If you feel trapped “grinding out” dividend income with classic 3% or 4% payers, you can double your payouts (or better) immediately by moving to closed-end funds, or CEFs. In fact, you can often make the switch without actually switching investments. You do need to make sure you avoid five common mistakes when doing so – which I’ll explain in a moment.

But first, let’s explore the stock-for-CEF trade. For example, American International Group’s (AIG) investors can potentially trade in their 2.2% dividend yields for the Gabelli Dividend & Income Trust Fund’s (GDV) 7% payout. AIG is GDV’s largest holding amongst a list of blue chip dividend payers plus growers like Wells Fargo (WFC) and Verizon (VZ).

Superstar money manager Mario Gabelli runs his namesake GDV. He combines his yields with growth and leverage to create his outsized yield – which he delivers investors every month, to boot.

Sounds like a sweet deal, right? His investors get the benefit of a legendary money mind along with his access to ideas and cheap money.

CEFs can indeed be sweet deals for investors when done right. On the other hand, there are dividend traps out there – funds that pay fat yields today, but “eat their own institution” in order to pay their distributions. Long term, they are losers.

Here are five checkpoints to avoid trouble, and narrow down a watch list of CEFs that will provide your portfolio with secure high yield.

Point #1: Don’t Freak Out Over Management Fees

Most investors are conditioned by their experience with mutual funds and ETFs to search out the lowest fees, almost to a fault. This makes sense for investment vehicles that are roughly going to perform in-line with the broader market. Lowering your costs minimizes drag.

Closed-ends are a different investment animal, though. On the whole, there are many more dogs than gems. It’s an absolute necessity to find a great manager with a solid track record.

Great managers tend to be expensive, of course. I wouldn’t pay a premium to invest with anyone, though…

Point #2: Demand a Discount

Premiums are rare in the closed-end space, and usually reserved for “rock star” managers and hot ideas. PIMCO’s funds would often trade at a premium when “Bond King” Bill Gross was running the show. In fact, three still do trade at double-digit premiums, with the most excessive above 45% today:

Yes, you read right – there are people who pay $1.45 for $1.00! Personally I prefer not to be down big out of the gate.

Instead, I demand a discount when I buy closed-ends. While you won’t find any deals for 20 cents on the dollar, you will find excellent funds selling for 10-15% discounts from time-to-time – such as these three “Bond God favorites”.

Point #3: Don’t Worry Blindly About Higher Rates

Many first-level investors are running away from closed-end funds, claiming that their “free leverage lunch” is nearing an end with higher rates on the horizon. Plus, they say these funds are going to see more competition from other fixed income assets looking increasingly attractive, making them less so.

Sounds like a good theory – but it’s flat wrong in practice. Let’s look at the most recent meaningful rate hike cycle to see why.

In June 2004, Fed chair Alan Greenspan began boosting rates from then-historic lows. Over a two-year period, he increased the federal funds rate from 1% to 5.25%. An earthquake.

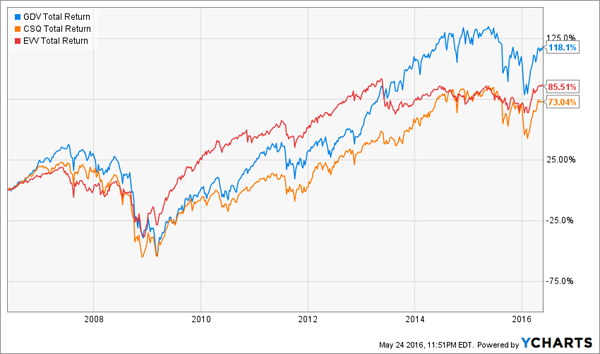

How’d CEFs perform? I checked the historical performance of GDV along with two other prominent funds – the Calamos Strategic Total Return (CSQ) and the Eaton Vance Limited Duration Income Fund (EVV). And all three outperformed the market during Greenspan’s aforementioned run:

Higher Rates No Problem for Top Closed-Ends 2004-06

Point #4: Consider the Fund’s Strategy Carefully

Make sure your manager is earning his fee with a strategy that actually adds value. Many closed-end funds are nothing more than glorified mutual funds. They buy a bunch of stocks, declare a much higher distribution and “hope” for capital gains to make up the difference.

Visit the homepage of any CEF you’re considering. Read through the most recent reports and the letters from management, and figure out if their strategy is adding value or just paying their own salaries.

There’s an easy way to verify – check the track records.

Point #5: Look for Long Term Track Records

Funds have histories, as do their managers. Look at both.

To check a fund’s track record, I subscribe to a paid product called YCharts.com. I use a “total return” calculation, which includes dividends – this is important because most of the gains from CEFs come in the form of payouts. So “price only” is not an accurate reflection of value gained over the long haul.

There can be a wide variance in performance over multiple years. Take the three funds I mentioned earlier – laggard CSQ returned just 73% over 10 years, while GDV made its investors 118.1% richer. It paid to go with the superstar manager…

The Best Manager Delivered the Best Returns

My Favorite 3 Closed-End Funds Today

If you think GDV, CSQ and EVV are exciting, wait till you see the three other closed-end picks I have for you. These “slam dunk” income plays pay 8.0%, 8.4% and even 11% dividends.

Plus, they trade at 10-15% discounts to their net asset value (NAV) today. Which means they’re perfect for your retirement portfolio because your downside risk is minimal. Even if the market takes a tumble, these top-notch funds will simply trade flat … and we’ll still collect those fat 8% to 11% yields.

Most likely, they’ll jump 10-15% to close the “free money” discount … and we’ll still collect those fat dividends!

It’s only a matter of time before other investors ditch their paltry 3% and 4% payers and find their way over to these “slam dunk” income plays, so the time to buy is now, while they still trade at deep discounts to NAV.

Click here to get the complete story and the names of these three rock-solid retirement picks now.