I love “secret dividends.” They’re one of the few safe ways to collect yields up to 11.9% in a 1.9% world!

They’re also a great way to protect your portfolio against big market pullbacks, too. If you find yourself wincing every time you check your stocks, perhaps some secret dividends would help steady the ship.

“I’m 11 years older now. Brett, I just can’t have a repeat of 2008,” my new subscribers often share.

“Now tell me which of these dividends will survive a bear market like that. I want to buy the safest yields,” they continue.

Fortunately I’m no stranger to dividends that thrive in bear markets. We fittingly launched the Contrarian Income Report months before the market’s tantrum in 2016. The S&P 500 promptly dropped 10% as a welcome present!

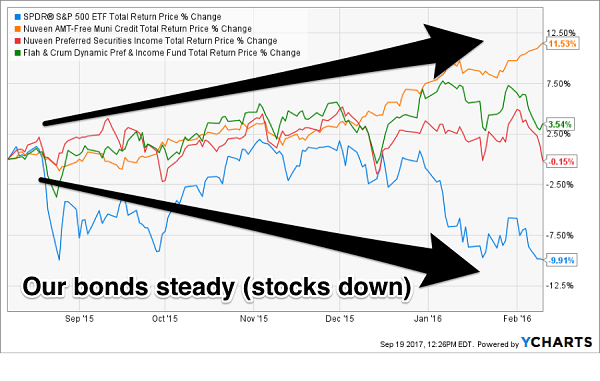

It was no problem for our steady, underappreciated dividends, however. In fact, subscribers who focused on their own holdings rather than the financial news likely have missed the broader carnage altogether. Our core bond fund holdings (orange, red and green lines below) not only continued to pay their 7% dividends, but they also averaged a 5% price gain while stocks (blue line below) were swooning:

What Pullback? Secret Bond Funds Sail

(It’s sneaky yields like these that have helped my subscribers to 10.6% annualized gains since inception. Most of these profits have come in the form of cash dividends. Our retirement portfolio is the ultimate “absolute return” vehicle thanks to under-the-radar dividends.)

I’ll share more on my unique high yield approach in a moment, First let me introduce you to five more stocks that are off the beaten path. Each of these sticks out for its dividend potential, and we’ll discuss a pair of 11%-plus yielders to boot.

Innovative Industrial Properties (IIPR)

Dividend Yield: 2.1%

Let’s start out with a modest yield in an area that almost no one would think to trawl for income:

Pot.

Innovative Industrial Properties (IIPR) is a rare bird that combines the breakneck growth of the budding marijuana industry with the dividend-producing power of real estate investment trusts (REITs). It owns specialized industrial and greenhouse buildings that it leases out to medical-cannabis producers. The company was only founded in December 2016, so the portfolio is understandably modest, but it features 16 properties across 11 states, spanning from coast to coast.

Importantly IIPR also boasts a sale leaseback program to marijuana producers hungry for cash. In short, it acquires real estate from these producers, which inject the funds into their own operations, while leasing their former real estate from IIPR. A couple months ago, I summed up the benefit to income investors:

Why IIPR? It’s the only real estate investment trust (REIT) that works with weed growers. As a publicly traded company, it gets to borrow money at much lower rates than it collects from its cannabis clients. As a REIT, IIPR is obligated to dish most of its profits back to its shareholders as dividends. The result is a good old-fashioned payout boom, a 200% increase in less than two years.

Those dividends are growing because IIPR is growing – like a weed, no less. Its first-quarter results included a 146% year-over-year boost in rental revenues and a 275% pop in adjusted funds from operations (AFFO).

Unfortunately, this is one case where being “weird” hasn’t allowed IIPR to fly under the radar. At all. Investors currently are paying dearly for its red-hot growth–a whopping 53.7 times AFFO that’s double or triple most REIT valuations.

Innovative Industrial Properties is simply too expensive at current levels. But it’s a force of nature worthy buying on a considerable dip.

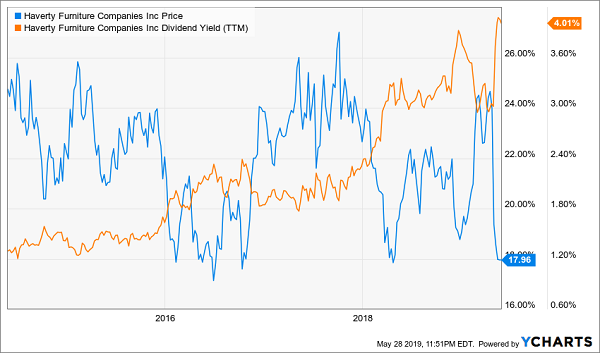

Haverty Furniture Companies (HVT)

Dividend Yield: 4.1%

Furniture companies are another brand of rare and rarely covered stock. For good reason: It’s a boring business where product lifecycles are literally measured in decades, and growth typically is at the whims of economic strength.

That said, when the economy is robust, and a furniture stock is trading at a nice valuation while serving up a decent yield, it at least merits a closer look.

Haverty Furniture Companies (HVT) is a well-established regional furniture company that was founded in 1885–before the Dakotas, Montana and Washington were admitted to the Union. It sports more than 100 showrooms across 16 states primarily in the South and Midwest.

It’s also in operational purgatory. On the one hand, the company has reported two consecutive years of declining revenues, and HVT shares have lost roughly 25% of their value in about a month after reporting a dreadful quarter that saw comparable-store sales plunge 4.7%. Analysts were looking for a 0.8% gain.

The flip side? Earnings and free cash flow have at least been trending in the right direction over the past half-decade, and 2018 was its best year on both fronts in at least the past five years. Moreover, much of Haverty’s recent tumult has come courtesy of the U.S.-China trade war. “The tariff imposition has been disruptive, particularly to our important motion upholstery category and some key dining and bedroom collections,” CEO Clarence Smith said in the report.

It’s tempting to speculate on HVT, whose price is at the bottom of its five-year trading range while its yield is at the top. At the same time, this is a company that has indeed been rangebound for the majority of the past decade – and analysts don’t expect the kind of growth that would catalyze a new leg higher anytime soon.

Sluggish Haverty Is Cheap, But Not a Bargain

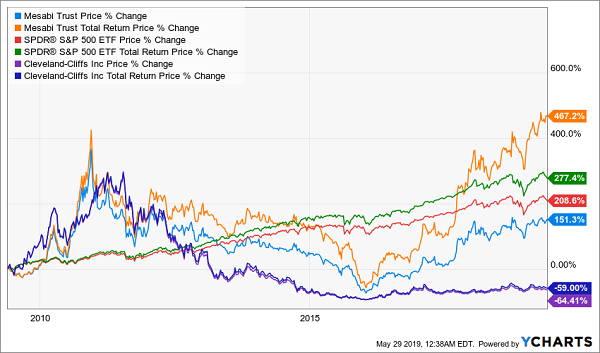

Mesabi Trust (MSB)

Dividend Yield: 11.9%

Most income investors know the traditional haunts: Utilities, REITs, MLPs, BDCs, CEFs.

But even the well-informed might have skipped “royalty trust day” in dividend school.

Royalty trusts are a very specific type of corporation that primarily exists here in the U.S., with a few in Canada, to own the rights to the energy or mineral assets. They don’t operate any facilities. They just collect royalties. But these companies enjoy a setup similar to REITs and BDCs in that their profits aren’t taxed at a corporate level as long as a high level of them are redistributed to shareholders as dividend-esque “distributions” (much like an MLP). These are typically high-yield plays, but interestingly, they can terminate–sometimes by a specific year, or other times after a certain level of proceeds are doled out to shareholders.

Mesabi Trust (MSB) derives income from the iron-producing Peter Mitchel Mine in Babbitt, Minnesota, that is operated by a Cleveland-Cliffs (CLF) subsidiary called Northshore Mining Company.

One mine. That’s it. And it’s a painfully specific operation at that:

Northshore pays royalties to the Trust primarily based on the selling price of pellets shipped from Northshore’s pellet plant at Silver Bay, Minnesota, on Lake Superior approximately 45 miles from the mine, plus a significantly smaller royalty based on tons of ore extracted at the mine.

While iron prices have only appreciated about 37% over the past decade, Mesabi Trust has ripped off 150% price gains … and an eye-popping 467% total return once you factor in its double-digit payout. (Meanwhile, look at what miners like poor Cliffs have done in the same time!)

When an 11% Yielder Becomes a Rip-Roaring Growth Play Too

Mesabi ultimately is a commodity play centered around iron ore and steel, which means tariff headlines could easily throw this royalty trust for a loop at a moment’s notice. But it has proven over the past few years that it can certainly pack a total-return punch.

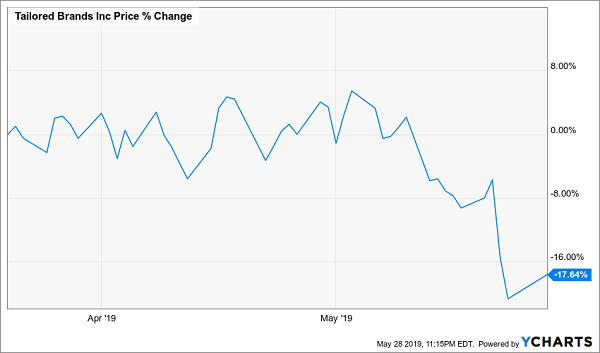

Tailored Brands (TLRD)

Dividend Yield: 11.4%

Apparel retailers are a dime a dozen, but Tailored Brands (TLRD) sticks out because of its particular niche. That is, as the owner of Men’s Wearhouse and Jos. A. Bank, it’s the dominant name in the men’s professional-wear space. In fact, there is no other stock like it.

For better or worse.

When I discussed this “apparent train wreck” in March, I pointed out that “Shares have been bludgeoned over the past year, losing roughly two-thirds of their value since May 2018. Some of the biggest hits included disappointing same-store sales growth in June, a report in December that Men’s Wearhouse traffic was sliding (thanks to several factors, including increased competition from the likes of Bonobos) and another report in January in which the company lowered its fourth-quarter guidance on weakness at Jos. A. Bank.”

I also cautioned readers that “cheap stocks can get even cheaper.”

And Indeed, This One Did

TLRD has been bludgeoned to the point where it almost seems crazy not to buy the stock. It yields more than 11%. It trades at a mere 3 times forward earnings estimates–and unlike other hyper-low-valued stocks, its future profits indeed are projected to grow.

But while Tailored might be an interesting swing trade for agile day traders, this is not a buy-and-hold income play for anyone responsibly planning for retirement. It’s facing a considerable sea change in consumer tastes–not just for its wares, but also in how people shop. That’s a recipe for instability.

PetMed Express (PETS)

Dividend Yield: 5.9%

Pets have long seemed a way of American life, but over the past couple of decades, they have become a monster business–and a monster opportunity.

The American Pet Products Association says American spending on pets was $21 billion back in 1996. Twenty years later, that figure more than tripled to almost $67 billion–then $69.5 billion in 2017, $72.6 billion in 2018. And spending across pet food, medications, vet care and more is expected to reach $75.4 billion by the end of this year.

PetMed Express (PETS) is an online pet pharmacy that many people will know as 1-800-PetMeds. For a time looked like it was going to hit the moon banking off this trend.

The company has spent the past five years consistently growing its top and bottom lines, and it’s been increasingly able to squeeze cash out of its pet-pharma business. The legitimate fundamental story, coupled with a sudden surge of awareness of this space that even prompted the launch of an ETF last year–the ProShares Pet Care ETF (PAWZ)–as well as absurd premiums on the stock drove the stock to more than triple between 2015 and 2018.

PETS has since collapsed from a high of more than $50 last year to current prices below $20.

Despite its 15 minutes of fame, PetMed is still a less-traveled stock in a niche industry (PAWZ only has $27 million in assets under management and only trades a few thousand shares a day). It’s been growing dividends regularly for years, and can easily afford its payout with room to spare, and the nosedive in its stock has brought it to a much more reasonable 10 times profit estimates.

But PetMed fell for a reason. Expectations have wildly outpaced actual results, with the company whiffing on profit estimates by 20% or more the past two quarters, and missing the mark in three of the past four quarters. That’s really disconcerting when you consider that Wall Street recently hacked its estimates for PetMed, projecting a 10% drop in profits this year followed by a lackluster recovery next year, accompanied by low-single-digit sales growth. Getting some of the blame is increased competition as the rest of the world gets wise to this lucrative market.

The yield is right, and so is the price. But the story has fizzled out of this story stock.

This “Secret Dividend” Trick Will Net You 28% Annually in America’s Safest Stocks

I love secret dividends, but the opportunity has to be right – and stocks like HVT and PETS don’t exactly give me the warm fuzzies.

Instead, I’ve set my sights on drawing massive total returns of nearly 30% in the unlikeliest of ways: massive, safe blue chips that yield next to nothing.

Wait, what?

I know, I know. I typically hound market trackers because blue chips typically churn out OK-but-not-great returns of about 8% on average. However, I’ve recently put together a method that takes “growthy” safe stocks – think juicy blue chips such as Visa (V) – and squeezes giant distributions out of them. We’re talking 28% in annual total returns that’s more than triple the S&P 500’s annual average.

It sounds crazy. It’s absolutely unorthodox. But this is one of the best income opportunities I’ve come across in years – and I’ve even put my money where my mouth is, putting my own personal accounts to work in this strategy.

This method takes Wall Street’s most growth-first, income-last blue chips such as Google parent Alphabet (GOOGL), and it turns them into “double threat” holdings that put traditional dividend payers like Procter & Gamble (PG) and Coca-Cola (KO) to shame. We’re talking double-digit upside, 8%-plus dividends … and no, we’re not doing this by using complicated options schemes or arcane leveraged funds, either.

We’re doing it via my new income-generating discovery: “Dividend Conversion Machines.”

These stocks have specialized businesses that allow them to do what other stocks simply can’t: They wring high-single-digit dividends from some of the most skinflint companies in America. One of my Dividend Conversion Machines takes Visa’s 0.7% payouts and magnifies it to 9.7%. Another one can take Google’s 0% and produces a 9% yield out of thin air.

This isn’t a complex options strategy. It’s not high-risk derivatives. It’s certainly not the “next Bitcoin.” This is a stunningly safe strategy that’s essentially the same as buying traditional American blue-chip stocks. In fact, I’ll even show you the four steps you’ll need right now:

- Launch your web browser.

- Go to your trading account.

- Instead of entering a buy order for, say, Disney by entering the stock’s “DIS” symbol, enter the 3-letter code for one of my 4 Dividend Conversion Machines instead.

- Instead of getting Disney’s 1.6% dividend, start collecting an 7.5%+ income stream!

That’s it!

The incredible investments I’m going to show you in just a second are 100% as safe as investing in “stodgy” blue chips – except you get retirement-enhancing dividends and BIG upside too! In fact, they even have another leg up on traditional blue chips: They pay out their dividends monthly, which is ideal for retirees who need that income to pay their bills – and ideal for investors planning for retirement because those dividends will compound even faster!

Let me show you how to reap 28% in annual returns from miserly blue chips today. Click here and I’ll introduce you to these four “Dividend Conversion Machines,” including names, tickers, buy prices and full analyses – AND throw in three other income-generating bonus reports – all for absolutely NO COST to you.