“And what can we do to get better shots?”

Your fulltime income strategist and part-time basketball coach asked his team of fifth and sixth graders for their ideas. Or, at least, tried to.

Then a ball bounced. After coach specifically said hold balls for a second time. This third infraction ended the conversation.

“That’s it—on the line. Start running.”

When coach says run, the players don’t really have a choice. Get moving in practice or lose playing time in the games they all love.

Likewise, when the government tells an industry that there is a cap on their profits, well, they’d better get moving too.

“Fat cat” financial lender stocks have tanked since the Oval Office asked for a 10% national cap on credit card interest rate. This went from a campaign slogan to a formal request to Congress. Ugly reaction from some stocks.

Capital One (COF), for one, shed 9.1% last week. The 10% cap created a hard ceiling on the company’s net interest margin (NIM), installing a much lower ceiling on its business model. What’s in your wallet? Less NIM for you!

The industry CEOs know it’s ugly. Everyone’s favorite financial villain, big boss at JPMorgan (JPM) Jamie Dimon, called the proposal an “economic disaster.” (Jamie always talks his book.) Bank of America (BAC) meanwhile is scrambling to design a “capped” card. Which will voluntarily put a lid on its profits.

Google searches for “credit card limit” are spiking amid the cap chatter. It’s ugly out there in the financial sector. But this has presented a “baby with the bathwater” buying opportunity. Indiscriminate selling gives us opportunity.

Visa (V), for example, is not a bank. It’s a financial plumbing tollbooth. Yet, it’s off 8% over the last month! Silly investors. They miss the distinction:

- The Banks (like Capital One) risk their own capital to lend money. They need high interest rates to maintain their fat profit margins.

- A Network (Visa) takes a small fee on every swipe.

Visa doesn’t care if the interest rate is 10% or 30%. To be blunt, they don’t care if the user pays the bill or defaults! They only care that the card is swiped. Visa processed $15 trillion last year—the caps won’t touch that. It’s a misunderstood growth model that features “Stablecoins” as the next big growth driver.

The real pivot, though, is from “capped” banks to “uncapped” energy. The regulatory hammer is flexing on financials. But Washington is doing just the opposite with energy pipelines. In fact, the administration is peeling back red tape and rolling out the red carpet.

Pipelines are becoming the “boring” cash machines that banks used to be. They charge fixed fees to move natural gas and oil. And the sector is gushing so much free cash flow that they are raising payouts…and unlike the banks, the pipelines earn without having to fight Washington. Energy production is a priority for this administration, and these companies directly benefit with less regulation.

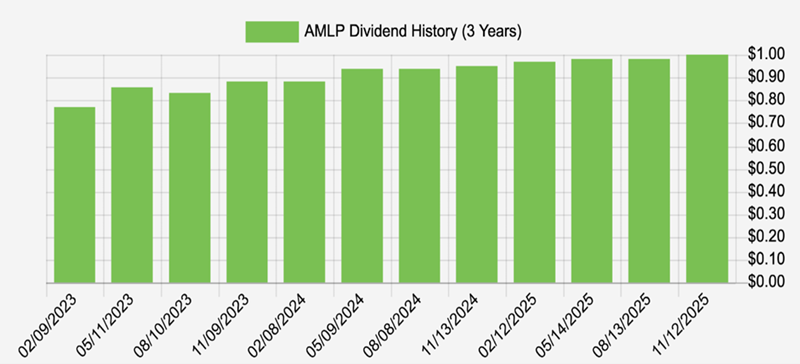

My preferred way to play this trend, which will run through at least 2028, is the Alerian MLP ETF (AMLP). AMLP owns a basket of midstream MLPs (master limited partnerships), the pipeline and infrastructure companies that mint fee-based cash flow. These businesses don’t need $100 or even $80 oil. They merely require traffic.

And traffic is what the US energy system does in 2026. We produce. We refine. We export. Oil is cheap but the pipes are still filling up. Whether prices are high or low, the tolls are getting paid.

And so are we, collecting an 8.1% yield from AMLP!

The fund provides us with a paperwork advantage, too. It is structured as a C-corporation fund, so shareholders receive a 1099. No K-1s, the tax headache many income investors endure when they buy individual MLPs.

AMLP also hikes its payout prodigiously:

AMLP Raises Its Divvie Regularly

What a contrast with banks like Capital One! They are fighting for their fat-cat lives against a 10% cap. Meanwhile, energy pipelines quietly toll the cash flow, free of regulatory scrutiny, paying us 8.1% to hold them.

This is how we live off $500,000…practically forever. By buying elite 8.1% dividends that are favored by the current administration.

Of course, there’s no need to dump a full $500K portfolio into AMLP alone. Diversify! Let’s start with these 3 incredible monthly payers dishing out dividends up to 14.9%.