2016 is in the books, and the S&P 500 gained over 11% on the year. That’s great news if you’re already in the stock market … but it’s bad news if you’re looking to buy.

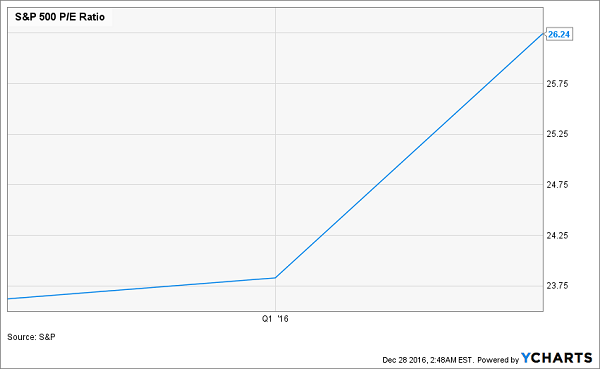

The market’s price-to-earnings (P/E) ratio is now 26.1, which is 17.6% higher than it was at the beginning of the year. In other words, if you buy stocks now, you’re paying nearly a fifth more for those companies’ earnings than you would have nearly 12 months ago.

Stocks Getting Expensive

Making matters worse is the fact that the S&P 500 has soared over 8% in the last two months alone—accounting for much of the year’s total gains.

“Trump Bump” Reboots Stocks

Moments like these are every passive investor’s worst nightmare. The market has skyrocketed and it feels expensive to buy anything—but if you buy nothing, your cash will earn you a handsome return of 0.3% … if you’re lucky.

At times like these, we all need to be value investors.

Specifically, we need to find stocks that have missed out on the broader rally, but because they’ve been overlooked, not because they’re duds. This means avoiding companies like Bank of America (BAC), which was a great buy a couple months ago, but now all the upside is already priced in:

BAC: The Check’s Already Been Cashed

Instead, we want stocks that have gone up less than the market year-to-date and with P/E ratios that are below the S&P 500 average. Our shopping list should also include companies with strong financials, and especially a history of revenue—and dividend—growth.

You may be surprised to hear that there are a few such stocks are out there, even if they’re getting tougher to find.

ASX: A High Yield and Big Payout Growth

Advanced Semiconductor (ASX) is one. Revenue growth just recently went positive after a year of declines, and analysts expect sales to jump 6.7% in 2017. The 5.0% dividend is generous, and it has grown nearly 50% in the last three years (The company pays dividends annually, usually in August).

Yet ASX’s P/E ratio is just 15.3, and the stock is down 11% year-to-date, partly on the broad weakness in tech:

Market Losing Faith

Nothing has changed in the company to suggest that the trend toward higher sales and dividends could be broken, making it a no-brainer buy at today’s level, which is near the stock’s 52-week low.

Ark: Lock in This 4.2% Dividend Now

A second great underappreciated company is Ark Restaurants (ARKR), which has a P/E ratio of 16.8, despite 4.4% year-over-year earnings per share (EPS) growth in its latest quarter and a 2.1% revenue increase. The stock also has a 4.2% dividend yield. Ark shares are also up just slightly year to date, even as they’ve rallied along with the broader market and on expectations of stronger revenue growth in 2017:

Going the Right Way … but Still Undervalued

Throw in the stock’s ultra-low P/E ratio, which seems more like one you’d find on a company with declining revenue, and I love this name.

FLO: Buy as Expansion Kicks In

Flowers Foods (FLO) is a bit pricier from a P/E perspective, trading at 23 times trailing-twelve-month earnings, but its 3.8% year-over-year revenue growth in the third quarter, along with a 3.2% dividend yield, make it a contender.

And the elevated P/E is just because this baked-goods company is investing heavily in expansion efforts. The market is ignoring this and pricing it as a company on the decline (its P/E ratio is down from 24.9 at the beginning of the year)—although it’s also been saved by the recent market recovery:

Flowers Still Deep in the Red

However, with an 8% year-to-date price decline still on the books, this looks like a great value pick to lock in its 3.2% dividend yield. Oh, and that dividend has grown by over 14% a year, on average, over the last three years, so expect that income stream to keep getting bigger.

FNF: The Last Bargain Financial Stock?

Surprisingly, there are a few remaining underpriced financial firms, despite the euphoria the sector has enjoyed after Trump’s surprise win, and Fidelity National Financial (FNF) is one of them. The stock is still down slightly on the year after the post-election rally failed to push it back up over January levels:

Fidelity Gets Little Love From the Trump Rally

There are a few reasons for this. The biggest is that Fidelity’s business model. As a brokerage, it’s not seen as ideally positioned to benefit from Trump’s planned deregulations and tax breaks.

But that doesn’t mean it’s overvalued. Fidelity’s P/E ratio is a laughable 16.9, despite a 9.8% return on equity and a 2.9% dividend yield. Revenues are soaring at a 5.2% year-over-year rate, and EPS is up 9.4%. Over the last three years, the quarterly dividend has gone up 13.0% annually, on average, meaning management has the chops to increase payouts to shareholders at a time when low interest rates have made things harder for financial firms broadly.

These are just some of the dividend plays I like for 2017, but they’re not the only ones. I’m also pounding the table on 6 other investments that yield a safe—and growing—8.0%!

We’ve put them together in our brand-new “No-Withdrawal” retirement portfolio. And thanks to its outsized payout, you’ll instantly trigger a $40,000 income stream if you put a modest $500,000 nest egg into these low-risk investments!

The best part? You don’t have to sacrifice gains to get that income. Each of these dividend machines is cheap right now, setting them up for nice upside in 2017, too.

Why spend hours and hours searching for the right combination of growth and income when you can get both with just a few simple mouse clicks?

Let me bring this powerful new portfolio to you now. It could be the best investment move you make in 2017. Simply click here to get all the details. You have nothing to lose and much to gain.