A couple weeks ago, I showed you a 4-stock dividend portfolio that’s throwing off a gaudy 7.3% yield today.

It’s ideal if you’re retired and leaning on your investments to pay the bills. But if you’re looking to grow your nest egg, your best bet is to reinvest your dividends and harness the magic of compounding.

Today I’ve got three stocks for you that are perfect for doing just that.

But first, I’d say the name of the game here isn’t necessarily a high current yield; instead, you’ll want to home in on stocks that boost their payouts year in and year out. Not only do top-flight dividend growth stocks give you a steady income stream in your golden years, but they tend to beat the market over time, too.

The three stocks below are perfect examples. Their average current yield is 3.4%, which is certainly better than the S&P 500’s average of 2.2%.

But the real story is how much they’ve boosted their payouts in the last five years: an average rate of 165%, or 33% annualized! And that doesn’t include the huge special dividends one of them has delivered (more on that in a moment).

That’s translated directly into a stupendous total return: an average 110% over the past five years, well ahead of the SPDR S&P 500 ETF (SPY), at 80%. Plus all three are bargains—a rarity in a market trading at a nosebleed 24 times earnings.

This Dividend Will Double in 3 Years or Less

In the past five years, Wyndham Worldwide (WYN) has hiked its payout by 233% and followed that up with a 116% price gain, for a total return of 139%.

Put another way, $10,000 invested in the hotel operator back in 2011 would be worth a cool $21,600 today—plus you’d be yielding 6.4% on your original investment—more than double Wyndham’s current yield of 2.9%!

With gains like that, you’d think Wyndham would be expensive … but you’d be wrong. Its forward price-to-earnings ratio stands at 11.9, a nice discount to its five-year average of 15.5, implying 30% upside from here if it returns to that level.

Either way, the pieces are in place for more big dividend hikes: the payout ratio (or the percentage of earnings paid out as dividends) is just 35%, and Wyndham’s forecasting adjusted EPS of $5.61 to $5.75 in 2016, up from $5.14 last year.

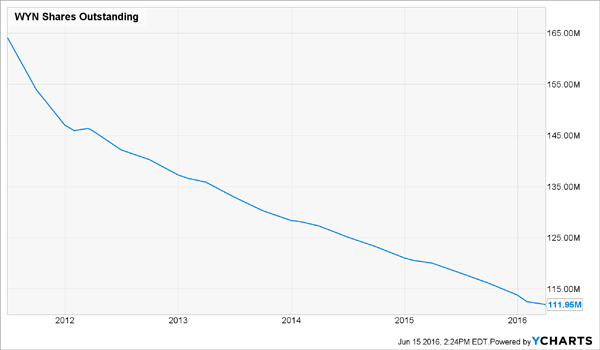

Meantime, the company’s share buybacks help put a floor under the stock price, because they cut the number of shares outstanding, thereby boosting EPS.

The company does face strong competition from other hotel chains and Airbnb, but tourism spending is soaring, particularly in the developing world, so there’s plenty of business to go around.

A “Boring” Stock With an Exciting Dividend

Packaging Corp. of America (PKG) isn’t a stock you hear a lot of investors—particularly younger investors—talking about. The company’s business is decidedly unsexy: it makes packaging for everything from produce to in-store displays.

But the stock checks all my boxes for a top retirement portfolio pick: it pays a tidy 3.4% current yield; boasts strong dividend growth: 175% in the past five years; and it’s a bargain, with a forward P/E of 13.1.

It also aligns perfectly with an old Warren Buffett standby: “Never invest in a business you can’t understand”—and they don’t come much simpler than Packaging Corp.

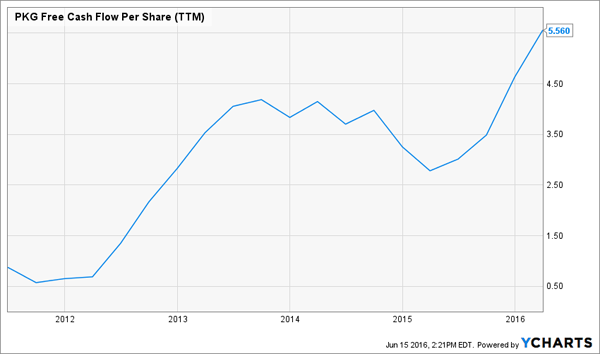

Here’s something else Buffett would love: Packaging Corp. is a free-cash-flow machine, with FCF per share clocking in at $5.56 over the 12 months ended March 31, easily covering the $2.20 the company handed out in dividend payments.

Management’s plowing some of the remainder into share buybacks—a smart move, given the stock’s bargain valuation. In the latest quarter, Packaging Corp. repurchased $100 million worth of shares, finishing off its $150-million authorization. In February, the board signed off on $200 million more.

Best Buy’s “Hidden” Dividend

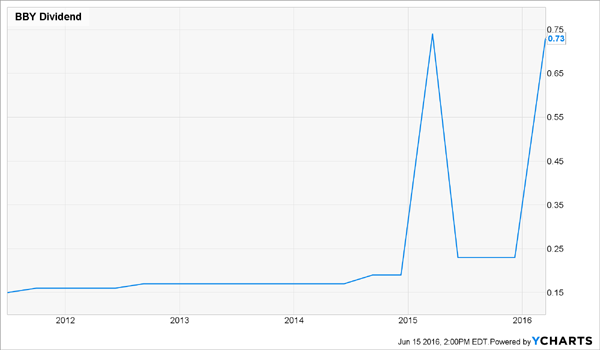

Best Buy (BBY) yields 3.8% today, but that yield doesn’t include special dividends, of which the electronics chain has paid two: $0.45 in March 2016 and $0.51 in March 2015.

When you add the latest special dividend to the regular quarterly dividend Best Buy paid out over the last 12 months, it bumps the stock’s “actual” yield up to 4.8%.

This is why I love special dividends—because stock screeners like Google Finance and Yahoo Finance don’t account for them in their yield calculations, so investors often overlook companies that pay them.

Best Buy has come a long way since 2012, when pressure from Amazon.com (AMZN) drove it to steep losses. But it’s turned the tide by slashing costs, closing money-losing stores and upping its own online game.

Since the start of 2013, BBY has delivered investors a 185% total return, though the stock is down year-to-date after the company lowered EPS guidance for the second quarter to between $0.38 and $0.42 from the consensus forecast of $0.50. A year ago, EPS came in at $0.41.

But profit growth should pick up again later this year and next as the company continues to work through its turnaround.

While you’re waiting, you’ll pocket a dividend anchored by Best Buy’s low 48% payout ratio, steady cash flow and healthy balance sheet, with $3.1 billion in cash and just $1.4 billion of long-term debt. And yes, there’s always the possibility of more “specials” down the road.

The stock is also a bargain, trading at just 10.1 times forecast 2016 earnings.

Best Buy will deliver strong returns for investors, but with a turnaround play like this, you’ll have to be patient—and there will still be plenty of ups and downs along the way.

Conclusion

Even though these three companies are hiking their dividends at a rapid clip, it will still be 10 years or more before the yield on your original investment comes anywhere near what you’d collect on three other stocks I’m recommending now.

I’m talking about payouts of 8.0%, 8.4% and even 11%.

Whether you’re in retirement or looking to compound your dividends before you reach your golden years, these three undervalued investments are a great choice, particularly in today’s low interest rate environment.

They’re an often-ignored asset class called closed-end funds, and in addition to the fat 8.0% to 11.0% yields they throw off, they all trade at big discounts to the value of their assets—with markdowns of 7% to 15%—so if you get in now, you can look forward to a nice gain as that gap narrows.

Don’t miss out. Go right here to get the names of these incredible income plays now.