Real estate investment trusts (REITs) just don’t get the respect they deserve. And that’s too bad, because owning just a handful can make a huge difference in your investment returns.

I’ll reveal four of my favorite REIT buys now in just a moment.

First, let me explain why I’m pounding the table on the sector today.

The main reason: REITs often pay dividend yields far above your average S&P 500 stock. What’s more, they’re obligated to pay out 90% of their taxable income as dividends, which forces management to take a disciplined approach to growth.

In addition, REITs give you a very liquid way to invest in physical assets; your shares represent a part of the actual buildings the trust owns.

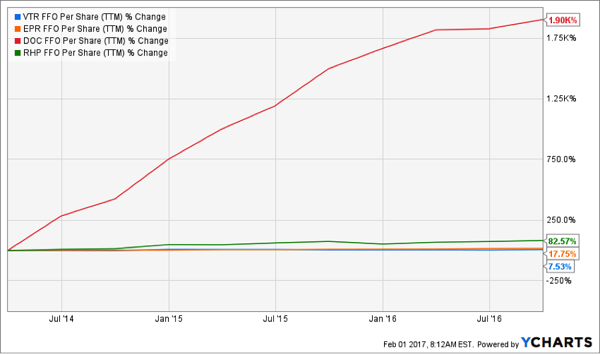

And many REITs are very diversified—we’re talking ownership of hundreds, even thousands, of buildings across many states. The best trusts are diversifying even further by buying up more properties that, in turn, boost their funds from operations (FFO), which is how REITs define their earnings.

Thanks to all their strengths, REITs saw a flood of investor interest last year, but that interest is waning as President Trump steals all the headlines. This is good for us, because it means there are four REITs out there that aren’t rising as fast as they should.

Why should they be soaring?

Well, they’ve beaten the REIT market broadly (not to mention the S&P 500) on a total-return basis over the last year; they have low payout ratios (or the percentage of FFO paid out as dividends); well-diversified holdings; great management; high occupancy rates; and growing operating margins. In short, they have just about every strength you’d want in a REIT.

So what are these companies?

First, there’s Ventas (VTR) and Physicians Realty Trust (DOC), two healthcare REITs with different approaches to the market (VTR focuses on healthcare facilities, while DOC owns doctor’s offices).

Then there are two entertainment-focused REITs: EPR Properties (EPR), which owns movie theaters, malls, ski parks and schools; and hotel and resort operator Ryman Hospitality Properties (RHP).

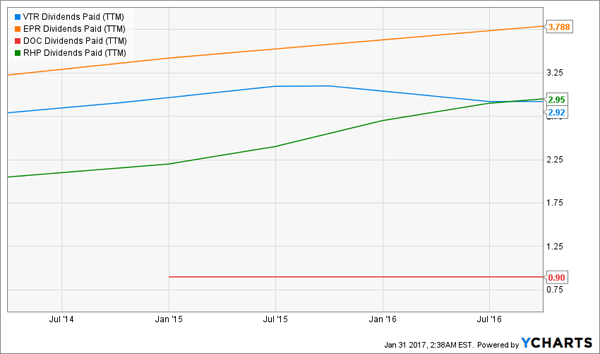

These companies all have one thing in common: they’re delivering strong FFO growth that’s translating into higher dividends for investors:

FFO Is Soaring …

… and so Are Dividends

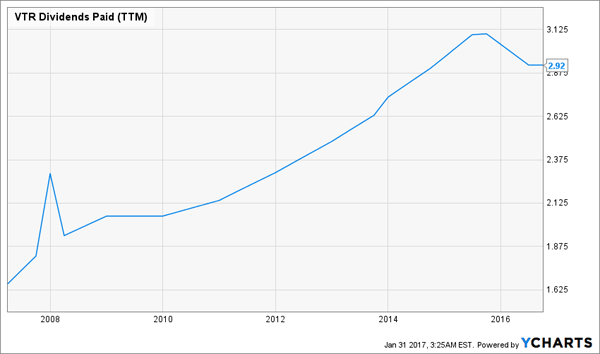

Let’s zero in on Ventas. The “dip” you see in the chart above is misleading because of special dividends in 2015 skewing the numbers—looking longer term at the total dividends, we see VTR is a strong dividend grower:

Reliable Long-Term Dividend Hikes

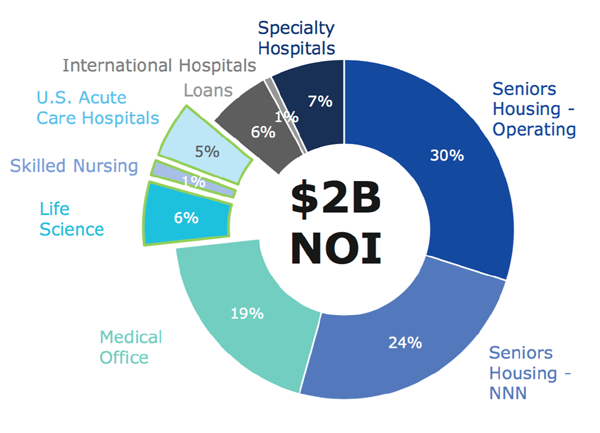

In fact, VTR has grown its dividend by 9% annually over the last decade, thanks to its simple approach: build a diversified portfolio of high-quality properties that are in ever-increasing demand:

A Multifaceted Healthcare Juggernaut

Source: Ventas Inc.’s website

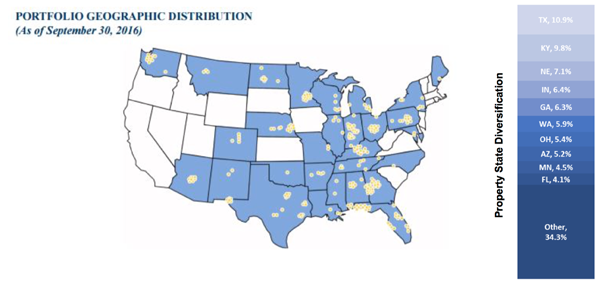

EPR Properties also diversifies geographically, so if demand for its entertainment, recreational and educational facilities declines in one pocket, it can be picked up in another—and EPR is constantly looking to shift to areas with high population growth:

EPR Properties Are Everywhere

Source: EPR Properties’ website

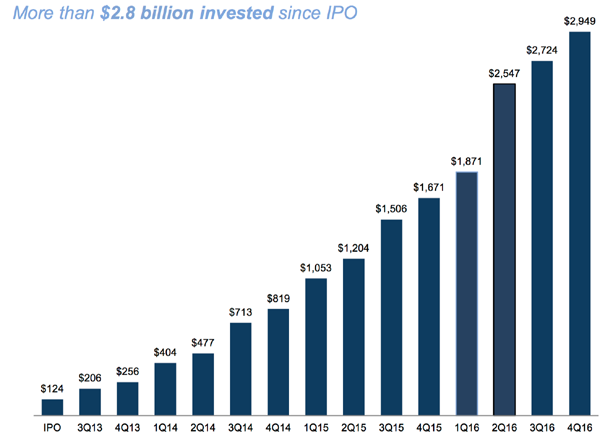

Physicians Realty Trust, as the newest and youngest REIT of our four picks, is less diversified, since it focuses on medical-office buildings (95% of the total portfolio). But this is still valuable to us because it’s different from VTR’s approach, so we’re not diluting our portfolio by investing in competing firms.

Moreover, DOC has the highest FFO growth by far but hasn’t increased its dividend yet—which suggests dividend growth is coming. What’s more, DOC is expanding its footprint more broadly across the country, in turn delivering more diversification:

Physicians Realty Trust Spends to Grow

Source: Physicians Realty Trust

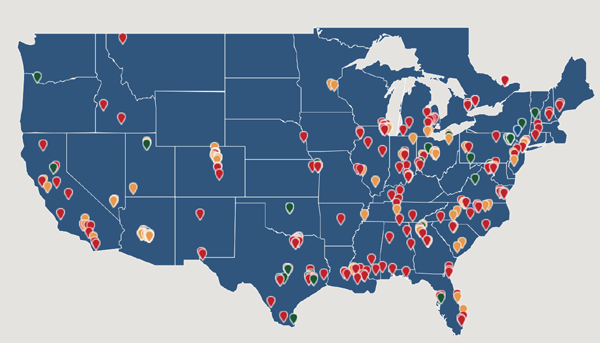

The map below shows the company still has a ways to go, however:

DOC Goes West

Source: Physicians Realty Trust

Finally, let’s look at Ryman.

This is the smallest company in our portfolio by far, with only four resorts in total. But I don’t care, because Ryman is a cash cow: in the last four quarters, it’s generated $5.19 per share in FFO, while paying out only $3 in dividends.

That means its payout ratio is 57.8%, one of the lowest I’ve ever seen on any REIT. Since becoming a REIT in 2012, Ryman has increased its dividend nearly 40%, though it hasn’t hiked the payout since the end of 2015. That makes this company ripe for a dividend hike, but its small size means it’s overlooked. I expect a nice jump in the price when Ryman does announce a higher payout.

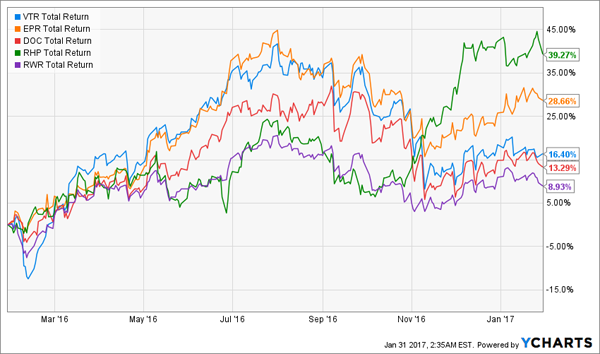

Finally, let me give you one more reason to pick these REITs over an index fund like the SPDR Dow Jones REIT ETF (RWR). I am not a fan of indexing because I see too many opportunities to beat the index with just a bit of analysis and risk taking. This applies even more to REITs than to regular stocks:

Selected REITs Beat the Index

Why settle for an 8.9% annual return when we can get triple that? At the same time, our income stream is much stronger:

A Little Extra Effort Delivers a Nearly 5.0% Average Yield

Here’s How We’ll Double Our Income in 2017

A 5.0% yield is nice, but you can collect a lot more income than that—I’m talking secure yields of 8.0% and up—if you invest in the 3 “stealth” income plays I want to show you today.

In addition to their high, safe yields, these income wonders throw off incredible dividend growth to boot!

This means you’re assuring yourself of 10%+ annual returns, with most of that coming as cash dividends. And unlike the overheated members of the Dow, they’re cheap now, trading at 7% to 15% below their true value.

That’s great news for us, because it gives us plenty of price upside to enjoy while we’re pocketing these high—and growing—payouts!

These stealth plays are perfect for today, with the market getting twitchy in the wake of the go-go “Trump bump.” And they’re going to become increasingly popular with income investors once they’re discovered.

That means you need to make your move now, before their prices get bid up (and their yields get squeezed). Click here to get all the details on my favorite 8.0%+ “No Withdrawal” dividend payers right now.