If tariffs really are going to crush the economy, someone forgot to tell the nation’s small businesses! Truth is, these “mom-and-pop shops” are thinking big—and growing.

And we’re here to play this “disconnect” for sweet 8.8%+ dividends.

Small Biz Bullishness by the Numbers

According to the latest NFIB survey, in July, 13% of small business owners said their businesses were in “excellent” shape, a five-point gain since June. And 52% said they were in “good” condition (a three-point rise). Only 4% said “poor,” a three-point drop.

The good times look set to keep rolling for these businesses, too: 36% of owners said they see higher sales ahead. That may not sound huge, but it’s a 14-point jump since June—a big swing in just one month.

This report is no outlier: The CNBC SurveyMonkey Small Business Confidence Index tells us that in Q2, 46% of small-business owners said the economy is excellent or good, up sharply from just 30% in the previous quarter!

Small Businesses Are the Real AI Winners

A big slice of that enthusiasm can be chalked up to two letters: AI.

Ask any small business owner about the biggest challenges they face and they’ll likely all say finding good workers. AI helps with that—and it’s a lot cheaper than humans, too!

A few months ago, Shanell Camp, owner of Shaded by Shanell (an up-and-coming beauty brand) explained her excitement to me about ChatGPT, her “go to” resource for brainstorming, marketing help and more.

“I even named him Ace. We are in a full-blown work relationship. That is my best friend, my assistant, my email writer—everything. I use ChatGPT for a lot of stuff in business and it’s very, very helpful.”

Shanell and Ace are a dynamic duo. Together they’re taking on giant beauty brands with much deeper pockets. And they’re doing it without Shanell having to hire.

The numbers back up her AI excitement. According to the US Chamber of Commerce’s Impact of Technology on Small Business Report, 58% of small businesses use the tech. That’s a big jump from 40% last year and 23% in 2023.

More AI use is locked in, as 80% of owners say it will help them grow future sales.

Lower Costs + Higher Sales = Rapid Expansion

You and I both know that when businesses feel bullish, they do one thing: expand. That, of course, requires capital. Where are they going to get the cash?

For years, they’ve bypassed stingy banks and looked to business development companies (BDCs). Bottom line here is when small business cooks, BDC profits sizzle!

Let’s look at two top BDCs to consider as small businesses bulk up. The first is a new player some readers have recently asked about (an 11.3% dividend tends to get their attention!). The other is what I call the “BDC bully”: It doesn’t pay as much (but still a gaudy 8.8%)—but its huge size lets it be very picky about who it lends to.

High-Yield BDC #1: A “New Kid” Crashing the BDC Party

The Morgan Stanley Direct Lending Fund (MSDL), payer of that 11.3% divvie, has all the markings of an overlooked bargain: It’s new, launched in January 2024; it’s small, with a $1.5-billion market cap, and it’s cheap (of course!) at 86% of book value.

A bargain-priced 11.3% payer? MSDL, you have our attention!

That price-to-book measure only shows the BDC’s price against its physical assets and loan book. It doesn’t account for MSDL’s hidden value—of which there is a lot.

Start with management. As the name says, the BDC is backed by Morgan Stanley (MS), more specifically, by MS Capital Partners Adviser, a Morgan subsidiary. That gives MSDL the expertise and resources of the 90-year-old investment bank—an edge few start-ups can match.

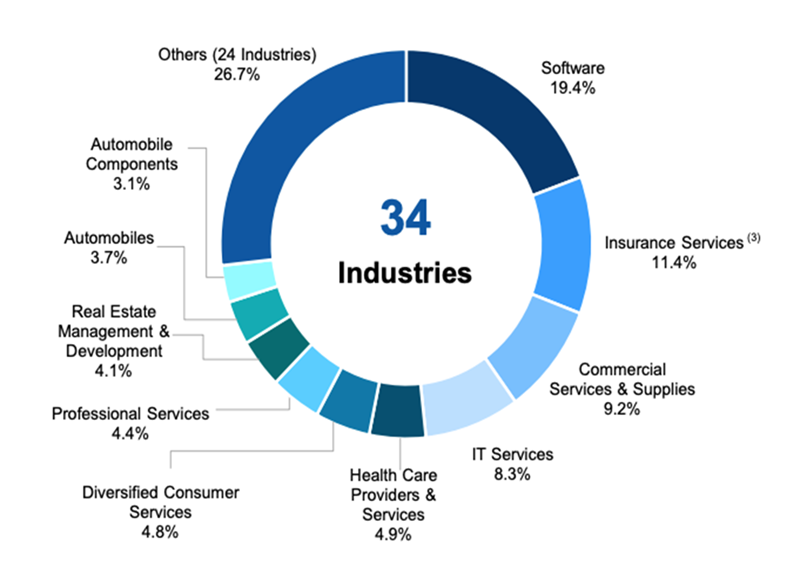

Management knows how to control risk: As of June 1, 96.4% of MSDL’s loans were “first lien.” So if bankruptcy hits one of these borrowers, MSDL is first to be repaid. But the team has taken steps to minimize even that outcome, with a portfolio spread across a range of industries:

Source: MSDL Q2 earnings presentation

The dividend? It’s covered by net investment income (NII), with $0.50 in NII over the last quarter matching the $0.50 quarterly payout.

There’s good reason to think that coverage will improve. Which leads us to interest rates, always a critical factor for BDC profits.

Here too, there’s a “bullish disconnect” for us to exploit. When the Fed cuts its policy rate—pacesetter for the rate at which financial institutions lend to each other—BDC loan income typically declines, especially floating-rate loans, an MSDL specialty (99.6% of its portfolio).

The Fed is likely to cut in September. This seems like bad news, but the crowd is missing the real story, as lower rates drive up loan demand, especially when businesses plan to grow (see small-business optimism above). That helps offset lower loan income and gives BDCs more floating-rate loans (whose income will gain when rates rise again).

MSDL has already grown its loan book, from 192 borrowers a year ago to 214. Its portfolio value has also risen from $3.5 billion to $3.8 billion. I expect that to continue as MSDL establishes itself and small-biz optimism rolls on.

High-Yield BDC #2: A “Bully” Paying a Steady 8.8% Dividend

Those strengths are enough to put MSDL on our Contrarian Income Report watch list. But we prefer portfolio holding Ares Capital (ARCC) for one main reason: scale.

ARCC is the biggest BDC by far, with over $29 billion in assets. This brings a steady stream of deal flow, helping management dictate favorable loan terms.

That’s why Ares is our “BDC bully”: Its size helps ARCC both be picky and grow quickly: As of June 30, it had 566 borrowers, twice MSDL’s number.

As well, delinquent loans were just 1.2% of the portfolio’s value in Q2—healthy for a lender in the “middle-market” credit space (companies with $10 million to $1 billion in sales), like ARCC.

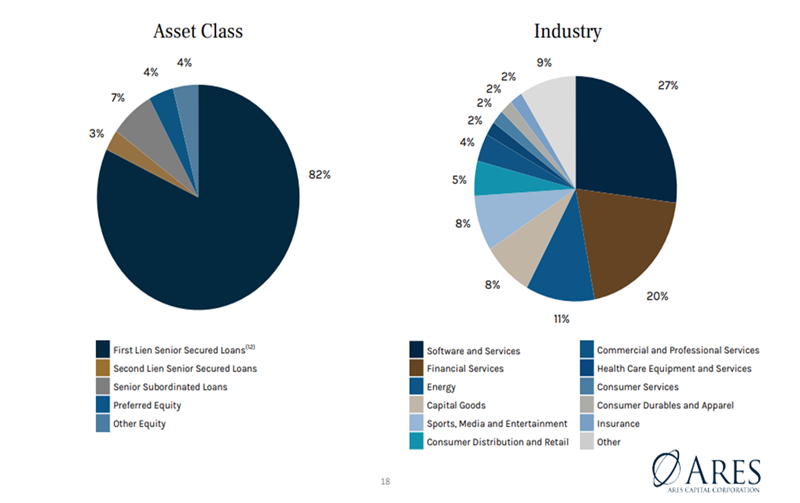

ARCC’s ability to grab the “pick of the litter” among borrowers has also let it build a diverse portfolio, with a lean toward those lower-risk first-lien loans:

ARCC continues to aggressively write new loans at attractive yields. Last quarter, the fund generated NII of $0.49 per share, covering its $0.48 quarterly dividend.

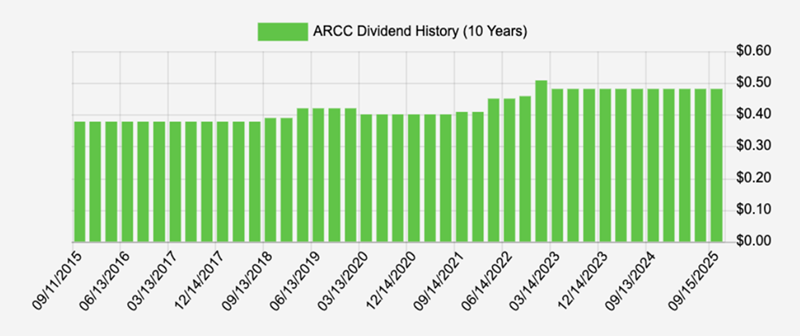

We also have a lot more dividend history to go on here, with ARCC going public more than two decades ago, in 2004. That history is very favorable indeed:

Source: Income Calendar

About 69% of ARCC’s portfolio is floating rate, but management is steering more loans that way, including 96% of the $1.1 billion of new loans written in July. That’s a smart move as future rate cuts spur more small-biz borrowing.

Finally, ARCC trades around 1.1-times book value, fair in light of its dominant position and long history. Sure, we’d like to buy “cheap,” but investors rarely knock our “BDC bully” below 1. So we’ll happily buy here and collect ARCC’s 8.8% payout while we wait for its next run up.

You Saved and Saved—and Think You Still Can’t Retire? You Probably Can.

I urge investors to buy steady high-yielders like ARCC in Contrarian Income Report for one reason: They’re a proven way to grab a strong, predictable income stream for retirement.

Stack up a few payers like ARCC in your portfolio and pretty soon you’re well on your way to a retirement funded by dividends alone—and on far less than you think you need.

Heck, you may have enough to clock out right now!

This kind of investing is critical now, with our portfolios being buffeted by inflation fears, recession fears, geopolitical fears—you name it. It’s gotten to the point where even those who’ve followed the “rules” and done everything right still think they can’t afford to hang ’em up.

I hate to see that—especially when “dividends-only” retirement is well within reach for many. They just haven’t been shown the right stocks to get them there!

That stops now. Click here and I’ll show you how you could retire on dividends alone, perhaps with as little as $500K invested. Then I’ll give you a free Special Report revealing the names and tickers of the stocks that can get you there.