Today we’ll discuss a duo of cheap dividend stocks paying 11.2%. And, for good measure, we’ll throw in another bargain even though it “only” yields 9.5%.

I jest because I love. Dividends, that is. And bear markets don’t usually last much longer than this. So, it is double-digit yield shopping we go.

These are serious yields we’re looking at—the kind we need to retire on dividends alone. They’re hard to find among over-followed, over-analyzed and over-owned blue-chip stocks. But they’re abundant in BDCland (populated by business development companies (BDCs), of course).

Like real estate investment trusts (REITs), business development companies are a creation of Congress. But rather than spurring real-estate investment, BDCs were designed to pump some blood into America’s small businesses. They provide much-needed capital that many banks simply won’t serve up because of the risk, or that they will—at excessively high rates.

And there’s plenty of reasons to love this under-covered industry:

- BDCs, like REITs, must pay out at least 90% of their taxable income to shareholders in the form of dividends. In the case of BDCs, we’re talking downright indulgent payouts typically in the high single and low double digits.

- They provide capital to a wide array of companies, which effectively makes them private equity companies that you and I can buy publicly!

- BDCs don’t get much media or analyst coverage—because they’re complicated and boring—so it’s common for them to be mispriced. That allows us to snap them up for less than they’re actually worth.

Sometimes these stocks are cheap for a reason. BDCs can and do have bad years. We contrarians mostly avoided them last year because, well, what’s the point of a dividend if we’re losing it in price?

(That said, dividends did cushion the blow. See below.)

Dividends Saved Investors 10 Points’ Worth of Pain

With that, let’s look at our first 11.2% payer. It happens to be trading for just 66% of its book, or net asset value (NAV). This means we’re buying the company for just 66 cents for a dollar in assets. Cheap!

PennantPark Investment (PNNT)

Dividend Yield: 11.2% yield

Price/NAV: 0.66

PennantPark Investment (PNNT) might sound familiar to regular readers—it’s the sister of PennantPark Floating Rate Capital (PFLT), which I’ve kept an eye on for some time.

PennantPark invests in the debt and non-controlling equity of primarily U.S.-based middle-market companies with EBITDA of $10 million to $50 million. Its portfolio currently holds 123 companies across 32 different industries—most heavily in business services (18%) and healthcare, education and childcare (12%).

The company says it targets “proven management teams, competitive market positions, strong cash flow, growth potential, and viable exit strategies.” Honestly, most BDCs are looking for most of the same traits. More useful to know is that PNNT traditionally is a conservative underwriter that boasts very few non-accruals across hundreds of investments in its 15 years of existence.

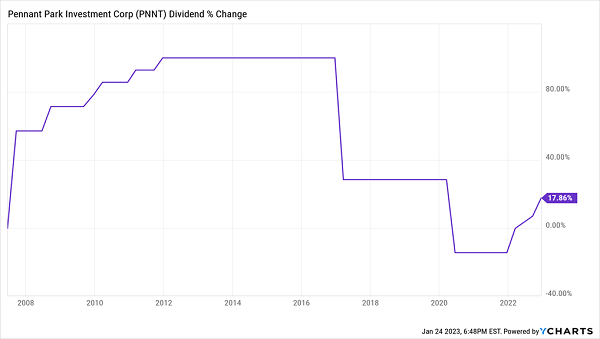

That conservative nature wasn’t enough to dodge a big hit during the COVID downturn. In 2020, PNNT slashed its payout by a third, to 12 cents per share. Encouragingly, the company aggressively started replenishing the payout, raising it four times in the past four quarters, to a current 16.5 cents.

A one-time ding in the midst of a generational crisis would be one thing, but this was PennantPark’s second rodeo. PNNT was forced to make a slightly bigger cut, from 28 cents per share to 18 cents (~36%) to its dividend in 2017 thanks to poor performance from its energy investments.

Not Exactly the Picture of Dividend Consistency

Also, even though PennantPark Investment is named differently from PennantPark Floating Rate Capital, 96% of PNNT’s debt portfolio—which makes up roughly three-quarters of the total portfolio—is floating-rate. That’s helpful while rates are rising, as it benefits more from Fed rate hikes than BDCs with fixed-rate investments. But if and when Jerome Powell flips the switch back to rate cuts, that portfolio might not look nearly as enticing as it does now.

It’s too bad—a deep 34% discount to NAV represents one of the biggest sales in the BDC world right now.

Prospect Capital (PSEC)

Dividend Yield: 9.5%

Price/NAV: 0.76

Prospect Capital (PSEC) is one of the market’s largest business development companies (BDCs). It has funded more than 400 investments in its nearly two decades of publicly traded life, and it currently boasts some $8.5 billion invested in 128 companies across 37 industries.

PSEC’s primary business is middle-market lending, which makes up 53% of the portfolio. It invests in American companies with EBITDA (earnings before interest, taxes, depreciation and amortization) of up to $150 million, typically through senior secured loans. But it also has arms focused on real estate (primarily multifamily) investing (19%), middle market buyouts (16%), and subordinated structured notes (9%).

I’ve long criticized Prospect Capital for not taking advantage of its relative size and scale—it has delivered long-term underperformance compared to the BDC industry’s better players, and it has cut its dividend twice since 2014.

A few years of aggressive expansion are finally starting to bear fruit, however. PSEC shares are more competitive of late as operations have improved. Net interest income for its fiscal year ended in June was up 9% and, at 81 cents per share, more than covered its 72 cents’ worth of monthly dividends. I’ve previously harped on the BDC’s dividend coverage, so this is a meaningful development.

Prospect Capital still has some question marks, including its high exposure to a fairly opaque investment to National Property REIT Corp., a portfolio of mostly multifamily properties. It’s also marred by high management fees. And while the 24% discount to NAV is certainly attractive on its face, PSEC has long traded at a massive discount—it could take a mighty catalyst to ever change that.

PSEC could finally be righting its longtime wrongs. But given that Prospect’s management has largely remained unchanged—it’s still the same crew that delivered a lot of disappointment to shareholders—a lot of caution (and a little healthy skepticism) is deserved.

Crescent Capital BDC (CCAP)

Dividend Yield: 11.2%

Price/NAV: 0.73

Crescent Capital BDC (CCAP) is another debt-minded, conservatively managed BDC. And it’s also dirt-cheap, at a 27% discount to NAV—which you can in some part chalk up to some underperformance over the past year or so.

CCAP Lags the Field, But It’s on the Upswing

Almost 99% of CCAP’s portfolio is floating-rate in nature. Senior secured first lien and unitranch first lien investments make up the lion’s share of the portfolio—89% by fair value.

This is an extremely defensively positioned portfolio, too. Crescent currently invests in 136 companies across 18 industries, but with an extreme overweight (86% by fair value) in non-cyclical industries. Health care equipment investments are the biggest chunk at 29%, followed by 21% in software and services. And if you’re looking for geographic diversification, CCAP offers a little, with roughly a tenth of the portfolio invested across Europe, Canada and Australia.

Of course, that portfolio is going to look different pretty soon: Crescent Capital is expected to close on its acquisition of First Eagle Alternative Capital (FCRD) as early as the fourth quarter of this year. First Eagle’s 73 holdings are primarily first lien senior secured debt; FCRD tries to limit each individual investment to less than 2.5% of the portfolio.

It’s a pricey buyout: First Eagle garnered $4.86 per share—a massive 66% premium that’s split across CCAP shares, cash from Crescent Capital and cash from CCAP’s advisor, Crescent Cap Advisors.

As a result, CCAP halted its streak of four consecutive quarters delivering a 5-cent special dividend. It’s not nothing—that contributed an extra 1.3 points to its already generous yield—but for now, management appears to want to conserve a little cash and see how the acquisition unfolds.

Give Me 4 Minutes, I’ll 4X Your Retirement Income

The yields and discounts on these BDCs are truly impressive, but they’re all wait-and-see stocks—nothing we can invest in with any conviction right now.

If we want a cozy, comfortable retirement without bleeding your nest egg dry, we need to be able to plan around our income with laser precision—and BDCs with a checkered dividend past, or that are plowing all their resources into M&A—don’t exactly scream “long-term dividend security.”

Fortunately, there are plenty of safe harbors in our “Perfect Income” portfolio—and you can enjoy their security and sky-high dividends, too.

The perfect dividend retirement stocks have several things in common:

- They pay you consistently, predictably and reliably.

- They’re built to survive—even thrive—in market crashes.

- They deliver double-digit returns, with safe, secure investments.

- They take just a few minutes every month to “manage.”

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Getting each and every one of these things from any single holding might sound impossible. But it’s par for the course for nearly every position in my “Perfect Income” portfolio.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Click here for my newly updated briefing on the Perfect Income Portfolio!