What’s the best way to add the consistent income growth of the Dividend Aristocrats to your portfolio without paying the “royalty premium” of these popular, well-covered stocks?

Buy ‘em while they’re young.

Right now, there are a handful of stocks I want to show you today that are knocking on the door of Dividend Aristocrats membership. We’re talking only one to three years shy of the 25-year benchmark of consecutive annual dividend increases.

That means they still boast more than two decades’ worth of higher payouts, which is plenty of proof that they’ve got bulletproof financials and put shareholders’ interests on a pedestal.

These stocks usually boast more upside than their more experienced counterparts, too. Let’s consider the performance of the three newest Aristocrats – Praxair (PX), A.O. Smith (AOS) and Roper Technologies (ROP) over the past few years. They’ve delivered total returns (including dividends) between 36% and 87%:

Fresh-Faced Dividend Aristocrats Deliver Returns Up to 87%

Today, there are a handful of Aristocrat hopefuls that are close to the royal court. Two of them have potential similar to what we’ve seen out of A.O. Smith and Roper Technologies – which means they could quickly double from here.

But not all inductees are buys – I’ve also identified two almost-Aristocrats that we should avoid.

Essex Property Trust (ESS)

Dividend Yield: 3.1%

Dividend Hike Streak: 24 years

Essex Property Trust (ESS) is about to become a rarity. The apartment real estate investment trust (REIT) is just a year away from becoming only the second REIT in the Dividend Aristocrats – Federal Realty Investment Trust (FRT) is currently the only real estate play in the 53-member group. (Such an announcement likely will come in February 2019.)

Essex, which manages multifamily apartment communities in the West Coast – including Southern California, Northern California and Seattle – went public in 1994, but has been in the real estate game since 1971. Essex’s geographic concentration means the REIT has been (and will continue to be) a beneficiary of the boom in technology; in fact, the headquarters of the 10 biggest publicly traded tech companies by market capitalization are all located within Essex’s markets.

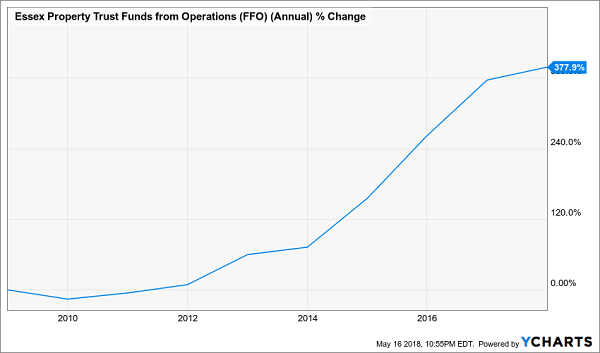

This REIT may be putting together an impressive dividend-growth streak, but that’s not because actual business growth is anywhere near “mature.” The company’s funds from operations (FFO) have exploded by nearly 380% over the past decade. And Essex kept its growth story going in Q1 of this year, recording 5% FFO growth, raising its full-year FFO growth forecast – and, of course, expanding its dividend by 6.3%.

Essex Property Trust (ESS) Is Riding Tech’s Coattails to Riches

It’s not often that a REIT deserves to be called “exciting,” but Essex is worthy.

Realty Income (O)

Dividend Yield: 5%

Dividend Hike Streak: 24 years

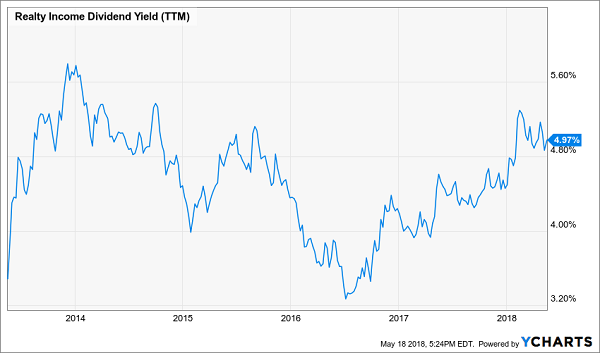

Realty Income (O) has staked its reputation to its dividend, which admittedly has a pretty impressive track record. The self-proclaimed “monthly dividend company” has paid 574 consecutive monthly dividends, increased its payout for 82 consecutive quarters, and boasts 4.7% compound annualized dividend growth since its 1994 IPO. Moreover, like Essex, the company is just one year away from Dividend Aristocracy.

No one is questioning Realty Income’s legitimacy on the dividend front. It’s for real.

However, even Realty Income’s impressive dividend growth and elevated income level – at 5%, O shares are yielding near the high end of their five-year range – isn’t enough reward for the harsh reality staring this REIT in the face.

Realty Income (O): A Good Yield, But at What Price?

I warned income investors about The Big O back in 2016, and even though it has lost a quarter of its value since then, I still don’t like the value prospects here given the harsh realities Realty Income faces.

That’s because Realty Income is a retail REIT, and thus is in Amazon’s crosshairs. Sure, some of its tenants include the likes of LA Fitness (no threat from Amazon) and FedEx (FDX, which actually benefits from Amazon at the moment), it also leases out single-tenant properties to the likes of Walgreens (WBA) and Kroger (KR) that absolutely are in the path of the e-commerce wrecking ball.

Realty Income might not lose you money in the next few years, but it’ll face an uphill climb to cover any significant ground.

Five percent remains respectable today. It puts the stock’s payout on a perch just above the safest fixed income investments (like Treasuries).

But is 5%+ enough compensation given that O’s property holding are shakier than ever? I’m not sure. As a retail landlord, it’s a crapshoot every month as to which rents are going to get paid – and which tenants will succumb to “Death by Amazon.”

Instead of gambling on O, I’d prefer to bet on surer things – like bonds that will actually rise in value as rates continue to climb.

Ross Stores (ROST)

Dividend Yield: 0.9%

Dividend Hike Streak: 24 years

Close your eyes and think about a stock that is trading near all-time highs, has ripped off 152% gains in five years and has generated double-digit annual profit growth for the past half-decade.

Open your eyes. What did you imagine? A hot chip stock? Maybe a defense contractor or a biopharma play?

Nope. Those stats belong to discount retailer Ross Stores (ROST).

Wait, Seriously?

It seems almost unimaginable to be bullish about brick-and-mortar retailers given that looming Amazon threat. But there are a couple of exceptions, and Ross Stores – which has 1,409 stores across 37 states, the District of Columbia and Guam – is one of them.

Ross delivers brand names at deep-discount prices, even undercutting rival TJX’s (TJX) TJ Maxx brand by about 33%. That’s enough to keep people coming through its doors even as customers flee other brick-and-mortar outfits. The company actually recorded 4% same-store sales growth last year – a figure that would make most other fashion retailers chartreuse with envy.

Better still, Wall Street’s pros are modeling 10% annual profit growth for the next five years. Moreover, the company has put up 165% dividend growth over the past five years but still has a payout ratio of less than 20%!

Sears (SHLD), JCPenney (JCP) and Macy’s (M) are toast. But Ross Stores looks like the truth.

International Business Machines (IBM)

Dividend Yield: 4.2%

Dividend Hike Streak: 23 years

International Business Machines (IBM) has done at least one thing right this year: It got the sales monkey off its back. In January of this year, the company reported a modest 4% year-over-year improvement in revenues – good enough to snap a 22-quarter streak of sales declines.

But Big Blue remains a big disappointment.

Dividend Growth Doesn’t Matter If Everything Else Is Plunging

IBM shares have essentially been dead money for a decade as the enterprise tech fell behind in the race to the cloud and spent years trying to catch up. Admittedly, IBM at least has its head in the right place, focusing on the cloud, cybersecurity and data analytics, but its lousy push off the starting blocks really set the company back.

The most recent quarter wasn’t exactly encouraging. While IBM did beat on the top and bottom lines, profit margins were helped by a one-time tax gain and, backing that out, weren’t exactly up to snuff. Moreover, revenues from its so-called “strategic imperatives” (those growthier cloud and data initiatives, among others) merely met expectations, discouraging analysts.

Also disappointing was IBM’s dividend increase, which came in at less than 5% – one of its cheapest hikes in years. A plateauing dividend is often a problematic sign.

How to Retire on 8% Dividends Paid EVERY MONTH

Relying on dividend growth from the likes of IBM will leave your retirement portfolio in tatters. In fact, even relying on Dividend Aristocrats in general could be dangerous – with an average yield of less than 2%, the Aristocrats deliver less income than the 10-year T-note!

However, I have a portfolio of dividend winners that not only will pay you 4 times more, but will pay you 3 times more often.

When you retire, chances are you’ll be relying heavily on dividend income to get you through your regular expenses: the house, the car, power … you name it. But while most publicly traded companies tend to pay dividends out quarterly, your bills sure aren’t quarterly. They come every single month, rain or shine.

That’s why monthly dividend stocks make so much sense for long-term retirement planners. A reliable stream of income that doesn’t vary from month to month allows you to budget with precision. And with the right plan, you can collect $3,000-plus in dividends every single month – and do it with a smaller nest egg than even the suits at Merrill Lynch say you need to retire well.

My “8% Monthly Payer Portfolio” checks off every box investors need from retirement:

- Monthly income to use against your monthly bills.

- Dividends large enough to allow you to live off investment income entirely. That means no selling your stocks and shrinking your nest egg, which ultimately shrinks your regular dividend paycheck.

- Better returns on any dividends you choose to reinvest. If you don’t need the income from your portfolio right away, you don’t have to wait every three months to put dividends to work – you can sink them back into new investments just about every 30 days!

These monthly dividend payers include a few picks that have remained mostly under the radar despite their high payouts and general quality. For instance, this portfolio includes an 8.7% payer trading at a bizarre 5.3% discount to NAV, and an 8.5% payer that not 1 in 1,000 people even know about.

Because these big dividends compound quicker, they’ll turbocharge your net worth and allow you to enjoy the retirement you’ve worked so dearly to reach. Don’t delay! Click here and I’ll send you my exclusive report, Monthly Dividend Superstars: 8% Yields with 10% Upside, for absolutely FREE.