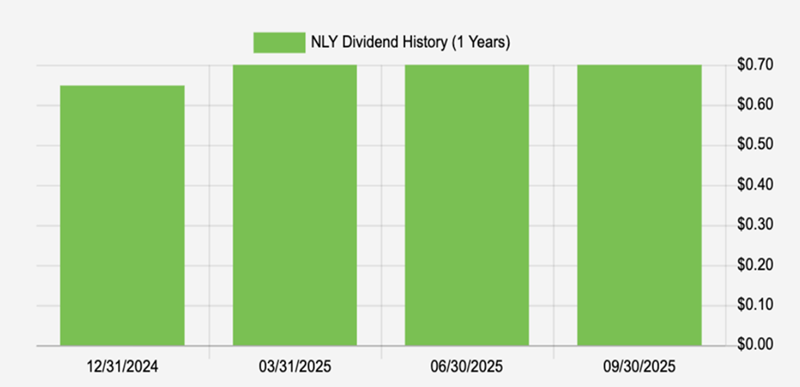

The company already has more than enough core earnings to cover its dividend ($0.73 in earnings per share versus $0.70 paid out last quarter). But with rate cuts shrinking NLY’s cost of funds and fattening its net interest margin, more earnings could boost NLY’s 12.9% dividend again!

Annaly’s Big Quarterly Dividend

But please note, not all mREITs are created equal. It’s a complex business requiring specialized expertise. Fortunately, Annaly is a big, seasoned operator holding guaranteed agency paper. Other mREITs often hold sketchy commercial mortgages—office loans tied to struggling tenants and illiquid credit bets. Why take that risk when you can have Annaly?

Bottom line is that rate cuts create winners and losers, just like the 2025 economy has. Don’t overthink it. Buy the proven playbook.

My only nitpick with NLY? It pays quarterly, not monthly!

Fear not, monthly dividend fans—this research is for you. Contrary to vanilla Wall Street opinion, it is possible to find elite 8% payouts that are delivered monthly. Here are my favorite 8%+ monthly payers for retiring on dividends.