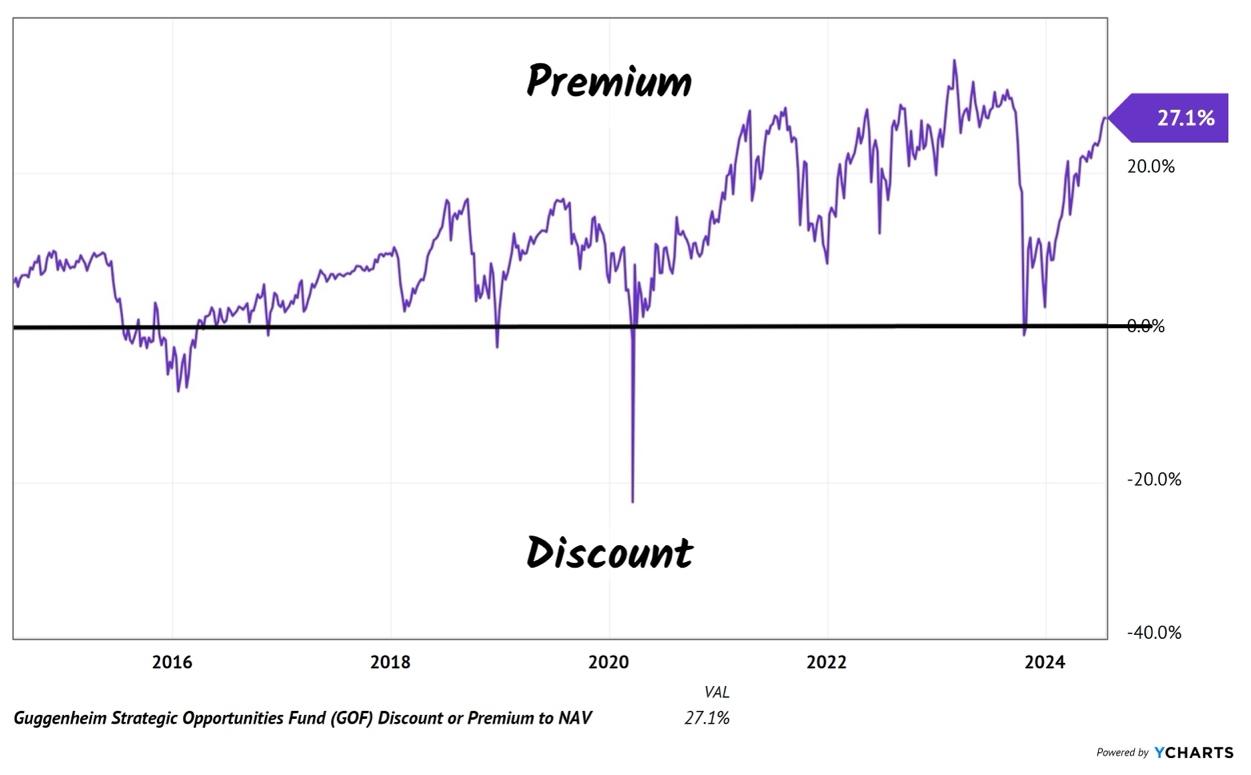

Who is paying a 27% premium for Guggenheim Strategic Opportunity Fund (GOF)?

Don’t get me wrong. GOF is a fine fund, delivering 9.8% yearly returns on its net asset value (NAV) since inception. But we are talking nosebleed valuation territory for GOF. It’s a dangerous purchase at these levels.

Bandwagoners buying today are unlikely to see 9.8% returns. Or anything close. Plus, they are exposing themselves to 27% downside risk because, as we’ll discuss in a minute, GOF eventually finds its way back to par.

How can a premium like this exist? GOF is a closed-end fund (CEF) with a fixed pool of shares. CEFs are different animals than ETFs because they do not issue more shares as their funds gain in popularity. When investors just have to own the fund—like crowds to the next new thing—GOF commands a premium.

This is not new territory for GOF. More often than not over the past decade, the fund has traded hands for more than its intrinsic value:

GOF Often Trades at Premium to NAV

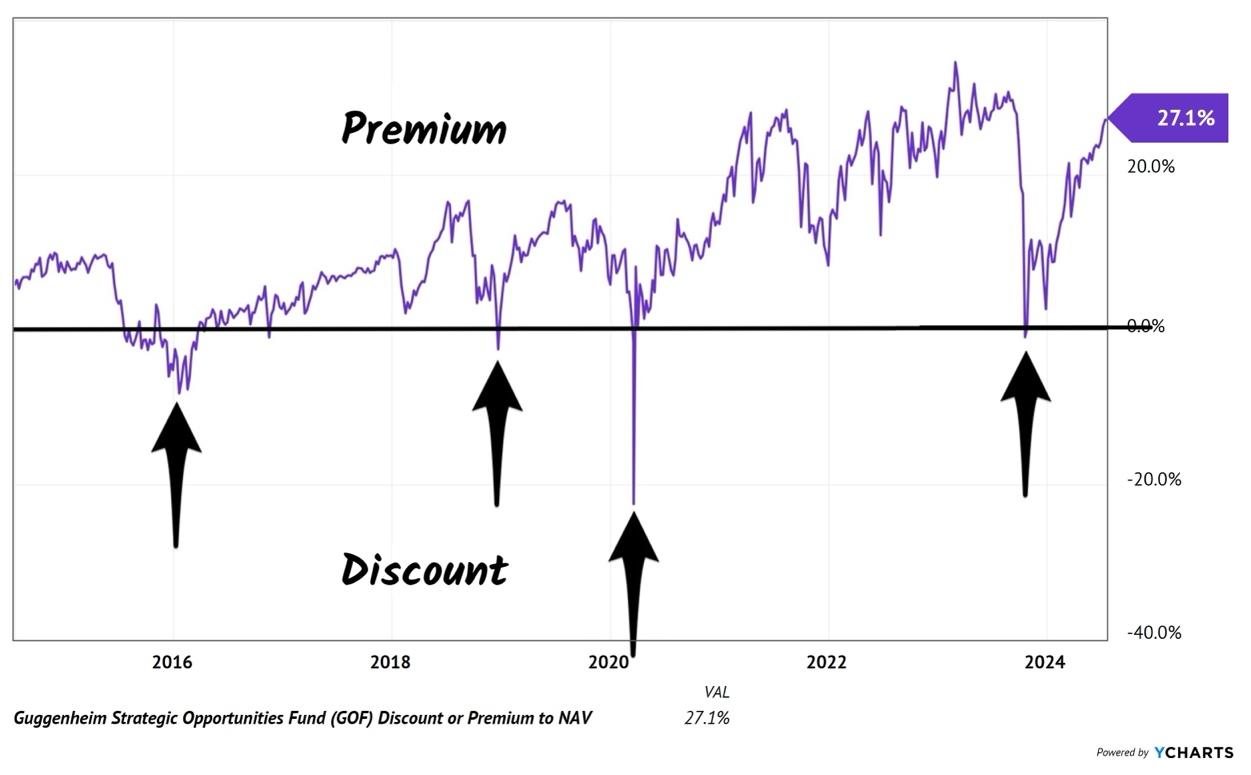

Problem is, when GOF is trading at a steep premium, it’s usually a bad time to buy because eventually the premium disappears. Every year or two or three, greed flips to fear and GOF sells at a discount. The blue-light special is brief but reliable in its reappearance:

Patient Contrarians Demand a Discount

So why not wait for mini panics like these to purchase the fund? By practicing patience we can lock in a high yield with price appreciation to boot.

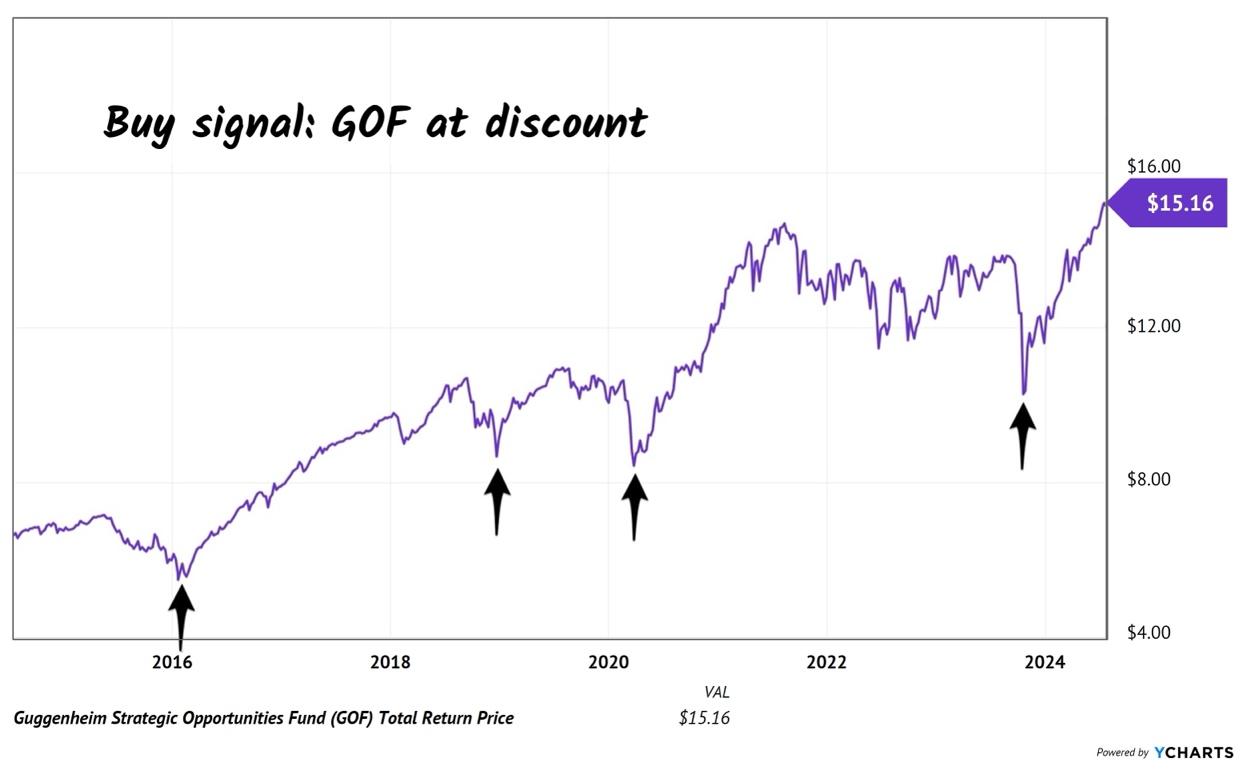

Discount buying provides serene investors with ideal entry points into GOF. Let’s zoom out and look at these four discounted moments on a total return basis (adding up the monthly dividends plus price appreciation). These are the optimal times to buy, before the FOMO crowd returns and bids GOF back up to a premium:

A Better Way to Buy GOF

Contrast this strategy with the “27% premium” buyers today, who are setting themselves up for a 27% price loss between now and the next panic! That will be a sad day for these generic trend chasers but a great day for us patient contrarians—we’ll be ready to purchase the discount.

Another “bad idea” CEF today is the PIMCO Corporate and Opportunity Fund (PTY). PTY is also trading at a 27% premium to its NAV.

Yes, PIMCO is a primo bond shop. I get the love for the company, but I pity the fool who buys PTY at such a premium!

For investors who insist on PIMCO, why not cut that 27-cent premium down to four? PIMCO Dynamic Income Opportunities Fund (PDO) trades at 104% of NAV. Not exactly a steal, but a heck of a better deal than PTY at 127% of NAV. Plus, PDO yields more!

Or consider PIMCO Access Income Income (PAXS), which yields 11.8% and trades at a modest 1% premium.

It’s a quietly frothy time in CEFland today, with perfectly good funds trading at terrible prices. Old favorite Calamos Dynamic Convertible and Income Fund (CCD) is one that I recommended to my Dividend Swing Trader readers a few years back

At the time CCD was trading at an 8% discount and yielding 8.3%. Ah the good old days—it had nowhere to go but up! My DST readers enjoyed 27% total returns in less than three months, gains that annualized to 83%.

Current CCD buyers are more apt to be karate chopped, though, when this fund returns to planet Earth. The vanilla types are paying a 20% premium for CCD. Yikes.

They are being lured by an income strategy that is often win-win. The “convertible bonds” that CCD owns are yacht club favorites that we have access to. Convertibles pay regular interest (like a bond) and can be “converted” from a bond to a share of stock if the underlying share rallies. These vehicles can provide the best of both worlds—income plus upside.

The well-known convertible fund is the benchmark Bloomberg Convertible Securities ETF (CWB). Problem is, CWB pays a piddly 1.3%! Hence CCD’s popularity—warranted, but overdone.

Again, regression to the mean is the threat here. The fund traded at a discount less than a year ago. During the next big pullback, it is likely to happen again—which means fast 20% downside potential.

I like the fund. But hate the current premium.

Fortunately, we have three better options today. My favorite CEFs are trading at discounts as I write. They pay yields up to 12% and have upside potential, too. I’d love to share my latest “bond bull” research with you, including fund names and tickers.