“Why is Arbor Realty (ABR) up 10% this morning?”

The emails piled in. And obviously, yes, it was this Tweet from Roaring Kitty—the high priest of meme stocks—that sent highly-shorted stocks higher.

Source: X.com

His real-life identity is Keith Gill. He’s a former financial analyst turned meme stock diocesan. In 2020, Keith aka Roaring Kitty led the charge behind the short squeeze of GameStop (GME), which sent that dinosaur stock (briefly) into orbit.

The mere hint that Gill was back in the game was enough for his disciples to bid up old flames GameStop and AMC Entertainment Holdings (AMC). Then Investor’s Business Daily jumped into the fray and advised a way to get more juice—by buying stocks with even more short tinder!

Ten stocks in the S&P Composite 1500, including SunPower (SPWR), B. Riley Financial (RILY) and Arbor Realty Trust (ABR), have 30% or more of their shares available for trade in the hands of short sellers… That’s much higher than the 24% of GameStop‘s (GME) floated shares controlled by short sellers.

More than 40% of Arbor’s outstanding shares are sold short. Forty percent! With so many nonbelievers, one IBD mention was enough to send shares soaring.

Remember, short sellers are borrowing shares to sell now, hoping to buy them back (“cover”) later, at a lower price and pocket the difference. Which is fine, except when Roaring Kitty is back Tweeting. I’m kidding. The shorts have a much larger problem in the form of a hefty tab that needs to be paid quarterly.

When we short a dividend stock, we must borrow the shares—which means we are on the hook to pay the dividend to the lender!

This is why we do not short dividend stocks here at Contrarian Outlook! We buy, hold or sell—we never short. We want dividends to work in our favor, not against.

Lots of short sellers have Arbor’s dividend working against them at the moment. Arbor yields 12.4% per year! So short sellers are paying a 3.1% tax on their position, per quarter, for the right to stay short Arbor. (They also owe the cost of the margin loan required for shorting! Remember, they are borrowing shares, which is not free.)

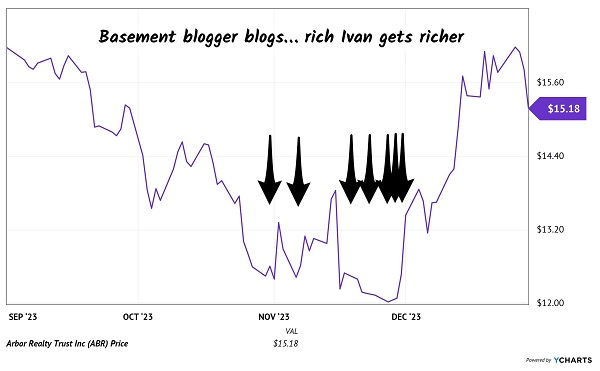

A few months back, a basement blogger decided to pick on Arbor. The blog post had no name, no face, but it was a nifty little PDF saying why “the firm that authored the paper” was short Arbor and we should be too.

I questioned whether the author’s mom realized her child was penning such a claim under her roof. Thus far, it’s been a bad bet. Arbor has delivered 12.5% total returns, including its quarterly dividends, in the six months since the bearish basement blogger hit the send button. Oops.

Fortunately for us calculated contrarians, we reasoned that we may want to take our cues from a rich executive instead. That would be Arbor’s founder and boss Ivan Kaufman, who was buying his own stock hand over fist at the time.

Ivan hit seven times after the basement blog report, adding a cool $2,460,898.90 to his personal ABR position. Shares (wouldn’t you know it) quickly bounced:

Arbor CEO Buys His Own Dip 7X!

Kaufman’s personal ABR stake exceeds $16 million, and the guy is banking nearly $2 million per year in his own dividends.

Like a good founder, Kaufman rarely sells. Perhaps he will actually cash in some chips if Arbor really pops in a short squeeze. Then again, he seems to not mind when the stock is low, because it gives him a chance to buy cheap.

Why are so many “investors” short this stock? Arbor is wrongly lumped with commercial lenders and landlords. But it doesn’t plant in that forest.

Smartly, Arbor has had cash flow diversification wheels in motion for some time. In the mid 2010s the company made a particularly big bet. At the time, Arbor was only valued at $325 million. Ivan threw down a chunk of change—$250 million!—to purchase a commercial mortgage-lending agency and its in-house technology platform.

It was a smart move because it created a new stream of loan servicing income. This grew to one-third of Arbor’s total sales in just two years—a diversified and protected income stream.

Today, Ivan refers to this as Arbor’s service income annuity. It amounts to $240 million of annual profits, which equates to $1.20 per share.

ABR’s quarterly dividend is $0.43 per share. This annuity covers two-thirds of the payout off the bat.

This was clutch when rates finally began to rise for the first time in a long time. In total, the company earned $0.48 per share last quarter—its payout is covered.

Plus, Arbor doesn’t have to reinvest excess profits to grow: the biz is all human capital and computers. I sure wouldn’t pay 12.4% per year for the right to be short Arbor!

All of this short interest serves as potential fuel for this stock price. Any day we could wake up and see the ticker pop another 10%.

Now we may not seek out short interest specifically, but we independent thinkers don’t mind it either. We like running against the herd. And the fact that we own something they will eventually need—actual shares of Arbor to buy back for delivery to the lender—is amusing.

We’re in no hurry to flip our shares for more, however. This 12.4% payer can keep on dishing dividends to us.

If this isn’t a perfect income investment, I don’t know what is! And if we act quick, we can buy a few more discounted dividend payers—like these—to craft a perfect retirement portfolio.