Who cares what financial “pundits” are yapping about? Show us the money. Show us what the insiders are scooping up!

I was going to say “cue the Drake meme.” Let me go ahead and tee that up.

Insider buying, generally speaking, is more predictive than insider selling. The C-level types may sell stock to buy new boats or bribe their kids’ way into college. (Ha!)

But when these guys and gals buy, it’s for one reason. They believe their stock’s price is undervalued, and that it’s due to pop.

Insider buying activity has been quiet of late. No surprise there: The market is setting new highs on the regular, and many execs are nervous about buying when their stocks are at or near all-time highs.

That said, I’ve had my eye on a handful of recent insider buys in some of Wall Street’s top payers. These companies are yielding 6.4% to 12.3%. These insider buyers are not only confident that their stock price is heading higher. They also believe in the dividend.

Let’s start with a 6.4% dividend that had four of its big bosses buying in May.

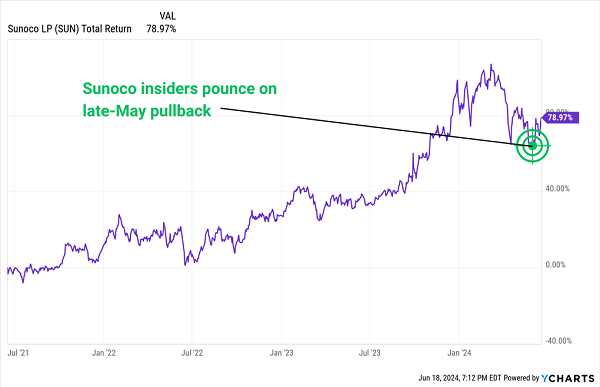

Sunoco LP (SUN)

Distribution Yield: 6.4%

Recent Noteworthy Buys:

- Chief Executive Officer Joseph Kim: 5,000 shares ($252,516) on 5/23/2024

- Chief Sales Officer Brian A. Hand: 2,000 shares ($99,180) on 5/24/2024

- Chief Operating Officer Karl R. Fails: 3,000 shares ($150,540) on 5/24/2024

- Chief Commercial Officer Austin Harkness: 1,000 shares ($49,740) on 5/29/2024

Sunoco LP (SUN), a master limited partnership (MLP) that distributes motor fuel to approximately 10,000 convenience stores, independent dealers, commercial customers and distributors in more than 40 states. And if the name sounds at all familiar, it’s connected to Energy Transfer LP (ET)—specifically, Sunoco’s general partner is owned by ET subsidiary Energy Transfer Operating LP.

And in May, Sunoco’s insiders went on a spending spree, buying up more than a half a million dollars’ worth of SUN shares.

The question is: Why?

Insiders typically don’t come out and tell us why they’re buying, so we need to read the tea leaves. For instance, Sunoco’s Q1 2024 results, posted in early May, were decent, and the company guided its 2024 adjusted EBITDA higher. And a few days before that, Sunoco raised its distribution—by 4%, to 87.56 cents per share—for the second time in a year. (That’s all the more important given that prior to 2023, SUN hadn’t improved its distribution since 2016.)

But I’m inclined to believe it’s more about two other factors.

For one, in late May, SUN shares retreated to their lowest point since 2023—a nice buy-the-dip moment to anyone looking for one.

Did They Nail the Bottom?

It also could be optimism over the company’s $7.3 billion acquisition of NuStar Energy LP, which closed May 1. NuStar, whose assets include 9,500 miles of pipeline and 63 terminals, is expected to give Sunoco a growth path in the Midwest, providing additional geographic diversity (Sunoco doesn’t have much of a presence in the region). NuStar also features a Permian crude gathering system and growing ammonia and renewables businesses.

There’s plenty of potential brewing, though still some questions to be answered. Sunoco is still figuring out the extent of any commercial synergies it might enjoy. And management has signaled that it’s looking to unlock value in its crude oil business—they won’t sell those assets outright, but they’re open to options including a joint venture.

I’ll also point out that Sunoco is an MLP that comes with the added complication of a K-1 tax form, which I try to avoid.

Granite Ridge Resources (GRNT)

Dividend Yield: 7.4%

Recent Noteworthy Buys:

- Director Michele J. Everard: 1,000 shares ($6,620) on 5/20/2024

- Director John F. McCartney: 1,007 shares ($6,590) on 5/21/2024

- Director Griffin Perry: 2,000 shares ($13,080) on 5/23/2024

- Director John F. McCartney: 500 shares ($3,275) on 5/23/2024

- Director Matthew Reade Miller: 7,700 shares ($50,050) on 6/3/2024

- Director Thaddeus Darden: 3,000 shares ($18,870) on 6/6/2024

- Director Matthew Reade Miller: 8,500 shares ($50,150) on 6/14/2024

- Chief Executive Officer Luke C. Brandenberg: 5,000 shares ($29,650) on 6/14/2024

- Director Thaddeus Darden: 7,000 shares ($41,300) on 6/14/2024

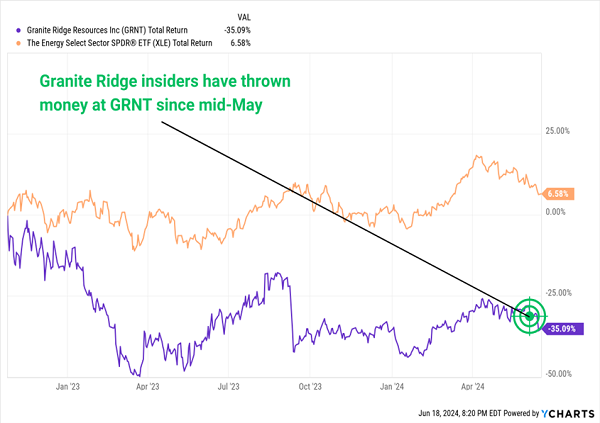

Granite Ridge Resources (GRNT) is an oddball of an energy firm from top to bottom.

Granite Ridge touts itself as a “hybrid” firm—part oil & gas company, and part private equity firm. It doesn’t actually operate anything. Instead, it invests in a diversified portfolio of production and acreage across the Permian Basin, Eagle Ford, Bakken, Haynesville and DJ Basin.

So, rather than drill wells and extract oil itself, Granite Ridge instead invests in more than 80 public and private hydrocarbon operators that do the work instead.

It’s also worth mentioning that this is a newer company—one that hit the public markets not by IPO, but via special purpose acquisition company (SPAC). Investment firm Grey Rock Investment Partners merged in October 2022 with Executive Network Partnering Corporation (the SPAC).

GRNT’s results since coming public have been dreadful—even with a generous dividend, shares have lost more than a third of their value during a period in which the energy sector is just above breakeven.

But Lately, Execs Are Buying GRNT Shares Hand Over Fist

Insiders bought about $30,000 worth of shares in mid- to late May while the stock treaded water, then really started to pile in with $190,000 worth of purchases as the stock dove in June.

It’s difficult to see any catalysts on the horizon. And the company’s financial profile is a mixed bag. Granite Ridge’s short track record does include decent production growth, and it sports pretty low leverage of just 0.4x net debt to adjusted EBITDAX. But the company has gone from sporting $51 million in net cash at the end of 2022 to $117 million in net debt at the end of Q1 2024. Meanwhile, Q1 earnings of 12 cents per share only just covered its 11-cent dividend, while the company actually burned $1 million in cash for the quarter.

Most oil-and-gas investment opportunities are heavily reliant on commodity prices, which can make for a bumpy ride. Adding an opaque, private equity-esque structure on top of that doesn’t help matters—especially when we can get similar yields out of more straightforward energy plays.

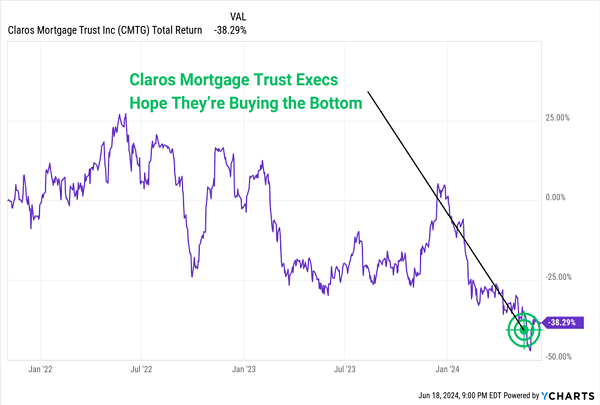

Claros Mortgage Trust (CMTG)

Dividend Yield: 12.3%

Recent Noteworthy Buys:

- Director Vincent Salvatore Tese: 6,000 shares ($43,581) on 5/23/2024

- Director Vincent Salvatore Tese: 1,000 shares ($8,248) on 5/23/2024

- Chief Executive Officer Michael J. McGillis: 15,010 shares ($110,172) on 5/24/2024

- Chief Executive Officer Richard Mack: 44,000 shares ($319,000) on 5/28/2024

- General Counsel Jeffrey D. Siegel: 5,000 shares ($36,150) on 5/28/2024

- Chief Executive Officer Richard Mack: 116,000 shares ($832,880) on 5/28/2024

- Chief Executive Officer Richard Mack: 40,000 shares ($276,000) on 5/29/2024

Claros Mortgage Trust (CMTG) is a member of one of the highest-yield industries on the market: mortgage real estate investment trusts (mREITs). Claros specializes in originating senior and subordinate loans on “transitional” commercial real estate assets, including multi-family residential, hospitality, office, mixed-use and other properties. Its $6.7 billion loan portfolio is predominantly (98%) senior loans; a similar percentage is floating-rate in nature.

The basic mortgage REIT business goes like this: An mREIT buys mortgage loans and collects the interest. They make money by borrowing “short” (assuming short-term rates are lower) and lending “long” (if long-term rates are, as they tend to be, higher). It’s a great model when long-term rates are steady or, better yet, declining. A drop in long-term rates makes existing mortgages more valuable because newer loans pay less. But if long-term rates rise, like they have over the past few years, mREITs get killed.

And Claros Is No Exception

Off the cuff, I think the buying spree can be chalked up to the stock hitting all-time lows since the company’s 2021 IPO, combined with a “rates have to come down eventually” mentality.

Management might be right, but if they’re not, they and their shareholders could continue to suffer.

On a pure price basis, the stock has been cut in half since 2021. The mREIT has even pulled off a dividend cut in its short history—a 32% reduction in 2023 to the current 25 cents per share. Even then, distributable earnings—a non-GAAP measure favored by CMTG—were just 28 cents per share for all of last year, which wasn’t nearly enough to cover the payout. Even worse? Claros delivered a 12-cent distributable loss in the first quarter of 2024.

Even if rates improve, this is a portfolio with growing higher-risk loans and non-accruals above 10%. That’s not exactly a place of strength.

Give Me 5 Minutes, And I’ll 5X Your Retirement Income

Obviously, these insiders know something we don’t, but remember: Insiders are biased to think they’ll get the job done—and sometimes, they don’t.

Me? I’d prefer to avoid stocks that lurch every time oil dips or Jerome Powell sneezes. What good is a 12% yield today if we don’t know whether it will be cut to 9%, 6% or worse in a year?

If you need a can’t-miss retirement cash machine that you want to hold for decades, you need stocks and funds that will stand on their own.

That means no relying on the Fed.

No relying on oil prices.

No relying on a Cinderella economy in perpetuity.

And if you’re thinking “No way those kinds of stocks exist,” think again. Because these are exactly the kinds of names I hold in my “Perfect Income” portfolio.

We don’t chase trends. We don’t time the market. In my “Perfect Income” portfolio, we simply target high-yield investments (roughly 5x the S&P!) and hold on to them, no matter what the Fed, Congress or the rest of the world throws their way.

Perfect, right?

In addition to having high-single-digit and even double-digit yields, every single holding must check off several crucial boxes:

- They DO pay consistently, predictably and reliably.

- They DO survive—and even thrive—in market crashes.

- They DO deliver double-digit returns, with safe, secure investments.

- They DO require minimal management time—just a few minutes every month!

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!