In last Thursday’s article, we talked about one of my favorite “low-drama,” high-paying investments—I’m talking 7%+ payouts here.

Those would be covered-call funds, which we look to in times of higher market volatility, which we’ve seen recently and I see as more likely as we move toward year end. At times like these, covered-call funds are a good option, as their option strategy cuts their volatility and boosts their income. Check out that article for our full breakdown of how this works.

Today we’re going to go one step further and delve into how these funds fit into your portfolio. We’ll also talk tickers.

Investing in Covered-Call Funds: Think Short Term

Right off the top, we should say that covered-call funds have gotten more popular recently, thanks to their attractive combo of income and stability. And while they’re great for short-term hedging and dividends, there is one thing we do need to remember about them: They’re not great for the long term.

Covered-call funds basically exchange part of their future profits for a cash guarantee in the short term. They do this by selling investors options to buy the fund’s assets at a fixed price at a future date.

As a result, since stocks tend to go up over the long term, covered-call funds will go up a little less than their indices as their best picks get sold away.

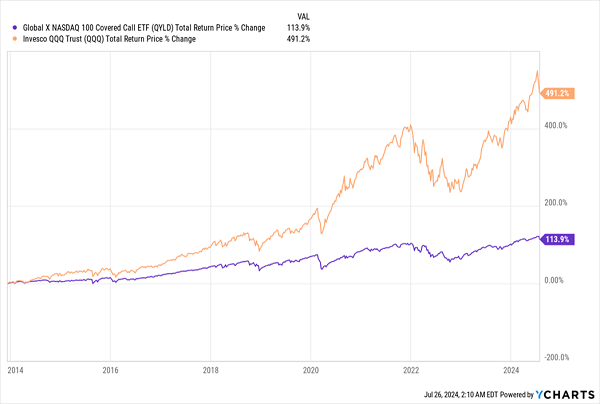

To see this in action, let’s compare a covered-call fund—the Global X NASDAQ 100 Covered Call ETF (QYLD)—with its underlying index. As the name says, QYLD (in orange in the chart below) sells options on its portfolio of the 100 stocks in the NASDAQ. The benchmark, then, is the index itself, shown by the Invesco QQQ Trust (QQQ), in purple.

Covered-Call Fund Trails Its Index in the Long Run

You’ll see this pattern repeated for pretty much every covered-call fund out there. The reason for this is that, as mentioned, they aren’t meant to be held over the long term.

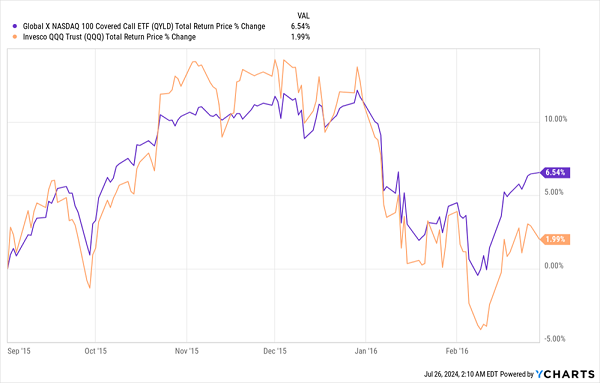

There are exceptions in the short term, however, namely when the market doesn’t really go up or down a lot but just goes sideways. To demonstrate this, let’s see how QYLD did during the flattest six-month period since 2010, which was from September 2015 to February 29, 2016:

An Outperformance Appears

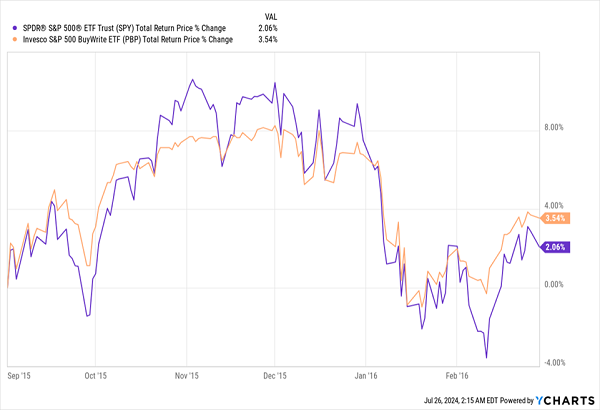

As you can see, QYLD did better than its index. It isn’t alone. Covered-call funds that own the S&P 500 and sell call options against it also did better than the S&P 500 in that time, such as the Invesco S&P 500 BuyWrite ETF (PBP):

Of course, that didn’t last long, which is the point: Funds like these aren’t meant to be held for longer. But when a market is debating whether to go up or down, a covered-call fund can temporarily outperform.

A Long-Term Buy to Pair With Our Covered-Call “Dividend Hedges”

Covered-call funds don’t just give you that extra bit of protection. As I mentioned earlier, they also pay high dividends: QYLD yields 11%, and PBP yields 8%, much more than the S&P 500.

Obviously, these covered-call funds are very compelling if you’re an income investor. And we can complement them by picking up “pure” equity CEFs (with little or no option selling) we can hold for the long term.

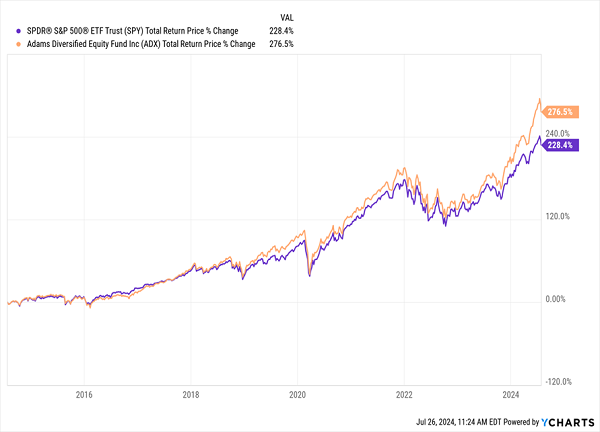

Case in point: the 8.2%-yielding Adams Diversified Equity Fund (ADX), which has outperformed the S&P 500 for a long time while delivering outsized income. (It yields around 8% now.)

Here’s how ADX (in orange below) has fared over the last decade on a total-return basis compared to the S&P 500 (in purple):

ADX Beats the Market

Part of the reason for that outperformance is that ADX doesn’t simply track an index. It’s run by Adams Funds, which traces its roots back to 1840.

The fund does hold many blue chip stocks, like Microsoft (MSFT), Amazon.com (AMZN), JPMorgan Chase & Co. (JPM) and Visa (V), so it would be a good ticker to “swap” for an S&P 500 index fund, if you’re holding one now.

ADX trades at a 9% discount to net asset value (NAV, or the value of its underlying portfolio), so we can buy its holdings for less than 91 cents on the dollar. That discount has narrowed lately, due to a change in the fund’s dividend policy: It will now pay 2% of its NAV per quarter, for an average 8% yield on NAV.

Because of its discount, that amounts to an 8.7% yield, based on the marked-down share price. I expect the new dividend policy (which replaced ADX’s old approach of paying out most of its returns in the form of a single year-end special dividend) to attract more investors and further narrow that discount, making now a great time to buy.

Alert: These 5 CEFs Buys Yield 8.7% (And Won’t Be Cheap for Long)

Most folks have never heard of CEFs, and there’s a good reason for that: The big fund companies want everyone to pick up ETFs instead. Because if everyone knew about CEFs, they may never buy an ETF again!

But that’s going to change: As interest rates fall, more people are going to go looking for high income, and I expect many to flock straight to CEFs. We want to be in before that happens.

We’ll start with the 5 CEFs I’m pounding the table on now. They yield an astounding 8.7% and are so deeply discounted that my research suggests 20%+ price gains in the next 12 months!

The time to buy them is now, before their discounts close and their prices race away from us. Click here and I’ll tell you more about how we ride closing CEF discounts to big gains. I’ll also give you a free Special Report naming all 5 of these deep-discounted 8.7%-paying picks.