Which dividend is most likely to be hiked?

Usually, the brand-new payout.

Chief Financial Officers are a conservative bunch. A CFO will only agree to pay a dividend if they know they can:

- Make the payment comfortably.

- Hike the dividend repeatedly for years to come—with said comfort.

The hike part is important because rising dividends drive stock gains. I’m talking about hundreds or even thousands of percentage points in potential gains.

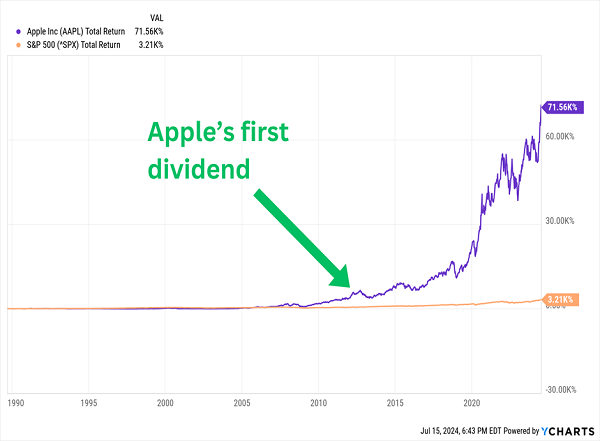

Let’s consider Apple (AAPL) and its inaugural dividend moment. In March 2012, the tech giant initiated a regular dividend of $2.65 per share. The payout was a catalyst for 12 subsequent years of moonshot performance.

Apple Initiates Dividends, Subsequently Soars

Apple now has company in Dividendland. Facebook parent Meta Platforms (META) and Google parent Alphabet (GOOGL) became the latest members of the Magnificent Seven to initiate a payout program.

Both yields are currently less than half a percent. Not enough yet to get our attention, though we will keep an eye on growth.

We do however have five newly initiated dividends that are more generous. Is the next Apple in this bunch? Let’s sort through the payout groceries.

Fidelis Insurance Group (FIHL)

Dividend Initiation Announcement: Feb. 29, 2024

First Dividend Payment: March 29, 2024

Dividend Amount: $0.10 (Quarterly)

Dividend Yield: 2.2%

Fidelis Insurance Group (FIHL) is a relatively new entrant in the field of insurance and reinsurance.

Founded in 2014, incorporated in Bermuda, and also operating out of Ireland and the U.K., Fidelis operates in three segments: Reinsurance, Specialty (some really interesting insurance solutions including aviation, aerospace, marine construction and more) and Bespoke (customized risk solutions, again featuring interesting products dealing with political risk, cyber reinsurance and more).

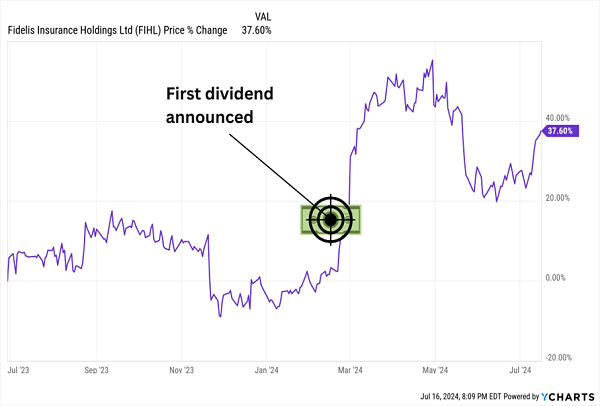

Fidelis’s history as a publicly traded company is even shorter. The company’s initial public offering (IPO) landed in June 2023, with very little fanfare—the company’s $13.10-per-share open was actually below its $14 offer price.

But things have gotten better since then.

A Payday, And a Price Bump

Top-line growth has been consistent since 2020, which is the oldest public data available. Profits have been more variable, which is par for the course for insurers, but on Leap Day, the company announced a banner 2023 in which the bottom line exploded by nearly 10x year-over-year.

No surprise, then, that FIHL decided it was time to share some of its haul. Fidelis said it would pay out 10 cents per share quarterly starting in March—complimenting its existing $50 million share repurchase program.

Insurance is a terribly cyclical market, but Fidelis has a few positive qualities. The specialty insurance business is an area of growth, it’s entering new niches (it just launched a Lloyd’s syndicate), and it’s fairly cheap at current prices.

Super Group (SGHC)

Dividend Initiation Announcement: June 27, 2024

First Dividend Payment: July 17, 2024

Dividend Amount: $0.10 (Annually*)

Dividend Yield: 2.7%

Super Group (SGHC) is an online sports betting and gaming operator that resides in the Bailiwick of Guernsey—a British Crown Dependency in the Channel Islands with fewer people than Canton, Ohio, whose business-friendly taxes and laws make it a popular place for London-listed companies to incorporate.

Super Group is a holding company for two gaming names:

- Betway, a global online sports betting brand that operates in more than a dozen countries

- Spin, a multi-brand online casino offering.

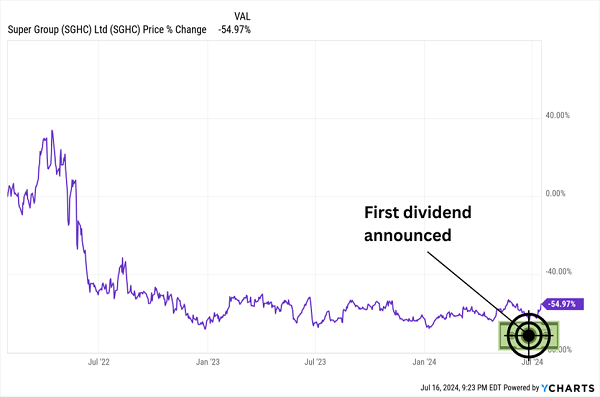

SGHC isn’t just another foreign stock—it’s another recent launch, founded in 2020 and a public company as of January 2022, when it merged with Sports Entertainment Acquisition Corporation, a special purpose acquisition corporation (SPAC).

From a stock perspective, however, things haven’t gone nearly as well as they have with Fidelis, and instead have followed a path familiar to many SPAC investors:

SPACs Can Be Pretty Wack

Super Group is actually in retreat—strategically, anyways. The company recently announced its intentions to leave the U.S. sports betting market (though other operations will remain in the country), and it’s otherwise looking to exit other global markets that have less upside potential.

That’s not to say SGHC is completely unattractive. It recently acquired partner Apricot’s sports betting tech stack, which will help Super Group control tech costs and the pace of product rollouts. And its iCasino operational performance continues to improve.

Despite choppy profitability, SGHC still decided to move forward with a regular dividend initiation near the end of June. Though it did it in an odd way. It said it would pay out 10 cents per share on July 17, 2024, with a target of 10 cents per share annually. So, one would assume this is an annual dividend. But SGHC added that “in the first quarter of 2025, the company’s intention, subject to Board approval, is to pay regular dividends on a quarterly basis.” So while Super Group seems to be signaling that there will be no more dividends this year, 2025 could see four quarterly dividends … but at 2.5 cents per share.

It’s a decent yield to start with, but it’s being paid from a business that’s still trying to figure out its geographical mix in a fluctuating and competitive industry.

Nomad Foods (NOMD)

Dividend Initiation Announcement: Jan. 30, 2024

First Dividend Payment: Feb. 26, 2024

Dividend Amount: $0.15 (Quarterly)

Dividend Yield: 3.3%

Making our way to another exotic location, we have Nomad Foods (NOMD)—a British company that’s headquartered in the British Virgin Islands.

Nomad Foods is Europe’s leading frozen food company, offering up frozen fish products (like fish fingers and natural fish), frozen poultry, frozen meat, ready-made meals, ice creams, and a load of other products. And it does so under a wide variety of names, including frozen-food pioneer Birds Eye, Green Cuisine, Iglo, La Cocinera, Goodfella’s, Belviva and more.

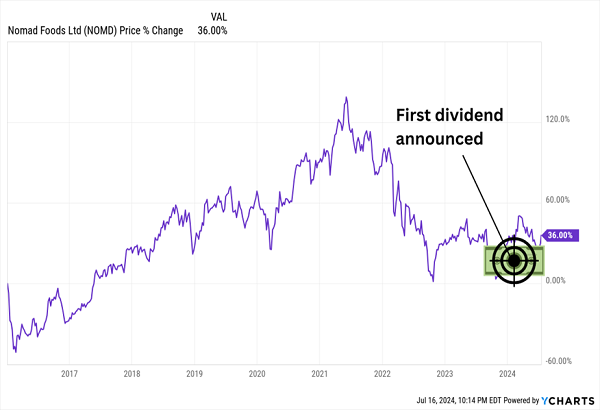

Nomad’s brands are of various ages (Birds Eye has been around for more than a century), but the company itself is only a decade old. It started in 2014 as an investment vehicle, then after buying Iglo Group and Findus Group, it switched listings from the London Stock Exchange to New York, and it has continued its acquisitive streak ever since.

NOMD boasts the slow and steady revenue growth we’d expect from a consumer staples company—perhaps a bit slower than we’d like in places given some of that growth has come from acquisitions.

The bottom line has been less consistent. Over the past couple of years, Nomad has been hobbled by volume declines, as well as higher commodity costs digging into margins. That in turn has sent investors packing from NOMD shares.

An Ice-Cold Couple of Years for Nomad Shares

That said, volumes are trending in the right direction and commodity cost pressures are easing. While analysts see consumer staples-appropriate 3% annual revenue growth over the next couple years, they think the bottom line will cruise ahead at a roughly 10% annual clip.

Nomad itself projected confidence in late January when it initiated its first dividend, just months after it authorized a $500 million stock buyback plan. The 15-cent quarterly dividend comes out to a 3%-plus yield, and translates to a conservative 30% payout ratio.

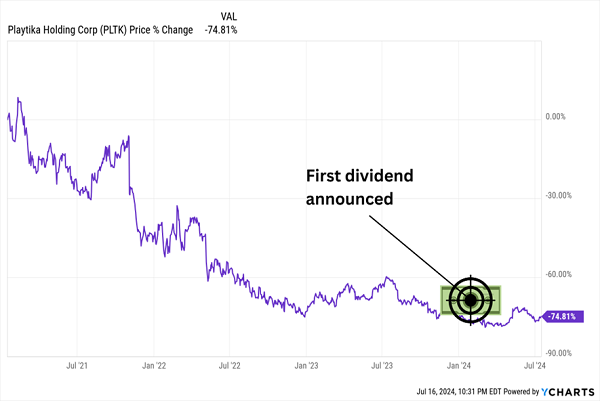

Playtika Holding (PLTK)

Dividend Initiation Announcement: Feb. 26, 2024

First Dividend Payment: April 5, 2024

Dividend Amount: $0.10 (Quarterly)

Dividend Yield: 5.0%

Next, we travel to the Middle East, where Israel-based Platytika Holding (PLTK) develops primarily casino-themed games for countries on just about every continent. Here in the U.S., Playtika is known for titles including Bingo Blitz, Redecor and Solitare Grand Harvest.

Playtika was founded in 2010 and has since changed hands a few times; Caesars Interactive Entertainment bought it in 2011, then sold it to a Chinese consortium in 2016. It then went public in January 2021. But Playtika has been acquisitive itself, buying out Seriously, JustPlay.LOL, Youda Games and Innplay Labs, among others. (It also proposed an acquisition of Angry Birds maker Rovio in 2023 that eventually fell apart.)

These acquisitions have largely taken advantage of—but also are a method of trying to survive in—a brutal mobile games market that has left PLTK shareholders shellshocked.

This Game Doesn’t Look Fun at All

The mobile game market is a brutally competitive one, especially among companies publishing the “free to play” titles Playtika boasts. That said, the market has perhaps been a little too rough on PLTK shares—revenues have been at least stable over the past few years, and while the bottom line has shrunk, it has been by roughly 15% since 2021, with analysts projecting a small rebound this year.

The financials appeared good enough to management that in late February, Playtika announced the beginning of a 10-cent quarterly dividend, which translates to a mighty fine 5.0%. But it also translates to a little more than 60% of the company’s estimated earnings this year, at a time in which management has already said it would also dedicate more capital to additional M&A.

Anyone considering Playtika also has to consider any additional effects of the Israel-Hamas war; last year, some 150 of its 1,100 employees in Israel (3,800 worldwide) were called up to reserve duty.

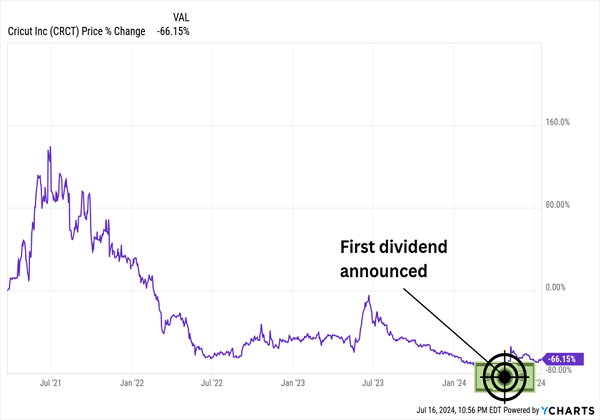

Cricut (CRCT)

Dividend Initiation Announcement: May 7, 2024

First Dividend Payment: July 19, 2024

Dividend Amount: $0.10 (Semiannually)

Dividend Yield: 10.0%

Our journey brings us home to the U.S., with South Jordan, Utah-based Cricut (CRCT)—yet another company that has announced a new dividend in the midst of a deep funk.

Cricut Shares Have Been Cut to Shreds

Walk into a Michaels or Jo-Ann Fabrics, and chances are you’ll come across a Cricut—it’s a machine that lets users turn their ideas into professional-looking handmade goods, such as cards, mugs, T-shirts, even large-scale interior decorations.

But Cricut is more than just its machines—it’s a “creativity platform.” Cricut boasts a pair of subscription plans that offer additional fonts, images, and more, as well as software that integrates its machines with design apps (including its own Cricut Joy App). And both its machines and technology are sold on six continents.

Cricut itself has actually been around since 1969, but it was known as Provo Craft & Novelty up until 2018, when it changed to the current moniker. It went public three years later, in March 2021, and as the chart above shows, things haven’t gone very well ever since.

That same year is when CRCT’s financial performance peaked. Revenues have dropped 40% in the two years since; earnings per share (EPS) have plunged by nearly two-thirds. Both metrics are expected to decline again in 2024, albeit more modestly.

And yet, in May 2024, Cricut surprised many investors by announcing not just a 40-cent-per-share special dividend, but the initiation of a regular dividend, set at 10 cents per share semiannually, for a combined 60 cents, or an eye-popping 10% yield at current prices! They added a $50 million share repurchase authorization just for good measure.

The special dividend wasn’t unprecedented—CRCT unloaded $1.35 per share across a pair of specials in 2023. But another pair of cash outlays, and the promise of regular income going forward?

It’s hard to tell what management’s thinking. Active user and paid subscriber growth is slowing, and engaged users (anyone who has created a project in the past 90 days) are actually on the decline. And as product sales continue to decline, that’s an increasingly smaller influx of fresh blood Cricut can plug into its subscription products.

“Stealth” System Produced 57% and 148% Gains. These Could Be The Next 5 Winners

This feels like a white flag. In this case, skeptical pundits might be right—that management thought they had to make a growth-or-income choice, and it chose income.

Fortunately, we don’t have to make that choice.

I’ve identified five payout winners that aren’t just showering their shareholders with more cash—they’re also forecast to deliver 15%+ annual returns going forward.

By tracing the connection between dividend growth and share-price growth, I’ve uncovered gain after gain for my readers.

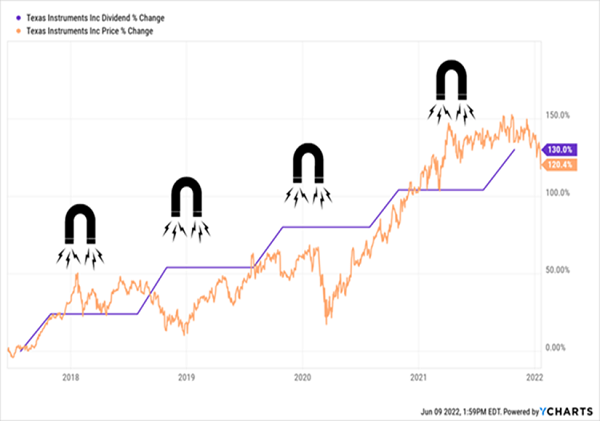

Including Texas Instruments (TXN), whose dividend marched 130% higher during our holding period, driving a 120% jump in the share price!

We Rode TXN’s Rising Dividend to a Massive Gain …

Add dividends and those share price gains together and you get a 148% total return!

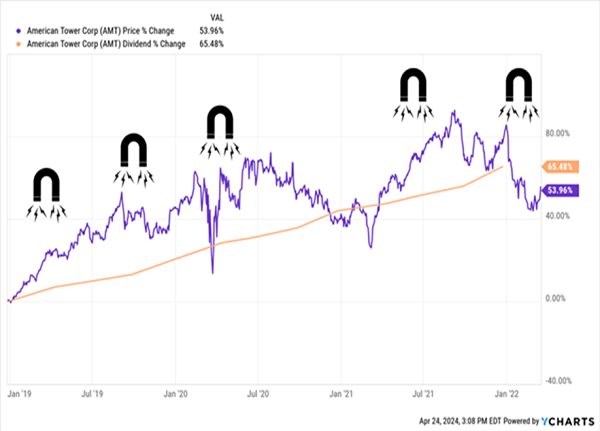

Or American Tower (AMT), whose payout rose every quarter in the little more than three years we owned it, from November 2018 to March 2022, ultimately soaring 65%.

The share price? It soared 54%, resulting in a 57% total return!

… And American Tower’s, Too

Now this “stealth” stock picking system has zeroed in on the NEXT five potential winners, and I can’t wait to show them to you.