These popular dividends were taken away in 2020. But rumors of a payout comeback are swirling, and the best time to buy these stocks may be right now.

Before America goes on a vacation binge, that is. See, these dividend payers will directly benefit from travelers being rereleased into the wild. We have been homebound for nearly a year now. (Sorry for the reminder!) But brighter days are ahead, and I know that my family is already booking out travel into 2022.

Should we pick up some hotel stocks while we’re online? After all, hotels will naturally benefit from our restlessness, as will their landlords—the real estate investment trusts (REITs) that were tossed aside this time last year.

The answer is, there are some opportunities remaining in lodging, but we have to be nimble as well as choosy.

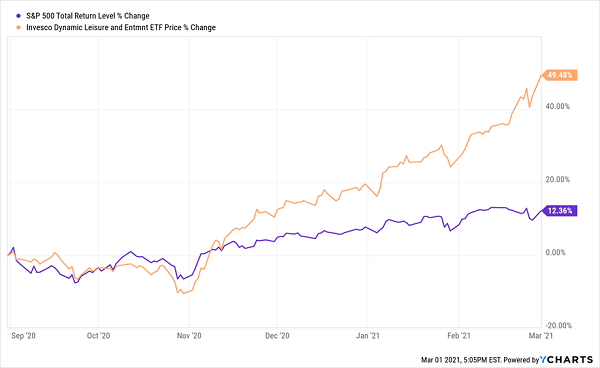

Just look at the performance of the Invesco Dynamic Leisure and Entertainment ETF (PEJ), a collection of stocks that include theme park owners, restaurants, hotels, booking sites, ticket vendors and casinos. This all-in-one economic-recovery bet has quadrupled the market over the past six months.

No One’s Sleeping on the American Vacation

You’ll see similar performance out of many of the major hotel stocks. Which makes sense, because the American Hotel & Lodging Association (AHLA) reports that

“Compared to last year, 36 percent of Americans expect to travel more for leisure in 2021, while 23 percent expect to travel less and 42 percent about the same.”

But there’s more to that report. Despite the fact that survey-takers were aware that vaccinations were merely a matter of time, AHLA’s other takeaways weren’t nearly as bullish as you’d expect. Among them:

- “Half of U.S. hotel rooms are projected to remain empty.”

- “56% of consumers say they expect to travel for leisure, roughly the same amount as in an average year.”

- “Business travel is forecasted to be down 85% compared to 2019 through April 2021, and then only begin ticking up slightly.”

We shouldn’t blindly throw money at the hotel space. Let’s take a closer look at five popular lodging payers. The current dividends aren’t particularly exciting, but there are three comeback stories in the works and we might get the best price on these stocks right now.

Wyndham Hotels & Resorts (WH)

Dividend Yield: 1.0%

Normally, you and I wouldn’t give a 1% yield the time of day. But many hotel and even hotel REIT dividends were reduced or even eliminated outright, so investors in this space need to focus on dividend recovery. In this case, WH cut its quarterly payout from 32 cents per share to 8 cents in the middle of the pandemic, but it has kicked off 21 by doubling the payment to 16 cents—still not great, but things are heading back in the right direction.

Wyndham itself—which includes its namesake brand, La Quinta Inn, Ramada, Dolce, Tryp, Dazzler and numerous other brands—appears to be one of the best plays on a recovery in vacation travel. The hotel chain saw revenues plunge by more than a third in 2020 and sustained deep net losses, but it’s positioned for much better things in 2021.

The primary reasoning is that 70% of Wyndham’s bookings come from leisure travelers. That compares favorably to say, Marriott (MAR), where only 40% of bookings came from leisure travel.

But what’s also compelling is that, of that remaining 30% for Wyndham, “two-thirds comes from the infrastructure industries, including construction crews, utility workers and engineers,” according to CEO Geoffrey Ballotti, and the remaining third is from logistics industries. Both have been showing signs of improvement, and the former could be especially potent should the Biden administration move on to long-awaited infrastructure legislation after its stimulus negotiations.

However, while WH shares have joined in the recovery, they haven’t been nearly as boisterous as other hotel names or the broader travel/leisure industries. And they’re only roughly flat from where they were at the start of 2019.

Is the Market Sleeping on This Hotel Recovery?

But that doesn’t make Wyndham a value. Shares trade at almost 34 times this year’s earnings estimates of $1.97 per share, and 22 times 2022 estimates of $2.87. It made $3.28 back in 2019. That means WH is not only trading at sky-high valuations, but it’s doing so when no one anticipates a full return to normalcy for several years out.

Extended Stay America (STAY)

Dividend Yield: 2.2%

Extended Stay America (STAY) caters to travelers looking for longer booking periods, and they doubled down on this type of customer during the pandemic.

“Longer-term bookings have always comprised a majority of the revenue at Extended Stay America, but shorter transient travel still accounted for about a third of room revenue pre-pandemic,” Extended Stay America CEO Bruce Haase said back in August 2020. “That shrank to about a fifth of room revenue over the second quarter.”

While STAY still cut its dividend early on during the pandemic, from 23 cents per share to just a penny, Extended Stay suffered shallower losses than many of its peers as a result. That allowed it to pay a 35-cent special “catch-up” dividend to shareholders at the start of 2021. And more recently, STAY resumed its dividend growth, bumping the payout up to 9 cents quarterly.

That flexibility should serve STAY well as it attempts to navigate the next change in travel trends. But it has already been richly rewarded, too. Shares sit 12% higher than where they sat at the start of 2019, and trade at 33 times this year’s earnings estimates. And, like Wyndham, that’s despite the fact that “profit normalcy” isn’t expected for several years down the road.

The Cat’s Out of the Bag on Extended Stay, Too

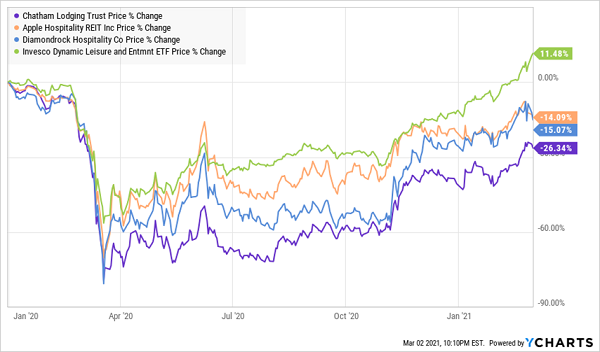

The picture is pretty clear here. Values are scarce among traditional hotel stocks. But maybe we can find a few bargains among their landowners.

Unlike the market at large, these REITs are still cheap. They wallowed through 2020 while other vacation-related stocks soared. No wonder. REITs’ primary use is as an income funnel, but many names had to shut off the dividend spigot entirely to make it through.

But now we have a chance at a “double whammy”—depressed prices and the potential for dividend reinstatements/growth as operations normalize.

Hotel REITs Haven’t Begun to Catch Up

For instance, there’s Chatham Lodging Trust (CLDT)—a previous winner for my Contrarian Income Report subscribers. This REIT owns a few dozen properties that house numerous hotel brands, including Residence Inn, Hyatt, Homewood Suites, Courtyard and Hampton Inn across 15 states and the District of Columbia. It’s not cheap, at less than 16 times 2022 AFFO estimates, but it’s not atrociously overpriced, either. While it’s difficult to be sure when any company will resume dividend payments, a few analysts are taking a stab; B. Riley Securities thinks CLDT will resume at 10 cents per quarter in Q421. That would be a roughly 3% yield right out of the gate.

DiamondRock Hospitality (DRH) owns 31 hotels and resorts in “gateway” cities across North America and the Virgin Islands. Its brands include well-known chains such as Westin and Hilton, but also properties such as Chicago’s The Gwen, and Havana Cabana in Key West, Florida. Its portfolio of “drive-to” (as opposed to fly-to) destinations could be key as travelers choose to travel, but perhaps still avoid flying germ tubes until they’re a little surer about COVID dying down. DRH has delivered negative funds from operations (FFO) since Q2 2020, but is expected to return to positive FFO by Q3 2021. It’s fair to assume some level of dividend resumption shortly thereafter. But it’s not all that attractively priced, at 19 times 2022 FFO estimates.

Apple Hospitality Trust (APLE) could be one of the best bets in the group. If nothing else, it’s more reasonably priced at less than 9 times its 2022 FFO estimates. This REIT has a large portfolio of more than 230 primarily upscale, “select service” hotels in 88 markets across 35 states. It’s most heavily concentrated in Marriott and Hilton (HLT) hotels, but it also has three Hyatts (H) and two independents under its umbrella. Q4 2020 results were on the disappointing side, though seasonality came into play; more encouraging are improving occupancy trends in January and February 2021. A few estimates show APLE’s FFO getting pretty close to normalcy by 2022, and if expectations for 2021 earnings are on target, we could see a resumption in the dividend by the end of the year.

Sky-High Dividends You Can Count on for DECADES

But do you really want to wait for another few quarters for dividends to merely restart, nevermind how long it will take to get back to the juicy yields you actually want?

The hotel space might make for an interesting swing play and a few “moonshot” dividend swings. But if you’re looking for truly generous and reliable income, you can find that today in my “Perfect Income” portfolio.

As dividends dropped like flies in 2020, income investors were sent scattering for better sources of income. But unless you perfectly bought the March dip, you’re mostly out of luck. Even if you had a million dollars in cash to plunk down right now, the S&P 500 would earn you just $15,000 a year! You’d do even worse with a traditional 60/40 portfolio!

Forget about retiring happily on that level of income. You can’t even survive on it!

Thankfully, the dividend-rich stocks in my “Perfect Income Portfolio” can and do deliver so much more.

Most of my readers have told me that these stocks have doubled and even tripled the dividends they were earnings from their old income portfolios. (And in a couple of rare cases, readers reported a 4x jump in their regular checks!) That alone is an upgrade, but the Perfect Income Portfolio delivers that level of cash while also …

- Paying those dividends consistently, predictably and reliably.

- Surviving, even thriving, in market crashes.

- Delivering double-digit returns across several safe investments.

- Gambling your hard-earned nest egg on flimsy day-trading strategies, options contracts or penny stocks.

Stop obsessively staring at your 401(k) or IRA and let me show you the stocks and funds you need to stabilize your retirement … and even teach you more about this incredible strategy itself, so you better understand exactly what you’re investing in.