Shall we turn 2023 into a bounce back year for our retirement portfolios?

How about we shoot for, say, 23% total returns?

The surest way to do it is by employing a technique I call the dividend magnet.

It’s safe. Reliable. And works beautifully on the back side of a bear market.

I recently gave a guest lecture for a finance class at California State University, Sacramento. One of the students, to put it lightly, was excited to make money in stocks.

His hand went up from the back of the classroom. (Nobody sits in the front rows. Some things never change!)

I pointed, he responded: “So I read that stocks with big dividends aren’t necessarily the best to buy. And that we should focus on, well, the medium yields.”

“Yes!” I yelled. Nearly pumping my fist. “Jon, flip the deck forward,” I instructed my friend, the actual professor of the class, to flip my slides.

“Look, big dividends are great if you are retired. Or close to being retired. Because you can live off of the income and not have to sell any stock.

“But you all are far from retirement. I mean, you haven’t even started working yet. You have enough time to make a lot of money. So that you can retire early—and then collect dividend income on your giant cash pile.

“Seriously, how much longer are you all going to be here?” I waved my arms maniacally at the surrounding campus. “A couple more years? More? Maybe you can make enough money using this strategy that you never have to work.”

Blank stares from the class. Even from my new pal in the audience. (As usual, I got carried away and “completely overdid it” as my wife likes to say.) But I was just getting started. Heck, I had 90 slides to share!

A flurry of them showed the dividend magnet at work—my safe “get rich quick” strategy. Here’s one:

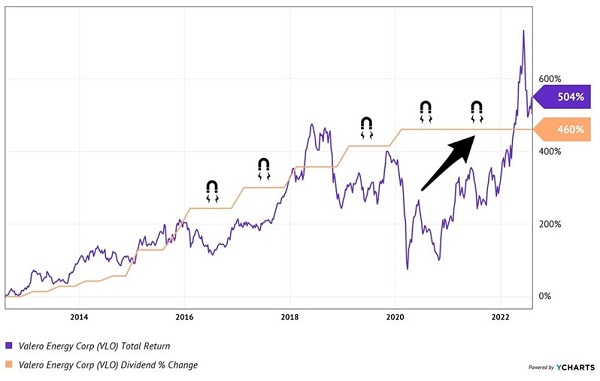

Valero’s Dividend Magnet

This is blue-chip oil refiner Valero (VLO). Its share price, the purple line above, is volatile because it moves with energy prices.

Valero’s dividend, the orange line above, is much steadier. The company is a cash cow and most years, it raises its dividend.

You can see that its payout (orange) acts as a “magnet” for its price (purple). The stock price can wander for months—sometimes many months—at a time. But eventually, the magnet “pulls” it higher.

It’s no coincidence that over this decade, VLO’s price appreciated 504% while its dividend climbed 460%. The magnet pulled the stock price higher.

Now VLO yields 3%—a “medium” dividend in wise student terms. It rarely pays much more because its stock price is always climbing to “catch up” with its payout raises. Dividend investors see when Valero’s yield is higher than its average and they buy. The buying boosts the price, to the tune of 504% in 10 years!

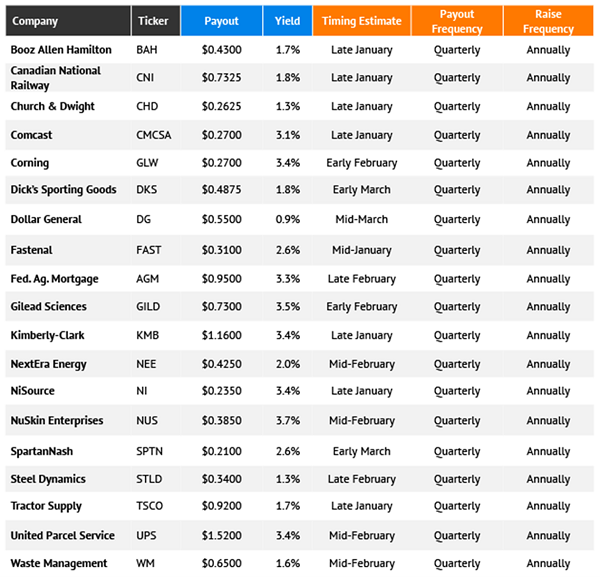

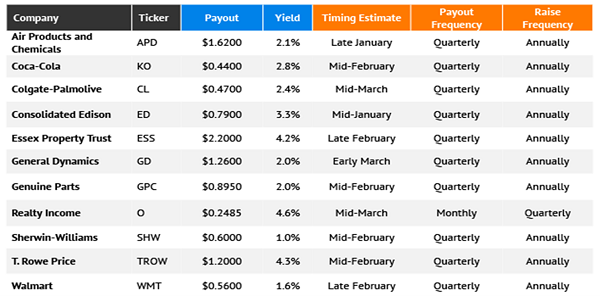

Want the next Valero? Here’s a list of 43 dividend raises that may hit the wires in the months ahead.

43 Dividend Raises Coming Up

Dozens of firms are likely to raise their dividends in the weeks and months ahead, and that’s where we should start our search.

Let’s review them in four groups: Traditional stocks, predominantly high-yield master limited partnerships (MLPs), real estate investment trusts (REITs) and Dividend Aristocrats.

Traditional Stocks

Featured Stock: Tractor Supply (TSCO)

One of the most aggressive dividend hikes of 2022 came from Tractor Supply (TSCO, 1.7% yield), which in late January unveiled a juicy 77% payout increase, to 92 cents per share.

Coincidentally enough, that followed a 70% rise in shares in 2021—a record operational year for the “rural lifestyle” retailer. Revenues were up 20% to a record $12.7 billion. Net income? Up 33% to $997.1, another all-time high.

But I’m curious to see how the retailer follows through after a much different 2022. A major driver of TSCO’s business over the past couple years has been Americans’ COVID-fueled exodus from cities into suburbs, exurbs and the country.

The influx of new potential customers is slowing, however. TSCO shares outperformed the market but still finished the year 6% lower—perhaps reflecting what’s expected to be good, but still more moderate, full-year 2022 growth compared to 2021.

So I certainly expect Tractor Supply’s 2023 dividend increase to be more modest than last year’s. But a still-aggressive hike would project confidence in continued robust growth ahead. Expect to find that out in late January, when TSCO is slated to report Q4 earnings.

Data Source: Morningstar, 1/10/23

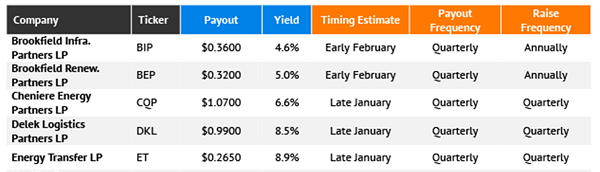

MLPs

Featured Stock: Energy Transfer LP (ET)

The energy sector rode half a year’s worth of skyrocketing energy prices to a full year of ridiculous returns in 2022. And while energy master limited partnerships (MLPs) didn’t perform as exuberantly as E&P stocks, they still progressed by leaps and bounds as they continued to recover from 2020’s pain.

2022 was particularly encouraging for Energy Transfer LP (ET, 8.9% yield), which returned to growing its distributions after halving its payout in 2020.

Energy Transfer is responsible for 120,000 miles of America’s energy infrastructure—according to the company, some 30% of the country’s natural gas and crude oil moves through its pipelines. But that scale didn’t matter much in 2020, as the COVID downturn in energy prices slashed ET’s worth by as much as two-thirds at its lowest point.

Rising oil prices (and, more importantly, rising oil demand) did wonders for ET in 2022, however. Indeed, intrastate nat-gas volumes, midstream gathered volumes and NGL fractionation volumes all hit new records during the third quarter of 2022. That allowed the MLP to raise its 2022 estimates for the third time in three quarters.

ET also resumed distribution growth at the start of the year and raised its payout four times in as many quarters, boosting the yield to nearly 9%. At 26.5 cents per share, the MLP is getting ever closer to its pre-cut 30.5-cent level.

How much closer will it get? Expect an update on the distribution sometime in late January.

Data Source: Morningstar, 1/10/23

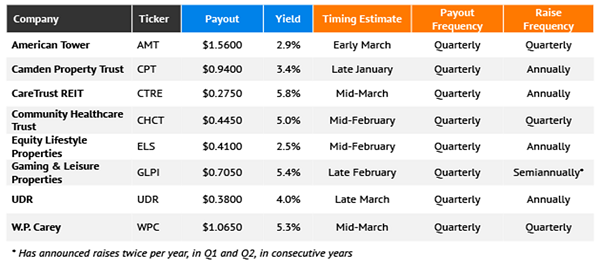

REITs

Featured Stock: Gaming & Leisure Properties (GLPI)

Trending in the exact opposite direction were real estate investment trusts (REITs), which were flattened in 2022 and lagged the broader market by a considerable measure.

But Gaming & Leisure Properties (GLPI, 5.4% yield) was a rare pleasant surprise, posting positive returns and operational strength, possibly foreshadowing more dividend growth ahead.

GLPI is a massive casino property owner, with 59 properties—all but one of which (the Tropicana) are outside of Las Vegas. It’s a geographically diversified operator, with casinos spanning 18 states, from Hobbs, New Mexico, to Columbus, Ohio, to Bangor, Maine. And in 2022, GLPI—as well as competitor Vici Properties (VICI)—thrived compared to their sectormates. Why? Well, for one, they tend to operate under extremely long-term triple-net agreements, so rent is safer and more stable than many other REITs. Also helping both companies are CPI-linked escalation clauses that help them fight off inflation.

Gaming & Leisure Properties is hardly invulnerable—it shaved 14% from its payout in 2020. But it has since resumed dividend growth with four hikes in the past two years, and its 70.5-cent payout is now above its 2020 levels.

Up next? It’s harder to say with GLPI because its schedule of hikes has been a little unorthodox. But if it follows the pattern of the past two years, it could announce a dividend hike sometime in late February.

Data Source: Morningstar, 1/10/23

Dividend Aristocrats

Featured Stock: T. Rowe Price (TROW)

There are zero guarantees when it comes to dividend investing. If you want proof of that, just look at PPL Corp. (PPL), a utility company that had grown its dividend in every year but one for roughly two decades—but whose run hit a brick wall in 2022 with a 52% pay cut.

That’s what makes the Dividend Aristocrats, and their minimum 25-year streaks of uninterrupted dividend hikes, so impressive.

The potential payout hike with the most intrigue, to me, is T. Rowe Price (TROW, 4.3% yield), which raised its payout 20% in 2021, delivered a massive $3-per-share special dividend midway through that year, then tacked on a respectable 11% to its payout. Clearly, T. Rowe is happy to spend when times are good and cash is plentiful. And it has a streak of 36 consecutive dividend hikes to defend.

Why T. Rowe’s next potential hike is so intriguing is because 2022 was downright awful to the investment management firm. While financials declined less steeply than the overall market, asset managers were fricasseed; TROW shares plunged by more than 40%. The company is expected to report deep declines on both the top and bottom lines for full-year 2022.

So it’s fair to expect a less exciting raise to TROW’s payout, which we’ll likely hear about in mid-February. But if the slowdown in dividend growth isn’t too severe, T. Rowe could be communicating that it expects last year’s troubles to fade in 2023.

Data Source: Morningstar,1/10/23

7 Little-Known (for now!) “Dividend-Magnet” Picks That Crush TROW

T Rowe is a great dividend stock to own—a mainstay in many investors’ portfolios. And its deep selloff has made it a nice bargain now, whether you’re buying “straight up” or through a DCA strategy.

But again, there are plenty of reasons to believe its best dividend growth might be in the rear-view mirror. At the very least, its payout hikes have been extremely inconsistent over the past few years.

And we prefer dividends that are not only growing but accelerating.

Accelerating payouts have an outsized impact on share-price growth, too, as the surging payout powers the stock’s Dividend Magnet, which yanks the stock higher.

That’s why we’re looking to 7 other stocks instead of T. Rowe. These stocks all have accelerating dividends and powerful Dividend Magnets that are delivering impressive share-price gains, too.

These 7 stocks and my proven Dividend Magnet system are your best route to reliable profits and rising payouts as we head into an uncertain 2023.