This market crash has served up some terrific opportunities in closed-end funds (CEFs), many of which are throwing off safe 7%+ dividends today.

Dividends of that size, of course, are critical today, as we look to offset rising inflation. And I think we can all agree that a CD or Treasury will never match a payout like that.

But of course, not all CEFs are set to rise equally as the stock market continues to regain its footing (which I expect it to as we move through the back half of 2022), so we need to be careful about exactly which sectors—and funds—we target.

Which is why, today, we’re going to dive into three corners of the CEF market (including specific tickers), so you know exactly where to put your money in the weeks ahead. Let’s get started with a sector that’s been on fire for the first eight months of ’22 but could be in for a turbulent final few months of the year.

Energy CEFs (Great for Dividends, but Their Discounts Are Deceiving)

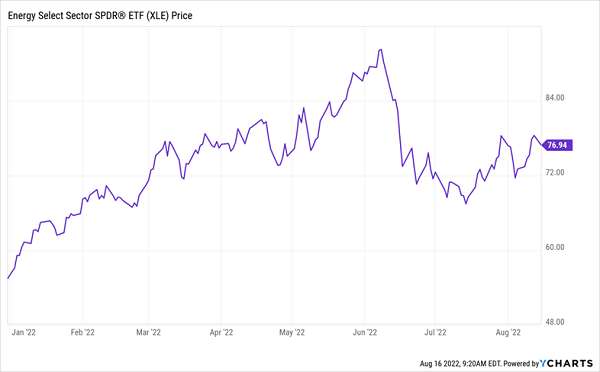

Back in early 2022, you could’ve bought just about any fund holding oil and gas producers and done well. But those gains have been fading as crude prices dipped, as we can see from the drop in the benchmark Energy Select Sector SPDR ETF (XLE) below:

Last Call at the Energy Party

Even though I don’t recommend energy stocks right now, if you do want to hold them, you can get a much higher dividend by purchasing them through a CEF like the ClearBridge MLP and Midstream Fund (CEM), for example. This fund yields 7% and holds a range of cash-generating master limited partnerships (MLPs) that operate pipelines, such as Enterprise Products Partners (EPD), ONEOK (OKE) and Williams Companies (WMB).

So you can grab yourself a nice dividend from CEM and other oil and gas CEFs, but upside is likely to be limited, and you could see a fall in these funds’ prices, due to waning oil prices.

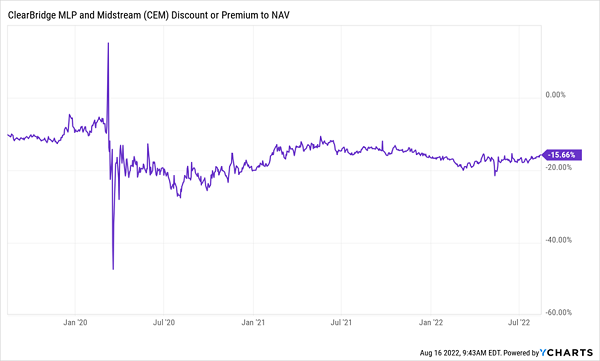

In addition, CEM, like many other energy CEFs, sports a discount to net asset value (NAV, or the value of the investments in its portfolio) that rarely changes: you can buy this one at a 16% discount today, but that markdown has been static for more than two years, lingering in double-digit territory since the COVID-19 crash of March 2020.

CEM’s Stagnant Discount

For market-beating gains in CEFs, we need discounts that shrink, propelling the fund’s share price higher as they do. Persistent discounts like CEM’s, along with the inherent volatility of energy CEFs, is why we don’t hold any of these funds in our CEF Insider portfolio.

Utility CEFs: Good Buys for Stability and Dividends, But Upside Is Limited

A good way to take the other side of the energy trade is through utilities, as many of these firms burn the (suddenly cheaper) fuels pumped by CEM’s master limited partnerships to generate power.

That means big utilities firms like Southern Company (SO) and American Electric Power (AEP) should see bigger profits as energy prices drop. The problem is that the cat is already out of the bag on this trade, which is why premiums to NAV dot the utility space today.

Consider the Reaves Utility Income Fund (UTG), a CEF trading at a 0.2% premium to NAV, compared to a one-year average premium of around 1%. That doesn’t portend a lot of upside. However, lower input costs do make our utility stocks’ (and CEFs’) dividends safer (UTG, for its part, yields around 7% today).

Consumer-Facing Tech CEFs Offer Diversification, Upside and Bigger Payouts

We all know that this selloff has been particularly hard on tech stocks, leaving many priced at attractive valuations. And there are CEFs out there that give you a basket of the best techs, including Amazon.com (AMZN), Alphabet (GOOGL), Microsoft (MSFT) and Visa (V)—the latter of which is more of a tech than a financial stock, due to its advanced payment network.

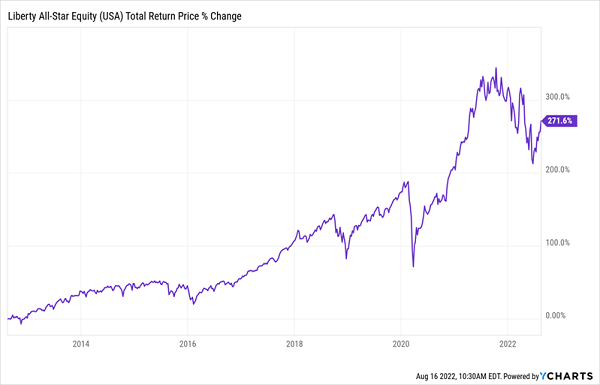

The Liberty All-Star Equity Fund (USA) is a good example. It holds all of the above names and has a lot of overlap with the S&P 500, due to its focus on American large-cap stocks, but it also pays a whopping 9.1% dividend yield. That outsized payout is fueled by management’s active approach to buying and selling stocks at opportune times. It then passes the cash from those sales (along with the dividends it collects on its holdings) over to us.

This strategy has paid off for USA investors: over the last decade, the fund has returned a sweet 272%, including dividends.

Outsized Income and Returns

USA does trade at a 5% premium, but there’s a critical difference between it and the funds above when it comes to valuation: USA’s premium has shot as high as 15% in the last year, and I expect further upside as its premium moves toward that level again, driven by a rebound in the depressed tech market and a continued rise in consumer spending.

Urgent: My 5 Top CEF Buys Are Cheap—and Yield an Outsized 8.6% Today

Sure, USA is a strong fund, but it still trades at a premium to NAV, and we should always demand a discount when we buy CEFs. Especially today, when there are a lot of CEFs out there yielding 7%+ and trading at temporary discounts we can ride to serious price gains.

The 5 “must own” CEFs my team and I have assembled are perfect examples. They yield 8.6%, and are ridiculously cheap—so much so that I’m forecasting 20%+ price upside from each of them in the next 12 months, to go along with their huge dividends.

That’s a forecast 28.5% total return, including your monthly payouts!