Are we having fun yet, my fellow income investor?

We’re now in a bear market, whether the financial media or our intrepid politicians admit it or not. Peak to trough the S&P 500 dropped 21% intraday. Based on closing prices the decline was “only” 18%, however—not quite the technical 20% drop that defines a bear market.

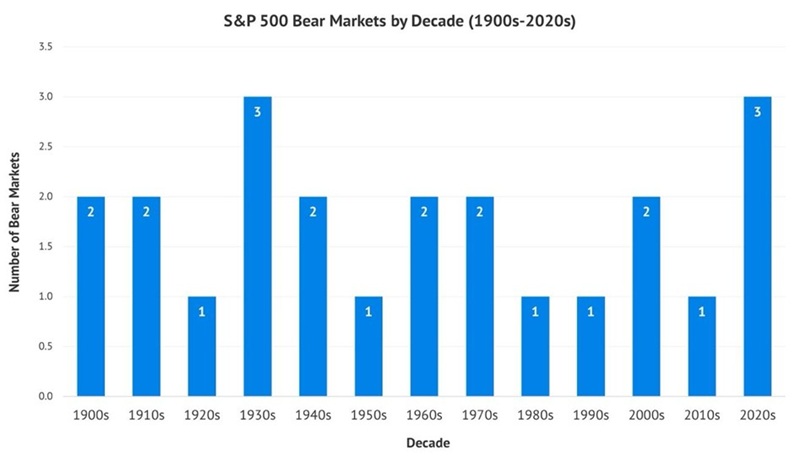

Regardless, let’s not split hairs and call this what it is—the third bear market of the 2020s. Three bears. And it’s only 2025!

You may be wondering, as I was, if this is normal. It is not, my friend. Since 1900 we have averaged 1.77 bear markets per decade. So yeah, three in six years sure is yet another stomach punch:

Last time around, in 2022, we sold early and often and hunkered down in cash. Stocks and bonds were pummeled for nine straight months. There was no point in trying heroics—Benjamins under the mattress outperformed active portfolios. So, we went with the “doomsday” allocation and put many of our payouts on pause for a few months.

It was the most difficult bear market a dividend investor will ever face. Normally we turn to bonds when stocks are uncertain. But that did not work in 2022, because bond prices were dropping faster than their payouts.

Our mission, when we retire on dividends, is to leave our principal intact. But in 2022 both stocks and bonds jeopardized our underlying nest egg, so cash was the only choice.

Fortunately, bear markets tend to last less than a year. Stocks take the stairs up but the elevator down and, on cue, the 2022 bear market ended after nine months. And we went back to a regular dividend-paying portfolio. We made up for our time in cash with price gains, which often follow bear market lows.

Return of capital trumps return on capital when the bear—and Trump tariffs (ha!)—growl.

We have a better landscape to work with here in 2025 because we can buy bonds. Not only do they pay more today than they did three years ago, but these higher interest rates provide us with price “cushions.” If yields come down, we’ll enjoy price gains.

Of course, yields don’t have to come down. The total China tariff rate is currently 145%. This will put upward pressure on imported goods—with the potential for sustained higher prices—over the next six months.

And just last week, as I was putting my kids to bed, I noticed the bond market melting down in the Asia session. The 10-year Treasury rate jumped 12 basis points, over 4.5%. Japan was rumored to be the seller, dumping its sizeable holdings to protest tariffs. The bond meltdown got President Trump’s attention—he announced the 90-day pause on most tariffs the following day.

I don’t blame you for not wanting to stay up at night babysitting bonds through Asia trading windows. China—ye of 145% levies—owns $760 billion in long-term Treasuries. Think they may be looking to sell?

China dumping bonds would obviously put pressure on long rates. This, in fact, may be the reason why long-dated yields are not lower in the face of slowing economic data.

The “short end” of the yield curve, on the other hand, is insulated from overseas sales. It follows the Fed, which is still relatively high, at least for the time being. When the Fed begins to cut again, these divvies will compress, so this may be the best time to find safety and yields between 4.3% and 5%.

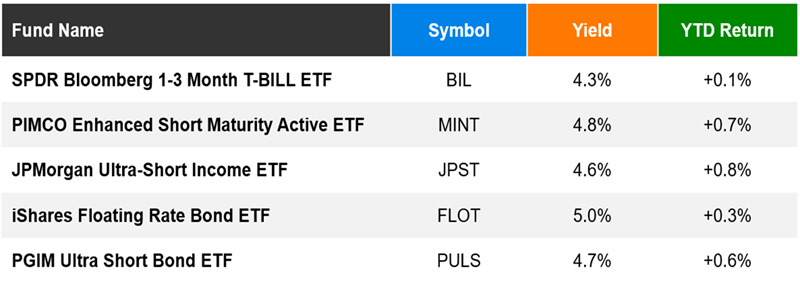

These low-duration bonds are not at risk when a trade war adversary begins to sell. Here are five of the safest, most liquid short-term bond funds on the market today:

SPDR Bloomberg 1-3 Month T-Bill ETF (BIL) invests in ultra-short-term US Treasury bills. It is plenty liquid and will protect our capital. BIL yields 4.3%.

The downside with BIL is that its yield may not last. When the Fed cuts rates, BIL’s yield will decrease, too. But this “dividend cut” will not eat into the price, so your principal will remain intact. (The same caveat and logic follow for our four other funds.)

PIMCO Enhanced Short Maturity Active ETF (MINT) pays 4.8%. This fund is actively managed by “blue blood” fixed-income leader PIMCO. Dan “The Beast” Ivascyn and his team buy high-quality, short-duration assets. Thanks to their expertise, MINT benefits with a bit of extra yield beyond what short-term US Treasuries pay.

JPMorgan Ultra-Short Income ETF (JPST) yields 4.6% and owns short-term investment grade bonds, both fixed and floating rate.

iShares Floating Rate Bond ETF (FLOT) pays the most at 5.0%, but it is down 1% month-to-date. FLOT buys investment-grade floating-rate bonds, and its “floaters” are a bit shaky as rates drop. Sock FLOT away on the watch list. We’ll revisit it on the other side of the upcoming economic downturn, when stagflation becomes a theme.

Finally PGIM Ultra Short Bond ETF (PULS) pays 4.7%. PGIM is another top name in Bondland. PULS buys ultra-short duration bonds with higher yields than BIL.

Of course it is difficult to retire on dividends using funds that only pay 4% or 5%. This requires $2 to $3 million in capital—we don’t all have piles of cash like this lying around.

Fortunately there are safe, simple monthly dividend payers dishing up to 10% right now. Ten percent on a million dollars is $100,000 per year in dividend income. We bank this without touching principal. Now we’re talking.

These funds are secure and built to handle recessions. The steady every-30-day payments help smooth out the stock market’s daily—ahem—gyrations these days. Here’s how to turn your portfolio into a monthly income machine.