There’s a clear pattern natural gas prices repeat time and time again. We’re going to pounce on it now—and grab ourselves a growing 7.4% payout as we do.

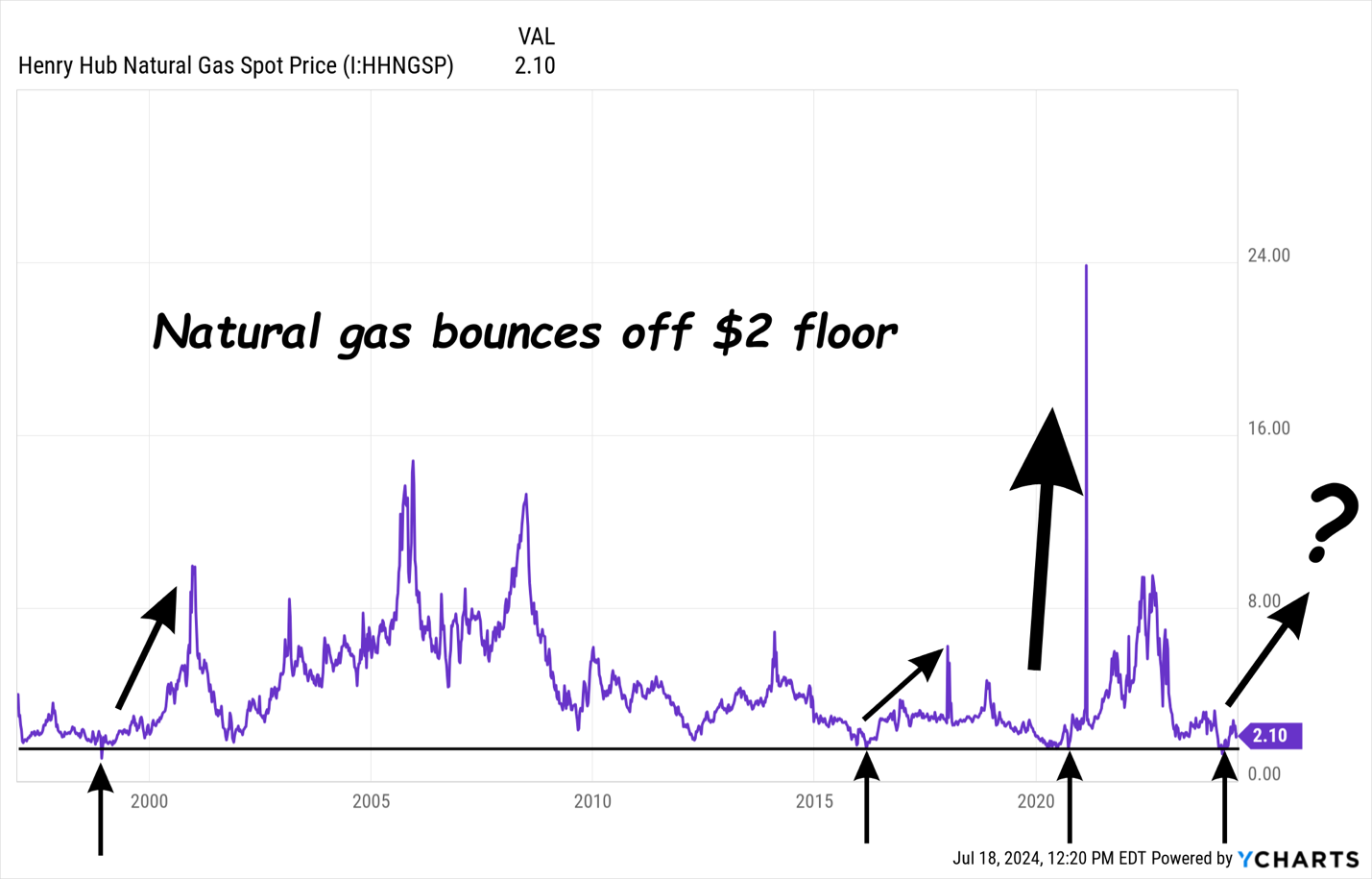

I’m talking about the “natty’s” $2 price floor. Every time it drops to that level (or below) it takes off. Check it out:

Natural Gas’s $2 “Trampoline Act”

It just goes to prove that the cure for low prices is low prices! To play this pattern, we want to buy after gas bottoms. Now is that time.

Think about it: We’re moving toward winter in North America (where temps are expected to be below those of last year’s “non-winter”). Europe is bringing in more liquified natural gas (LNG) as it continues its turn away from Russia. Then there’s China, whose economy is still set to grow 5% this year, boosting its LNG demand.

Which brings me back to that growing 7.4% “natty dividend.” It’s a Canadian firm that’s tapping into US growth—and making some canny moves overseas, too.

I’m talking about Enbridge (ENB), which has 74,000 miles of pipeline across North America. The northern gas giant (which trades on the NYSE, by the way) flies below the radar in the US, but it shouldn’t: it moves about 20% of the gas used here every year.

That’s poised to grow, just as the US brings more manufacturing home. Enbridge recently closed its purchase of the East Ohio Gas Company and it’s on track to close other buys it announced last year—in Utah, Wyoming, Idaho and North Carolina—by the end of 2024. In all, these deals add about 7 million customers.

These are big buys. To put them in context, Enbridge has roughly 4 million customers in its home country.

Growing in Gas—and Globally

Beyond that, ENB recently agreed to form a joint venture that’ll perfectly position it to grab a bigger slice of the growing export market.

It’s recently entered into a joint venture that consists of the company’s Rio Bravo pipeline (starting up in 2026) and two operating lines that haul gas from the critical Permian Basin in Texas to export terminals on the Gulf Coast.

Meantime, management is wisely not putting all its eggs in the “natty” basket. ENB also owns a renewable-power business that includes stakes in offshore wind farms in France and Germany. Green power is still a small slice of the firm’s profits, but it’s growing fast, with earnings before interest, taxes, depreciation and amortization (EBITDA) jumping 100% in the first quarter of 2024.

Management also says it has now reached its goal of cutting emissions intensity by 35% by 2030 and is 20% of the way to reaching its goal of net-zero by 2050.

Adding renewables and measurable emissions goals are smart for a firm with global ambitions like Enbridge. Beyond cutting its reliance on gas, these moves keep it on the right side of regulators.

A Classic “Tollbooth” Business

The beautiful thing about Enbridge is it’s basically a “tollbooth,” charging customers to use its pipelines, most of which are already built and hardly need any maintenance. That essentially creates a dividend that feeds on itself. These “tolls” either flow to us as dividends or fuel growth through acquisitions—which go on to grow that 7.4% dividend!

And there’s every reason to believe those tolls will keep growing.

First, let’s talk rate cuts. As rates decline, high-yielding plays like ENB will attract a lot of investors who get “shaken loose” from Treasuries and other guaranteed investments.

These folks will also love the company’s long (29 straight years!) string of payout hikes. In that time, investors have banked a tidy 12% annualized in dividends and share price gains, as of the end of Q1.

Moreover, the payout is well covered, with Enbridge paying 60% to 70% of distributable cash flow yearly as dividends. That’s fine because its infrastructure is built out. It is a cash cow.

Finally, there’s that bounce in gas prices we talked about a second ago.

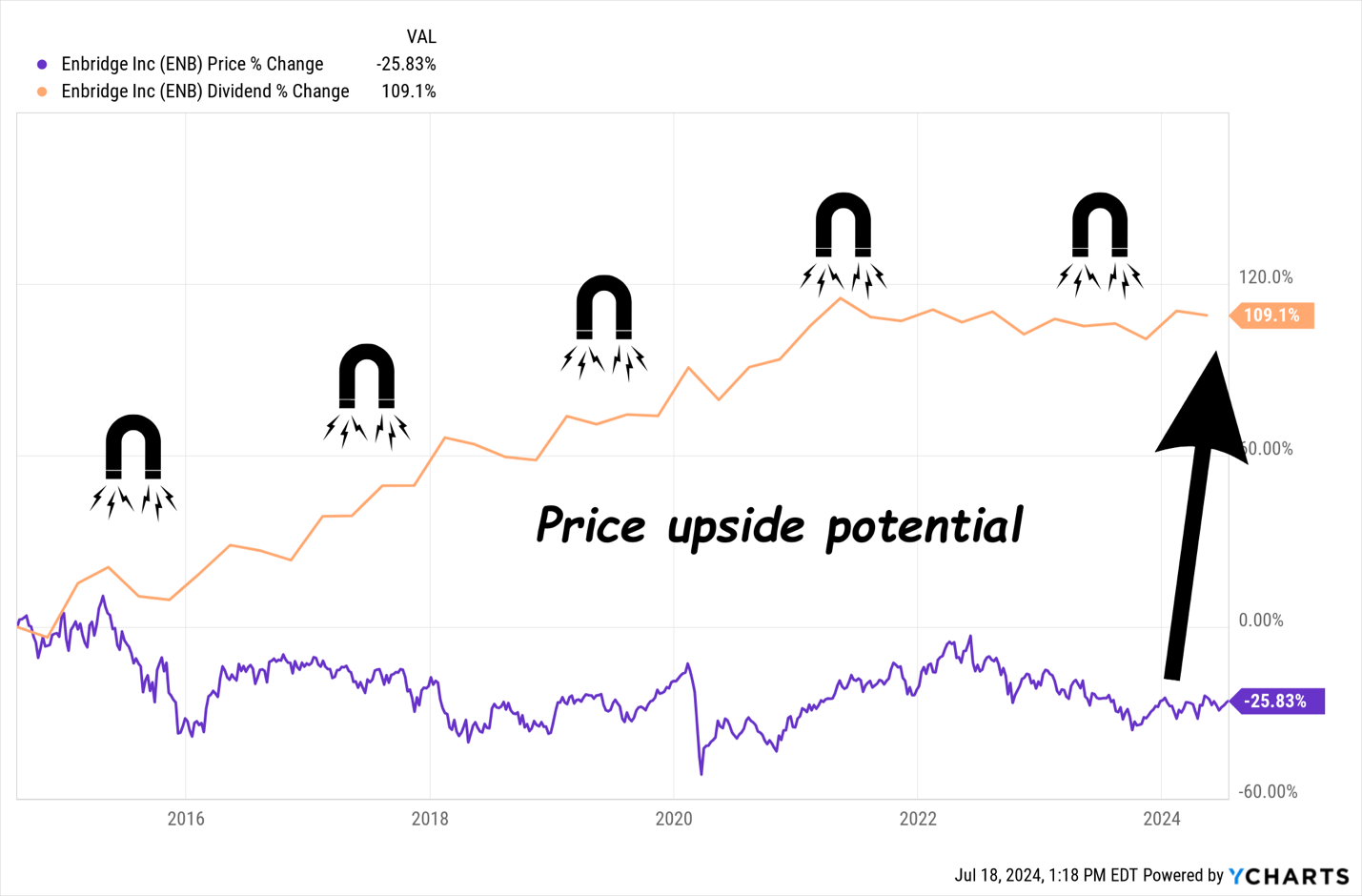

Yet despite all this, Enbridge’s share price has fallen far behind its dividend, which has more than doubled in the last 10 years. The payout also looks like a bit of a basket case when it’s translated from Canadian dollars—or “loonies,” slang for Canada’s currency, not its people—are translated into greenbacks:

ENB’s “Loonie” Payout Is Stronger Than It Looks

This “Dividend Magnet” is clearly due! If you’ve been reading my columns, you know that dividend growth is the No. 1 driver of share prices: Where the payout goes, the stock price follows. So when a gap like the one above opens, it’s a buying opportunity.

Keep in mind also that the 28% loss you see above is misleading because it’s on a price basis. Factor in ENB’s high dividend—something screeners like Yahoo Finance and Google Finance do not do—and you see that shareholders saw a 30% total return in that time (with payouts reinvested).

A Great Buy When the Greenback Falls (Which It’s About To)

Here’s something else that’s set to end Enbridge’s bad-luck streak and give that dividend an extra boost for US investors: When the Fed starts cutting rates, the soaring US dollar will re-enter Earth’s orbit. This will boost Enbridge’s numbers when they’re translated from loonies into greenbacks.

One thing that’s holding the Canadian dollar down is the fact that the country’s central bank has already started cutting rates. But the Bank of Canada doesn’t like to get too far ahead of the Fed, as doing so would drive down the value of the loonie and raise the cost of imports (and inflation).

As the “rate gap” closes, the loonie should strengthen against the greenback.

While we wait for that currency kicker, let’s collect this secure, stable 7.4% payout. Even if the greenback’s decline versus the Canadian buck takes longer to show up, no problem: ENB will power the payout higher on its own. Its distributions have totaled $34 billion over the past five years. Management expects this to top $40 billion in five more years, a 17%+ increase.

5 Dividends Booked for Yearly 15%+ Gains—Forever (Recession or No)

Enbridge is the perfect example of a “recession-resistant” dividend. Because let’s face facts: Even with the growth of renewable power, natural gas is going to stay in high demand. It’s just too deeply rooted in our everyday lives.

And Enbridge doesn’t care: It’s smartly planted its flag in the renewable space, too!

And as we just saw, the stock is cheap in relation to its payout growth now. And its dividend is growing. Both of these strengths help steady its share price in a pullback—and let us collect that fat 7.4% payout in peace!

ENB is just the start: I’ve uncovered 5 MORE “recession-resistant” picks with these exact same strengths: stable stock prices and surging payouts, backed by products that’ll stay in high demand, no matter what the economy is doing!

The time to buy these “recession-resistant” plays is now. Click here and I’ll tell you more about them—and give you the opportunity to download a free Special Report revealing their names and tickers.