I get it – you want a diversified portfolio that lets you live off dividends alone. And you probably don’t want to spend most of your waking hours worrying about a million tickers either.

Consider exchange-traded funds (ETFs) then, which provide your portfolio with instant diversification through a single purchase. Pick a strategy you like (ie. high yield) and let the fund do the work for you.

Today we’ll highlight five dirt-cheap ETFs that distribute loads of cash … and let you walk away with the lion’s share of income. Now you and I both know that high fees rob you of returns. That’s why so many investors have moved out of high-cost actively managed mutual funds and into low-cost indexed ETFs. But even within the world of ETFs, it pays big-time to comparison shop for fees.

Consider the results of a $10,000 investment in two funds: Fund A that charges 0.5% in annual expenses, and Fund B that charges just 10 basis points more, at 0.6%. Despite the exact same returns, after 30 years, Fund B’s fees have eaten almost $2,000 in returns on a mere $10,000 investment!

Expenses Drain Your Wealth!

It gets worse. Even if higher fees are offset by similar improvements in performance, you still fall behind over the long haul. Despite the fact that Fund A underperformed Fund D by a whole percentage point, “low and steady” won the race with more than $1,000 in extra returns.

Even Better Returns Can’t Make Up for Higher Fees

Just ask the fund experts at Morningstar, who in 2016 ran an updated study on fund fees versus performance. Their conclusion? “We’ve done this over many years and many fund types, and expense ratios consistently show predictive power. Using expense ratios to choose funds helped in every asset class and in every quintile from 2010 to 2015.”

Here are five funds that keep expenses low, and yields high:

VanEck Vectors Preferred Securities ex-Financials ETF (PFXF)

Yield: 5.8%

Expenses: 0.41%

The VanEck Vectors Preferred Securities ex-Financials ETF (PFXF) was the ETF industry’s answer to the financial crisis of 2008-09, but it’s also the answer for investors looking to invest in preferred stocks for a song.

Preferred stocks are considered by many to be “hybrids,” because they have some stock-like traits, but some bond-like traits too. For instance, preferred stocks trade on an exchange, just like a stock, but they typically don’t represent ownership in a company, which is closer to a bond. Also, they offer (typically high) fixed payments, just like a bond, and because of that, they tend to trade very closely to their par value.

Preferred-stock mainstays like the iShares U.S. Preferred Stock ETF (PFF) invest the majority of their assets in preferreds from the likes of Wells Fargo & Co. (WFC) and Citigroup (C). The PFXF, however, is a collection of 118 preferred stocks that completely eschews this industry standard, instead investing heavily in areas such as electric utilities, real estate investment trusts (REITs) and telecoms. Thus, top holdings right now include the likes of T-Mobile US (TMUS) and NextEra Energy (NEE).

PFXF yields nearly 6% while charging an industry-low 0.41% in expenses, so this ETF is great on sheer numbers alone. But considering we’re seeing the new presidential administration push for massive financial deregulation amid bubbling subprime car loans and spiking mortgage delinquencies, PFXF looks like the safest play in the preferred world right now.

Let the Income Roll In With VanEck’s PFXF

iShares 0-5 Year High Yield Corporate Bond ETF (SHYG)

Yield: 5.1%

Expenses: 0.3%

The iShares 0-5 Year High Yield Corporate Bond ETF (SHYG) is a “Goldilocks” bond fund if there ever was one.

The SHYG invests in more than 600 high-yield corporate bonds with less than five years in remaining maturity. A corporate bond is simply debt issued by a company, typically done for the purposes of raising capital. When a financially sound company issues bonds, they’re often given one of several “investment-grade” ratings by the major credit ratings agencies, such as Moody’s. However, bonds with a higher risk of default are classified as “junk,” and have to offer higher interest rates to entice buyers. They’re beloved by income investors not just for their high yield, but their relative stability compared to common stock.

However, SHYG invests in these bonds in a way that provides a balance of yield and relative safety that’s just right.

On the one hand, SHYG’s investments are in the junk debt of companies like Sprint (S) and Valeant Pharmaceuticals (VRX), which naturally carries high yield thanks to the loftier credit risk.

However, the majority of the fund (about 80%) is invested in the top two tiers of junk credit ratings, so you’re getting mostly junk debt … but not garbage debt. Better yet, SHYG offers even more protection in the way of an average maturity of just more than two years, so these bonds aren’t going to be as rattled by changes in interest rates as comparable longer issues.

As a result, SHYG doles out a yield of 5.1% currently, and you don’t necessarily need to tremble every time the Federal Open Market Committee meets. Meanwhile, the ETF’s 0.3% is one of the cheapest in the junk-bond world.

iShares’ Young SHYG ETF Offers the Best of Two Worlds

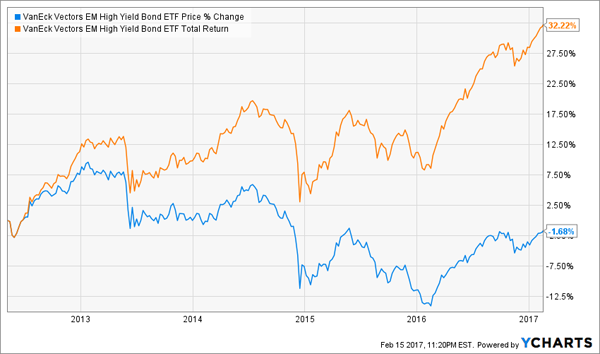

VanEck Vectors Emerging Markets High Yield Bond ETF (HYEM)

Yield: 5.7%

Expenses: 0.4%

Just like American companies raise capital by issuing debt, so do companies across the world – and that includes those headquartered in emerging markets.

And you’d think that going from short-term American junk debt to a big bundle of emerging-market debt would be fraught with excess risk.But you’d be pleasantly surprised.

The VanEck Vectors Emerging Markets High Yield Bond ETF (HYEM) invests in 355 high-yield bond issues – most of it corporate, but about 6% is government issued – across the emerging world. Yes, there’s exposure to the who’s who of EMs – China debt makes up 14% of the fund, with Brazil at 10% and Russia at more than 8%. But this diverse ETF even boasts decently sized weights to bonds from Kazakhstan, Venezuela and Colombia, among other traditionally underrepresented emerging markets.

HYEM takes a page from the short-term book, with an effective duration of 3.5 years that’s less than its American high-yield peers. That helps defray some of the risk from investing in these less developed markets.

And at 0.4% in expenses, HYEM represents one of the cheapest possible ways to invest in emerging-market debt.

VanEck’s HYEM Is Your Low-Cost Ticket to Exotic Dividends

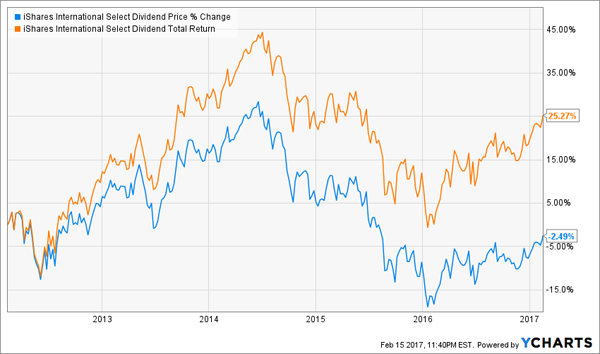

iShares International Select Dividend ETF (IDV)

Yield: 4.6%

Expenses: 0.5%

While emerging markets are the place to be for high yields in the bond world, investors need to venture to more stable locales for the best dividend equities.

Enter the iShares International Select Dividend ETF (IDV), a concentrated portfolio of developed-market holdings that will celebrate its 10th birthday in June.

The IDV’s underlying index is made by running a Dow Jones developed-market index through a few screens for quality and dividend growth, then investing in the 100 highest-yielding stocks that make the grade. Currently, IDV is heaviest in Australian stocks (22%) such as top holding Rio Tinto (RIO), and British stocks (19%) such as pharma giant AstraZeneca (AZN). The fund is rich with blue chips, with its holdings averaging about $20 billion in market capitalization.

And IDV’s yield of well more than 4% comes at a cost of just 50 basis points – an excellent ratio for international dividend equities.

iShares’ IDV Smooths Out Turbulence With Substantial Yield

VanEck Vectors High-Yield Municipal Index ETF (HYD)

Yield: 4.5%

Expenses: 0.35%

Last but certainly not least is the VanEck Vectors High-Yield Municipal Index ETF (HYD).

When most people think of government debt, they think of Treasuries, which are issued by the U.S. federal government. However, there’s also municipal bonds – debt issued by smaller areas of government, including states, counties and cities.

HYD invests in a wide basket of nearly 1,400 such municipal bonds that skews heavily toward California (17%), Illinois (11%), New York (9%) and Ohio (7.5%). The high yield comes from the higher-risk side of the munibond market, with 46% of HYD’s muni debt sitting in junk status, with another 23% as unrated. Still, just less than a third of the fund sits at the investment-grade BBB rating to enhance liquidity.

The dividend benefits of this fund are munibond oldies, but goodies. HYD pays out on a monthly basis, not quarterly, and because these bonds are generally exempt from federal taxes, you’re not looking at a 4.5% yield, but anywhere between a taxable equivalent SEC yield of between 5.3% and 7.4%, depending on your tax bracket.

In the small world of high-yield muni ETFs, HYD and its 0.35% annual fee offers the best mix of yield to expenses.

Capture High, Tax-Exempt Yield With VanEck’s HYD

Live Off Dividends Forever With This “Ultimate” Retirement Portfolio

If you want to retire comfortably, you need big dividends. The steady drumbeat of income is what helps pays the bills and keeps you afloat when you’ve stopped collecting a paycheck.

But if you want to get through retirement without ever touching your nest egg, you need more than just giant dividends – you need dividend growth to beat back inflation, and you need capital appreciation to keep building your nest egg. The “triple threat” stocks in my “8% No Withdrawal” retirement portfolio will deliver exactly that!

How many times have you seen a pundit shill for OK-yielding blue chips like Coca-Cola or Kellogg? They’re not bad companies, but they leave you with just 3% to 4% in dividends, paltry payout hikes and little in the way of growth potential.

You and I both know that math doesn’t add up. Those 3% to 4% returns on a nest egg of half a million dollars will only generate $20,000 in annual income from dividends at the high end!

You’ve worked your tail off for decades. So you deserve more out of your retirement.

My “No Withdrawal” portfolio ensures that you won’t have to settle during the most important years of your life. I’ve put together an all-star portfolio that allows you to collect an 8% yield, while growing your nest egg – an important aspect of retirement investing that most other strategies leave out.

I’ve spent most of the past few months digging into the high-dividend world, and I’ve had to weed out several yield traps that looked great on their surface, but potentially disastrous at a closer look. The result is an “ultimate” dividend portfolio that provides you with …

- No-doubt 6%, 7% even 8% yields – and in a couple of cases, double-digit dividends!

- The potential for 7% to 15% in annual capital gains

- Robust dividend growth that will keep up with (and beat) inflation

This all-star cluster of stocks features the very best of several high-income assets, from preferred stocks to REITs to closed-end funds and more, that combine for a yield of more than 8%.

This portfolio will let you live off dividend income alone without ever touching your nest egg. That means never having to worry about how you’ll pay your monthly bills, and never having to worry about wrecking your retirement account if disaster strikes.

Don’t scrape by on meager blue-chip returns and Social Security checks. You’ve worked too hard to settle when it matters most. Instead, invest intelligently and collect big, dependable dividend checks that will let you see the world and live in comfort for the rest of your post-career life.

Let me show you the path to the retirement you deserve. Click here and I’ll provide you with THREE special reports that show you how to build this “No Withdrawal” portfolio. You’ll get the names, tickers, buy prices and full analysis of their wealth-building potential – and it’s absolutely FREE!