I have to laugh when I hear people say Jay Powell has been tough on rates. Sure, he’s been talking tough. But when he’s not doing his Dirty Harry act at the mic, he’s been keeping the liquidity party going through the back door!

I call this “Quiet QE.” If you’ve read my articles in the last couple of years, or are a member of one of my premium services, you’ve no doubt heard me talk about it before.

It’s one-half of the opportunity we’re looking at in corporate bonds today.

The other? The arrival of what I call “real” QE, in the form of rate cuts slated to start up in September. Last Wednesday’s cooler-than-expected inflation report sealed the deal.

Let’s unwrap this more, starting with that Quiet QE I just touched on. Because while Jay says he’s been taking the punchbowl away from Mr. and Mrs. Market, he really hasn’t. Jay saw the collapse of Silicon Valley Bank and friends in March 2023 and got spooked.

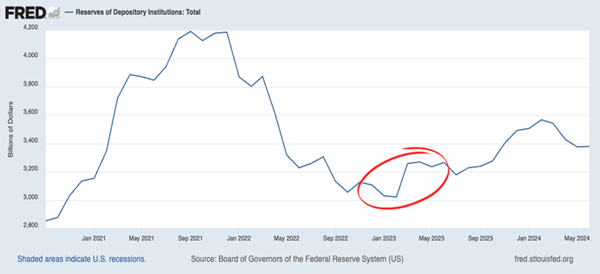

Though few people noticed it at the time, the Fed “pivot” was in: Liquidity would go that low—and no lower. You can see Jay’s change of heart clear as day in this chart of bank reserves:

Forget September’s (Likely) Rate Cut: The Fed Really Pivoted in March ’23

If you had any doubt this was the case, consider what stocks, particularly rate-sensitive tech stocks and crypto, have done since then: They’ve skyrocketed! It’s the exact opposite of what they should be doing if monetary policy were really getting tighter.

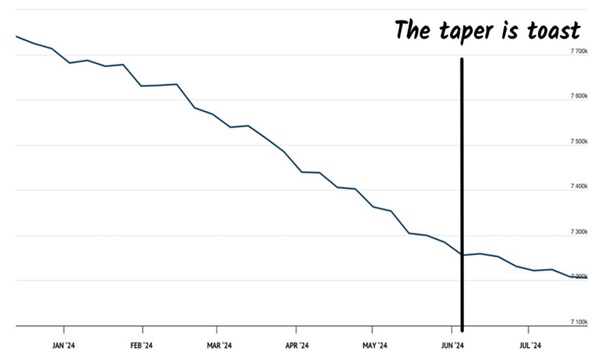

Fast-forward to today and Quiet QE is about to get a lift from overt easing measures. Remember the Fed’s tapering of its balance sheet? Bonds rolled off and were not bought back. This, plus rate hikes, caused the 2022 bear market.

Well, the Fed is nearly finished tapering its balance sheet. The tightening effort has slowed to a crawl and will officially end soon:

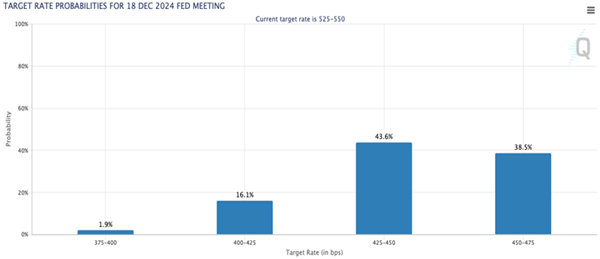

Also, the Fed is about to start cutting rates. The futures markets currently price in four or more cuts between now and December:

Source: cmegroup.com

Quiet QE. No more taper. Rate cuts ahead. This is a great time to be a dividend investor. But what should we buy?

This 14%-Paying Corporate Bond Fund Is a Smart Play on Falling Rates

Luckily there’s one 14%-paying fund that’s perfect when rates fall: a corporate bond–focused closed-end fund (CEF) called the PIMCO Dynamic Income Fund (PDI).

It’s a ticker members of my Contrarian Income Report service will know: Since we added it to our portfolio in May 2023, it’s handed us a 22.5% return—a big move for a bond fund.

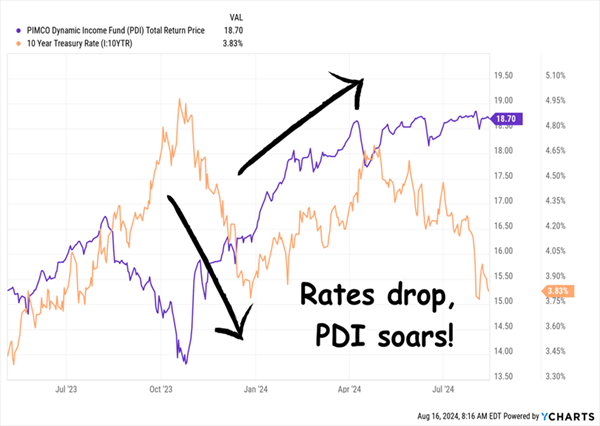

PDI Bounces With Bonds

Sure, maybe we were a bit early for the rate peak that arrived last fall, but that’s okay—we still reaped that nice 22.5% return, mostly in dividends. More important, we’re nicely set up for the next leg down in rates.

Falling rates drive up bond prices (particularly the prices of long-duration high-yield bonds like those in PDI’s portfolio, with an effective maturity of 5.44 years) because these look very good compared to the lower-yielding corporates issued as rates fall.

PDI’s “Beast” Tells It Like It Is

This ability to “surf the rate tides” is why we look to a human-managed CEF, as opposed to an algorithm-driven ETF to make our bond buys.

In the cozy world of bonds, well-connected managers get the first call when the best new issues are released, and there are few better connected than PDI’s Dan Ivascyn, dubbed “the Beast” by his colleagues for his long record of success.

Another thing we love about Ivascyn: He speaks his mind. He recently told Reuters he thinks the market is getting ahead of itself on rate-cut expectations, that there will only be one 25-basis-point reduction in September, and “future meetings will be live.”

We love it when managers say what they think and don’t simply “talk their own book.” Since high-yield bonds would stand to gain on a fast rate decline, Ivascyn could have simply been a cheerleader for that possibility. But he wasn’t. He now says he’s looking for opportunities in “safer parts of the credit market.”

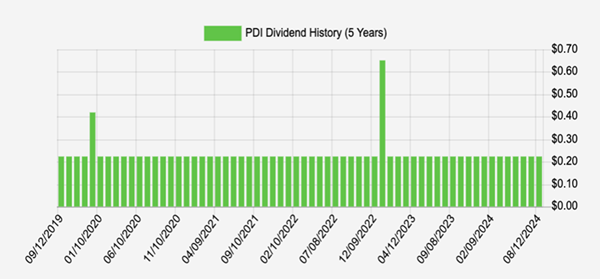

Meantime, that 14% yield translates into a sweet, steady (and monthly) income stream for folks “in the know” about this terrific bond fund, with special dividends thrown in:

Strong Income Stream About to Get Stronger

Source: Income Calendar

Another plus? PDI, like many CEFs, uses leverage to boost its returns, to the tune of roughly 37.5% of its portfolio. As rates fall, its borrowing costs will, too, boosting its overall return and further supporting its dividend.

A Timely “Dip Buy”

To be sure, PDI isn’t exactly cheap now, trading at a 10% premium to net asset value (NAV, or the value of its underlying portfolio). That’s $1.10 for every $1 of assets! But bear in mind that PIMCO holds legendary status in the CEF world, and it’s common for its funds to trade above NAV.

Even so, that premium is just a bit rich for us, so we’re putting PDI on our watch list (or ranking it a hold if you already own it). We’ll pick up this terrific fund on its next dip.

Quick, Tell Me How Much in Dividends You’ll Get in September (Bet You Can’t)

Whether you buy PDI now—and there is a case for doing so, as Ivascyn’s talents go a long way toward offsetting the fund’s premium—or hold off, there’s something else we need to talk about today.

It’s a new “AI-like” tool we’ve built specifically for dividend investors. If you use an “old-school” spreadsheet to track your payouts (or nothing at all!) it’s an absolute game-changer.

It’s called Income Calendar, and if you invest in high yielders like PDI (and I’m guessing you do if you’ve read this far!), you must have it in your “dividend toolkit.” IC tells you when (down to the day) and how many (down to the penny) dividends your portfolio will kick out in the week, month and year ahead.

You can get complete breakdowns by stock, plus a month-by-month calendar giving you a heads-up on earnings dates, ex-dividend dates and other critical periods for every one of your holdings. Instantly!

The ChatGPT of Dividends

Simply enter your tickers into IC (or use one of our “automatic” features to link it straight to your brokerage account in seconds) and you get an immediate monthly income summary.

With IC, you’ll know how much you’ll collect in dividends in September. And October. Heck, even in April 2025.

So long, spreadsheet, hello, extra time. Which you can use to seek out new dividend payers. Or with your grandkids. Or watching sports (hey, we don’t judge, we just try to save you time!)

Now is the perfect time to try Income Calendar, as we’ve just added a bundle of new features, including the ability to link to any brokerage (including Fidelity!) in a few clicks. Plus you now get instant email alerts when you receive dividends, a yield on cost calculation (so you can see the “true” yield on each of your stocks, based on the timing of your original buy) and more.