2024 is setting up to be a great year for us contrarian dividend investors—but to take full advantage, we need to buy now—while fear is still in the air.

Because that terror is totally unjustified.

Here’s how I see the current state of play: Fed rate hikes are toast, and a Santa Claus Rally is on tap. In fact, the more Jay Powell tries to persuade us he’s going to keep bringing the hurt (as he did again last week), the hollower it rings.

Look, inflation is on the wane, and the last thing Jay wants is a repeat of the March banking mess. As rates head lower in ’24, our favorite dividend growers will soar, making now the time to buy, while most of the crowd is still cautious, fretting the Fed will raise rates “forever and ever.”

But wait till December: I expect the Fed to turn dovish, with the economy downshifting into that “soft landing” we’ve all been talking about for, well, a couple years now.

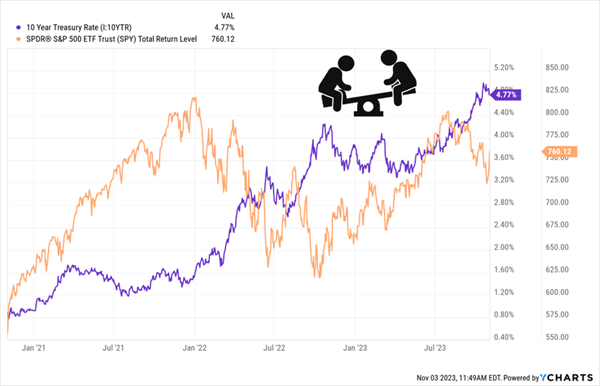

Heck, the 10-year Treasury rate—whose lurch to 5% has been the biggest drag on our dividend payers—has already called the top in rates: it’s reversed course, down to around 4.5% as I write this.

The 10-Year/S&P 500 “Teeter Totter”

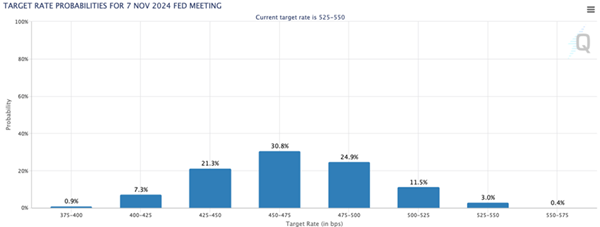

Futures traders aren’t having it, either: as of my latest read, most have the Fed’s target rate at least a quarter-point below where it is now a year out, and most of those are booking in rate cuts of a half-point or more:

Source: CME Group

So as we move through this buying opportunity, our job is to grab stocks with fast-growing dividends and share prices that are lagging those payouts. That gives us three different ways to get paid:

- A rising yield on our original buy as the payout grinds higher (we’ll see this in action with the three tickers below).

- Ongoing payout hikes (plus share buybacks, as savvy firms bargain-hunt their own stocks), and …

- Rising share prices, which catch a lift from falling Treasury yields and—more important—their own surging dividends, which pull their share prices higher as they climb.

Point 3 is really the straw that stirs the drink here, so let’s start with a top 2024 pick that provides a textbook example of this “Dividend Magnet” in action:

2024 Dividend-Growth Pick No. 1: Mastercard (MA)

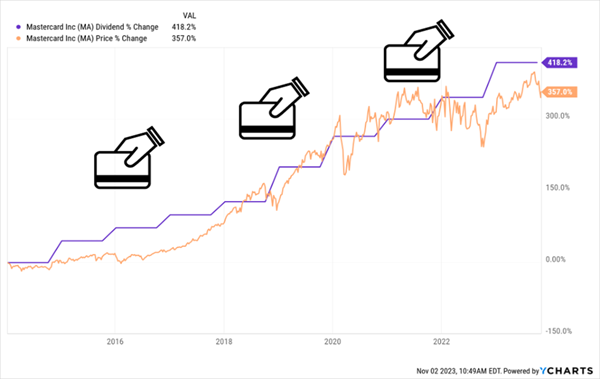

Mastercard gets exactly zero dividend investors’ hearts racing, with shares yielding just 0.6%. But man, that dividend growth:

Mastercard Ticks All 3 of Our Payout Boxes

This is exactly what I mean by a Dividend Magnet: see how the share price always jumps to meet the payout growth? Best of all, the gap between the two on the right side of that chart represents our “baked in” upside.

This is why the company has sported a current yield around 0.6% forever. But forget about that and just look at that payout growth curve, which is accelerating. If you’d bought this one a decade ago, your yield on cost would be up to 3% today—five times higher than the current yield! And you’d be sitting on a tidy 385% total return, too.

The beauty of Mastercard and its cousin, Visa (V) is that neither is a lender, so they don’t need to worry about defaults or stagnant loan originations, as banks do when rates are high. They just take a cut of every one of the millions of transactions humming through their networks every day.

That makes them “toll bridges” on consumer spending, which has held up nicely—and is likely to keep doing so as rates roll over and the economy settles into more moderate growth. And even if consumers cut back, Mastercard’s dividend will still be on rails, as it accounts for just 21% of free cash flow. A pittance.

Finally, we’re getting a nice extra kick from the stock’s “cheap” valuation. I put that in quotes because MA is never a bargain on a P/E basis, currently trading around 34-times its last 12 months of profits. But context is key here: Mastercard’s P/E ratio has averaged 41 in the last five years, suggesting plenty more price upside.

2024 Dividend-Growth Pick No. 2: Lowe’s (LOW)

Think back to the pandemic lockdowns for a second (I promise we won’t stay here for long!), when everyone reno’ed their homes, thinking they might never leave them again.

Home-improvement retailers like Lowe’s thrived—until 2022, by which time most folks had finished sprucing up their pads and inflation prompted the rest to delay their plans.

Now, with inflation falling, and rates soon to follow, those delayed renos are likely to move ahead, and at a more sustainable pace than the lockdown-induced fury of three years back. That points to sales gains for Lowe’s.

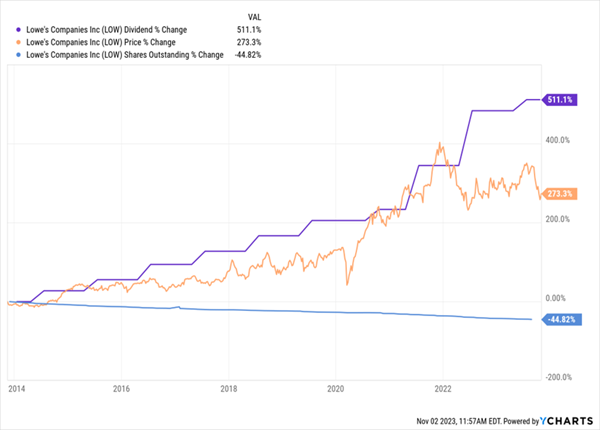

Our opportunity is perfectly spelled out in the chart below: as you can see, shareholders have enjoyed 500%+ dividend growth in the past decade, helping haul the share price up in tandem—until the 2022 dumpster fire, when the stock and payout parted ways.

Lowe’s Curb Appeal Summed Up in 1 Chart

That implies significant upside, especially when you consider that management has been on a buyback spree, taking nearly half of the company’s stock off the market in the last decade, boosting per-share metrics like EPS in the process.

I know what you’re thinking: “Brett, what about that slowdown in payout growth at the right side of that chart?” It’s true that management slowed dividend growth in the midst of last year’s uncertainty—a prudent move. But when dividend growth picks up again—and the long-term trend, as well as Lowe’s low 29% free-cash-flow payout ratio, suggest it will—it’ll exert even more force on the firm’s lagging share price.

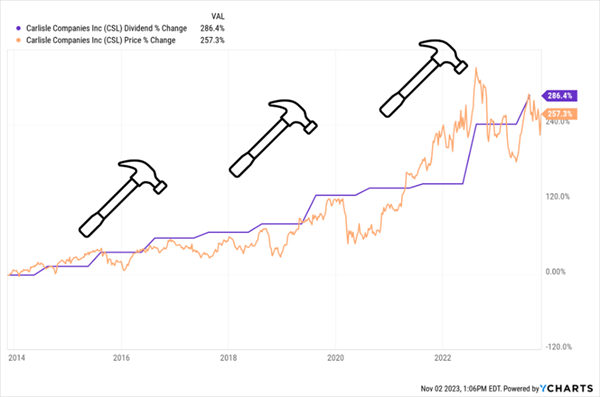

2024 Dividend Growth Pick No. 3: Carlisle Companies (CSL)

Arizona-based Carlisle sells engineered components, including roofing, insulation and waterproofing materials, to the construction, aerospace and automotive industries, among others. That makes it a direct beneficiary of the drive to make buildings more efficient—a trend supported by an array of tax credits and rebates at the state and federal levels.

The thing that stands out about Carlisle is its surging dividend: up a stunning 286% in the last decade, with a share price that’s followed, puppy-dog like, rising 257%—and leaving a nice little gap to close for more upside.

CSL’s Dividend Ratchets Its Price Higher

And there’s a ton of space to push that payout higher: CSL pays a mere 15% of FCF as dividends. That’s well below my 50% safety line; management could essentially triple its payout tomorrow and still keep it safe.

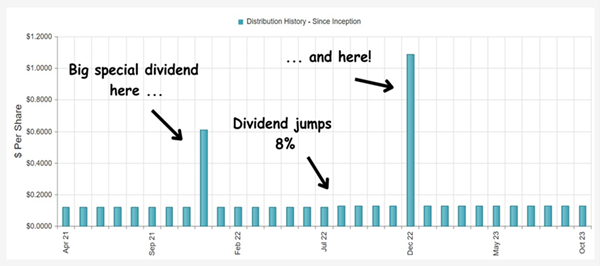

In all, payouts have risen for 47 straight years, and while revenue and earnings did pull back in the latest quarter, the company will benefit in the longer run as lower rates give construction a boost. Moreover, management recently announced a plan to sell its CIT division, which designs and makes high-performance wire and cable, as well as optical fiber. That will tighten its focus on building products.

Finally, management has been an aggressive buyer of its own shares, cutting the share count some 16% in just the last five years. That will support per-share earnings and, by extension, the share price. Buybacks are also a smart move while the stock is cheap, trading at 19-times earnings. The company’s strong balance sheet, with just $2.29-billion of debt, a mere 18% of its market cap, adds extra support.

Alert: This Top 2024 Pick Yields 14% (and Its Set to Make Its Next Payout)

One of my best buys for 2024 starts us off with a huge—and monthly paid—dividend yielding a steady 14%! Plus, this smartly run bond fund recently raised its payout and dropped some nice special dividends on investors, too.

A “Once-in-a-Generation” 14% Dividend Opportunity

What’s more, that immense payout is delivered by a manager who Morningstar previously named Fixed Income Manager of the Year, and who has also been inducted into the Fixed Income Analysts Society Hall of Fame.

To say he knows the bond world inside and out is an understatement—and now we have a chance to get him working for us. You do not want to miss this opportunity. Click here to learn more about this 14%-yielding income play and get a free Special Report revealing my latest research on it.