Let’s say you want to lock in a passive retirement income of $80,000 per year.

If you go with what most investors mistakenly see as the safest route, long-term US Treasuries, you’re going to need $3.3 million. That’s because 10-year Treasuries are paying a wimpy 2.4% interest rate today.

Investors who buy Treasuries often shrug off numbers like that. “So what?” they say, adding that Treasuries are about as low-risk as you can get.

Too bad they’re wrong.

If you buy into Treasuries and want to resell them before they mature—perhaps to deal with a big expense that comes out of nowhere—you have a pretty good chance of losing money. Take a look at the movements of the iShares 20+ Year Treasury Bond ETF (TLT) over the past five years:

Treasury Volatility

Here’s what this tells us: if you were unlucky and bought at the peak in mid-2016, you’re down 15.5% in just a few months.

Otherwise, there were several periods in every single year where your purchases would result in you losing money if you needed to sell at those times. And you’d really only come away with a meaningful profit if you were lucky enough to buy at the end of the Federal Reserve’s quantitative easing program in late 2013.

Long story short: buying Treasuries does not protect your capital if you need to access that money before the bond’s term is up. If you’re buying 10-year bonds, that means losing complete access to $3.3 million—just to get the middling yield these investments pay.

Luckily there are better options.

I’m talking about a series of other, higher-yielding investments that can get you the same amount of income with much less cash invested. They’re widely misunderstood by investors, but the truth is they don’t introduce much more volatility than US Treasuries. And that, in my opinion, is a small price to pay for their stronger return potential.

Let’s take a close look at each one, starting with…

High-Yield Investment No. 1: BDCs

Business development companies (BDCs) pool funds from shareholders, borrow against this cash, then lend to small and mid-sized companies. They then return 90% or more of the income from those loans to shareholders. BDCs are a complex sector, but you can think of them as alternative banks that specialize in corporate lending.

You can pick one or two BDCs, but there’s great risk in that. For instance, Fifth Street Finance (FSC) shares have fallen over 63% since their IPO less than a decade ago, and FSC has cut its dividend several times over the same period.

Instead, you can diversify with the UBS ETRACS BDC ETF (BDCS), a fund indexed to a basket of more than a dozen BDCs. Unlike FSC, this ETF has avoided a double-digit decline since its IPO and has handed most investors a nice double-digit total return.

The Value of Diversification in a Single Chart

BDCS yields 7.7% today—over three times what Treasuries pay—so it takes only a third as much capital (just over a million bucks) to get our $80,000 passive income stream.

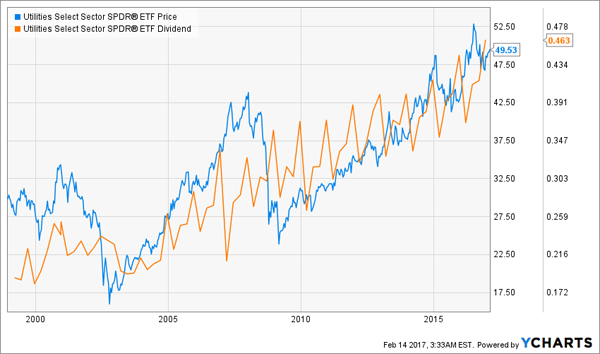

High-Yield Investment No. 2: Utilities

Utilities are famous for being boring, reliable income producers. They’re also strong dividend payers; the Utilities Select Sector SPDR ETF (XLU) has yielded over 3.0% since 2008 and most of the time since its 1999 IPO. This is thanks to slow, steady income growth over time: XLU’s payout has gone up by 245%, or about 5.1% per year, since inception. On top of that, the fund’s price has been steadily climbing since 2009:

Boring Is the New Exciting

Investing in XLU won’t get us as much income as the same amount of cash invested in BDCs would, but at least we only need $2.3 million to hit our $80,000 goal. Plus, payments will very likely go up, where Treasuries are guaranteed to never go up and BDC payments can very easily head lower.

The downside? Utilities have been on a tear since the global financial crisis, so you’d be right to wonder if there’s a correction in the cards.

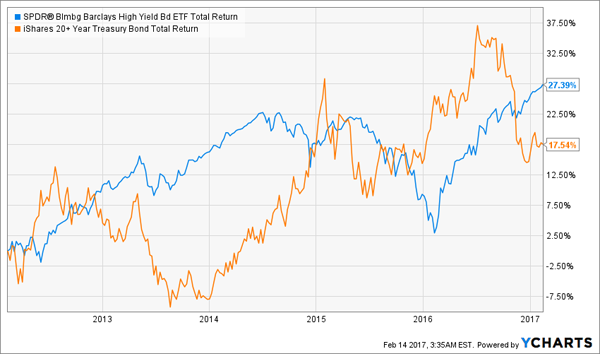

High-Yield Investment No. 3: Corporate Bonds

Many people are turned off by the moniker “junk,” but a good junk-bond fund like the SPDR Barclays High Yield Bond ETF (JNK) offers a 6.0% dividend yield and has outperformed US Treasuries on a total-return basis for the last five years.

“Risky” Junk Beating “Safe” Treasuries

There are downsides to junk bonds, however: they are extremely volatile and can jump all over the place in a short period of time if loan-default rates go up. And we’re now at the highest default rate for high-yield debt than at any time since 2008, so the risks are still present.

Fortunately, there’s an option here that most investors don’t know about. It can actually lower volatility while increasing total returns.

High-Yield Sector No. 4: Covered Calls

Before I get to that option, let me first mention one often-overlooked but powerful way to get high income: a covered-call fund. These funds buy a basket of stocks and sell call options against them—basically selling insurance to investors who have made risky bets against those stocks.

Options are derivatives, a word that makes a lot of people nervous. But we need to remember that these funds sell these derivatives against their assets, meaning the options cannot themselves produce a loss for the funds. Like insurance brokers, these funds are simply collecting extra income by helping other investors hedge their risky bets.

There are plenty of covered-call funds out there. The most popular is the PowerShares S&P 500 BuyWrite ETF (PBP), with about $290 million in assets under management.

PBP yields just 1.7% and its payouts are lumpy. However, the fund has outperformed Treasuries on a total-return basis pretty much since it began:

“Safe” Treasuries Lag Again

The Better Way

PBP has far too low of a yield, which is why I prefer looking for closed-end funds (CEFs)—or funds with a fixed amount of shares that can never dilute shareholder equity—that use a covered-call option strategy. Likewise, CEFs that specialize in junk bonds can also get us a more reliable yield and a higher total return because they are selective about what assets they buy and when they buy them.

Putting It All Together

When it comes to which approach investors should take to getting a higher passive income stream and less liquidity risk than Treasuries, the answer is “all of the above.”

The problem is figuring out when to buy covered-call funds, junk-bond funds, BDCs and utilities, since these funds can quickly go from undervalued to overvalued and back again.

Knowing which of these assets to buy—and when—is no simple task, of course, which is why we developed our “No-Withdrawal” retirement portfolio.

It hands you a yield even higher than what the UBS Etracs BDC ETF (BDCS) pays: I’m talking about an 8% payout you can count on … and double-digit price upside too.

And you don’t have to pile all your cash into a single asset class, like BDCs, to grab that income stream. The 6 undervalued investments in our new portfolio each come from wildly different corners of the market—CEFs, preferred shares, real estate investment trusts and more—which helps keep your nest egg safe.

It’s specifically designed to keep your income rolling in on a modest upfront investment (just $500,000 will hand you a tidy $40,000 a year to start) and without having to sell a single share to do it.

Many of these safe income plays are just about to deliver their next round of dividend hikes, making now a great time to buy in. Click here to get full details on the 6 income wonders in our 8% retirement portfolio and start profiting now.