Oil is up, and everything else is down. Stocks. Bonds. Even gold, the traditional safe haven!

Real estate stocks are on sale as well. Which means we contrarians need to go shopping. Today we’ll look at four real estate investment trusts (REITs) yielding between 6% and 15%.

Right before the conflict started, I mentioned that we were looking at an attractive setup for price appreciation in REITworld.

As the Fed cuts rates, the dividends that REITs pay become increasingly attractive to income investors. Money markets don’t pay 5% any longer. Neither do many bond funds. But REITs pay …

And rates are likely to continue lower due to the rollout of AI across the economy. Automation is capping wage growth. Customer support, for example, is well on its way to being automated. Next up we’ll see bookkeeping, compliance and even legal work increasingly handled by machines. Softer inflation gives the Fed room to cut more than Wall Street expects.

The longer-term outlook has not changed. (A big hint for anyone with a mature, big picture mindset!) But in the short term, the Federal Reserve has pushed “pause” on its rate-cutting trend.

Earlier this year, we could chalk it up to economic data. Now? The central bank is clearly in wait-and-see mode because of the Middle East.

“The thing I really want to emphasize is that nobody knows,” Fed Chair Jerome Powell recently said. “The economic effect [of the Iran war and oil disruptions] could be bigger, they could be smaller, they could be much smaller or much bigger. We just don’t know.”

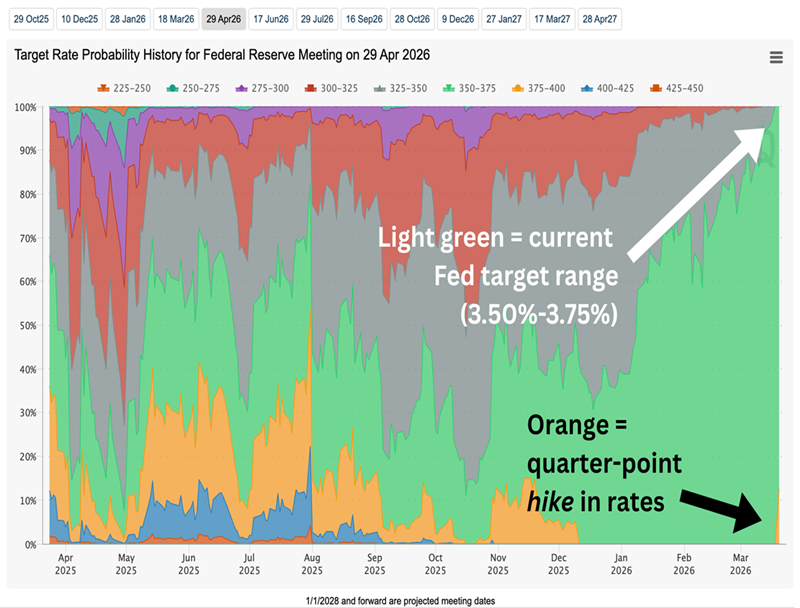

As a result, the market has all but given up on any additional near-term relief in interest rates. FedWatch, which uses 30-day Federal funds futures prices to determine the probability of changes to the Fed’s target rate, shows an 88% likelihood that the Fed will stay put at its late-April meeting.

And, In Fact, There’s a 12% Probability That Rates Go Up

Source: CME FedWatch

That’s misery for REITs, which thrive when borrowing costs fall and their dividends look good in comparison to shrinking bond yields—but struggle when rising rates produce the opposite effect.

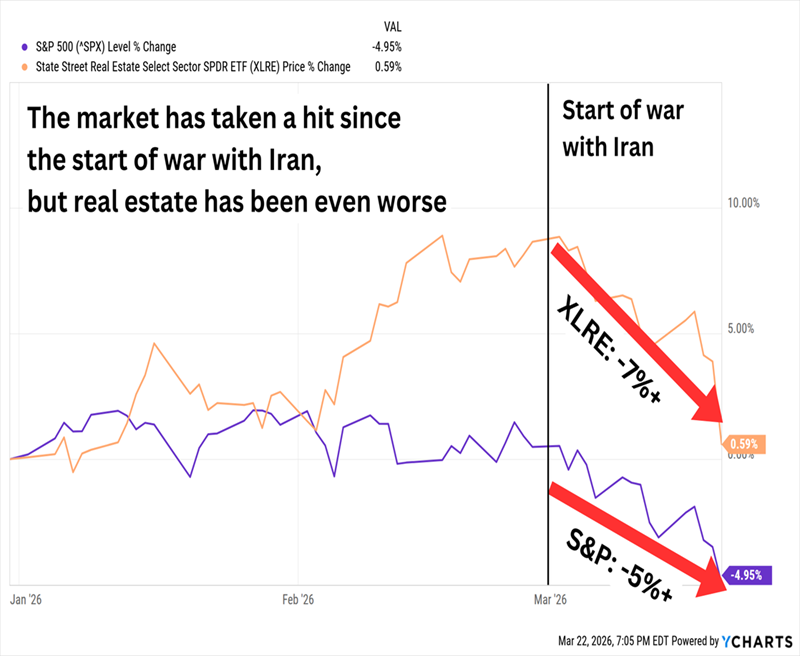

Virtually All of Real Estate’s 2026 Gains Have Been Erased

Again: The longer-term drivers of lower interest rates are still intact for now, which means this could be an ideal time to look for REIT deals. On my radar for a closer examination are these four landlords, which currently dole out between 6.1% and 14.6%.

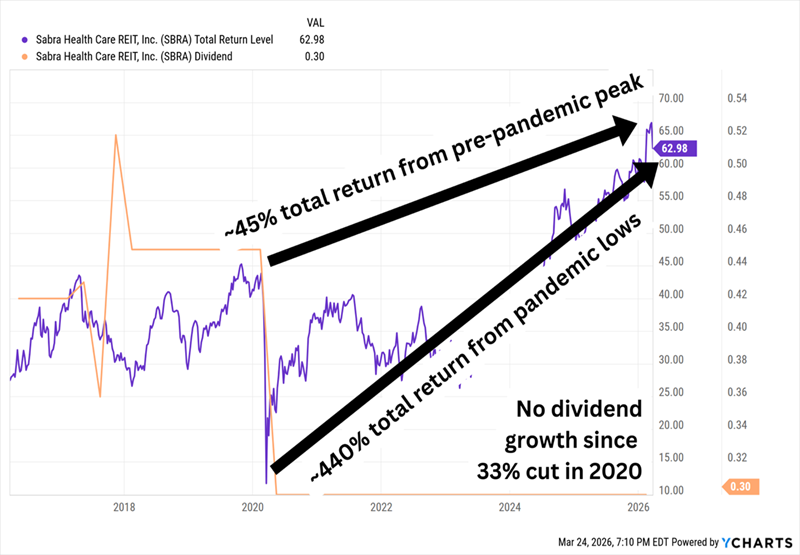

Sabra Health Care REIT (SBRA)

Dividend Yield: 6.1%

Sabra Health Care REIT is a senior-focused healthcare play with roughly 360 property investments across the U.S. and Canada.

A little less than half of the portfolio, as measured by annualized cash net operating income (NOI), comes from skilled nursing and transitional care real estate. Another quarter or so is managed senior housing, with the remainder split among behavioral health properties, leased senior housing and specialty hospitals, among others.

The COVID crisis delivered a major shock to this type of real estate, but the long-term trends have remained in its favor—and that continues today. Supply is low. Pricing power is high. And Sabra is looking at expanding its senior housing operating portfolio (SHOP) via acquisitions.

As a result, shares have simultaneously been less volatile than the market but also plenty productive. In fact, the stock has steadily been making its way toward pre-COVID highs.

Returns Look Even Better When We Include the Dividend, But …

Sabra’s distribution hasn’t budged since slashing it by a third during the depths of the COVID doldrums.

It’s not for lack of room. SBRA pays 30 cents per share quarterly, so $1.20 across the year. Estimates for this year’s adjusted funds from operations (AFFO) are $1.60 per share. That’s a 75% AFFO payout ratio, which leaves room for at least some growth. But even though many other REITs have returned to dividend growth post-COVID, it’s not exactly surprising that Sabra has been hesitant.

The latest dip gives us a decent yield of around 6%, and SBRA trades at a decent 12 times AFFO estimates. It’s OK, but it’s hardly bargain territory yet.

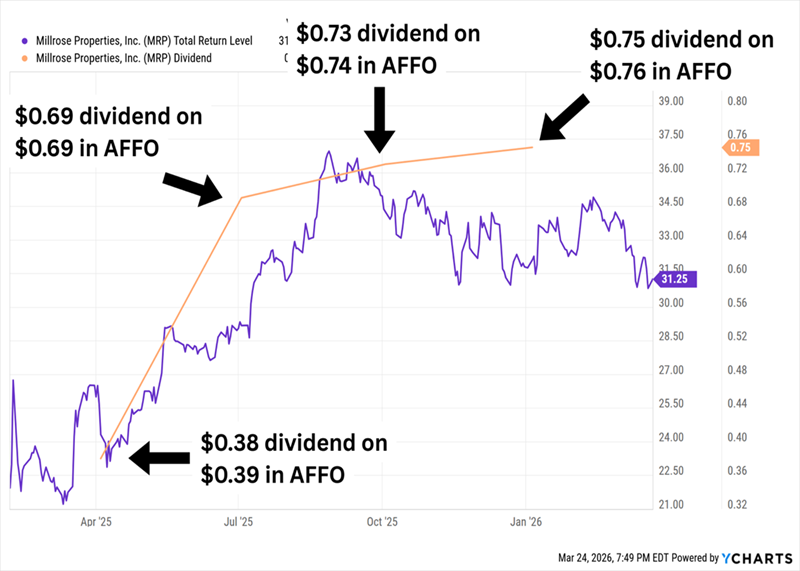

Millrose Properties (MRP)

Dividend Yield: 10.4%

I highlighted several new dividend payers last July, including Millrose Properties (MRP), one of the more unusual REITs to ever hit the market.

Millrose was spun off by homebuilder Lennar (LEN) in 2025. The company exists to buy and develop residential land, then sell finished homesites back to Lennar and other homebuilders through option contracts with predetermined costs. Lennar, for instance, will pay Millrose an 8.5% annual option fee.

It’s truly a unique structure, so I wanted to revisit it after we had more data to look at.

So far, no complaint on the bottom line—Millrose delivered higher AFFO across every quarter of 2025, and estimates are for MRP to maintain or modestly grow AFFO every quarter across the next couple of years. And the REIT has been happy to push almost all of that back to investors, raising the distribution every quarter of its existence so far.

Though I Doubt a 99% AFFO Payout Ratio Is Doable Forever

Rate uncertainty has clearly been weighing on shares of late. But what’s more interesting to me is that the administration’s executive orders to spark increased homebuilding haven’t done more to liven up shares.

I’ll also point out that MRP, at a 26% debt-to-capitalization ratio, is still plenty below its 33% max leverage target. Getting closer could spur more growth.

Meanwhile, shares trade at roughly 9 times AFFO estimates for this year. That’s definitely nice in a bubble, though MRP doesn’t have nearly enough trading history for us to know whether that valuation will be more norm or exception.

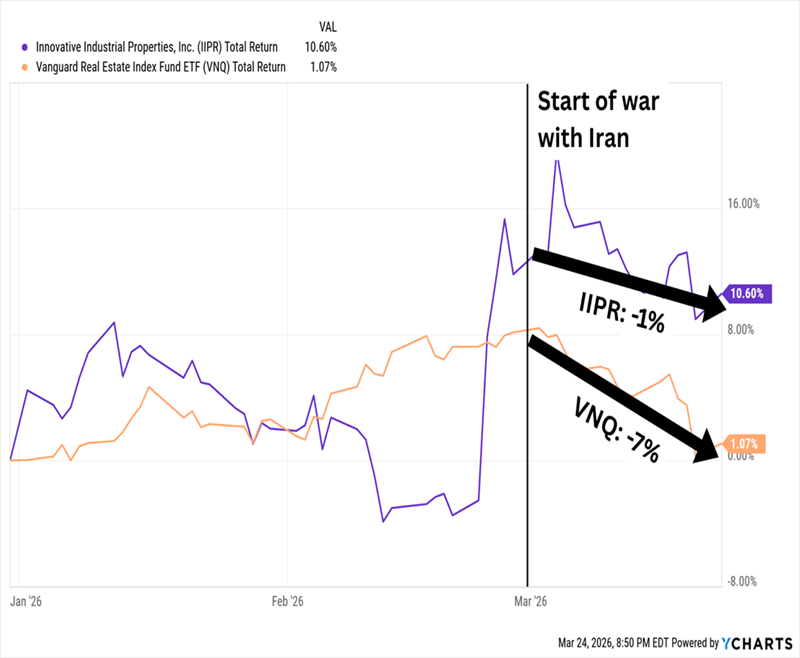

Innovative Industrial Properties (IIPR)

Dividend Yield: 14.4%

Innovative Industrial Properties (IIPR) acts as the first landlord and primary lender of choice for cannabis operators. In fact, this REIT is a capital lifeline for the industry.

IIPR buys dispensary facilities from the operators who are often short on cash and can’t finance their buildings because of the many roadblocks set up between cannabis businesses and banks. In the transaction, IIPR hands them a chunk of cash they badly need. Then it leases the facility back to the operator for 15 to 20 years.

Because traditional banks won’t touch the space, Innovative Industrial Properties negotiates incredibly favorable leases. They have long durations, built-in rent escalators and guarantees from the large corporate multi-state operator-lessees.

IIPR is essentially a “Godfather landlord” in a restricted industry. Cannabis peddlers need cash and have nobody else to turn to. So, they take the deal.

The REIT industry might have taken a hit in 2026, but we wouldn’t know it by looking at IIPR, which is one of the best-behaving stocks in the space this year.

IIPR Gained Ground After Earnings, Gave Very Little Back

It’s a promising sign of relative strength from a stock that lost its luster years ago. IIPR’s price has cratered by 80% over the past five years—a bubble that simply popped.

Still, the slow but persistent march of cannabis legalization remains a long-term tailwind. IIPR is paying investors a high 14% dividend, though coverage has tightened up of late (2025 dividends of $7.60 actually outstripped AFFO of $7.24 per share). And we’re not paying much—after commanding crazy valuations of 30 to 40 times AFFO years ago, IIPR trades at less than 8 times AFFO estimates.

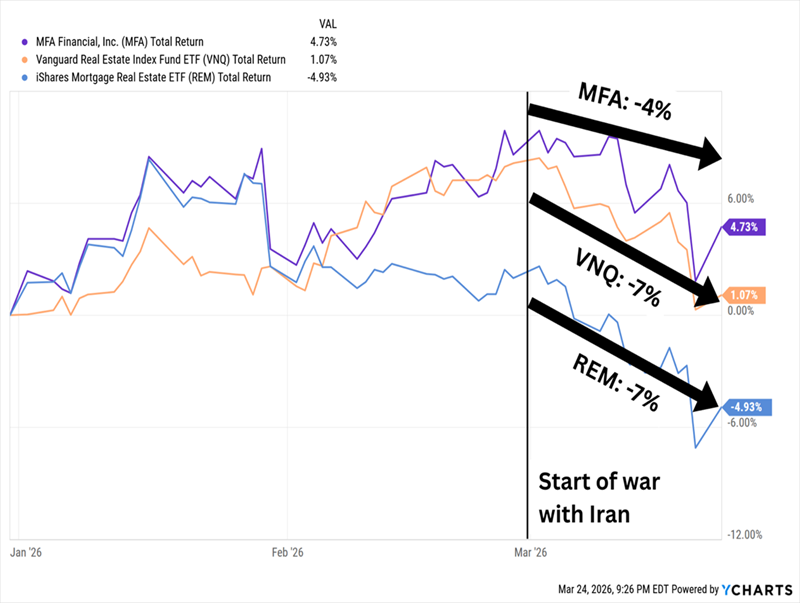

MFA Financial (MFA)

Dividend Yield: 14.6%

We can’t talk about high-yield REITs without discussing mortgage REITs (mREITs) like MFA Financial (MFA), which are the crème de la crème when it comes to eye-popping real estate payouts.

A reminder: Mortgage REITs borrow money at short-term rates to purchase mortgages (and other assets) that pay income tied to long-term rates, then profit off the difference. Their hope, then, is that short-term rates will be lower than long-term rates (which they usually are), and that short-term rates decline while long-term rates hold steady or move lower. The mREITs’ existing mortgages, which were issued when rates were higher, will yield more than newly issued ones, and thus be worth more.

Understandably, worries that the Fed might put off (or simply avoid altogether) any rate cuts in 2026, based on how the war with Iran resolves, has spooked mREITs right alongside traditional equity REITs.

MFA Is Holding Up Stronger Than Most, However

The company delivered an encouraging fourth-quarter report that provided some much-needed relief in a critical area: “distributable earnings per share” (DE), a non-GAAP measure of profitability that MFA favors.

I wrote in September that MFA was staring down the barrel of a significant dividend coverage problem—a potentially painful situation, but one that was expected to improve in 2026. And in fact, MFA finished 2025 with just $1.00 in DE versus $1.44 in dividends paid.

But its fourth quarter was much better than expected. Distributable EPS was better than expected. Economic book value per share inched higher in Q4, but management said it was up 3% so far in the current quarter. The investment portfolio improved by nearly 10%.

There’s still risk—MFA still needs to execute to get out of the woods, and a stalled Fed could hamper that—but this mREIT likely is still in a better position than it was half a year ago.

A Fully Paid Retirement for Just $600,000?

A 15% yield would do wonders for any retirement portfolio.

However, if we own 15% yielders that force us to religiously watch every earnings report for fear of a dividend cut, we might not make it to retirement.

If we’re going to retire on dividends alone, we don’t just need high yields—we need no-doubt payers that aren’t an earnings disappointment away from ruining our income stream.

And those are the kinds of dividends I prioritize in my “9% Monthly Payer Portfolio.”

These generous stocks and funds pay up to 14.9% and average more than 9% across the board. That’s enough to live on dividends alone—without ever needing to sell a single share to generate cash.

The math on this portfolio is easy to follow:

- A $600,000 nest egg could earn $54,000—in many places in the U.S., that’s enough for a fully paid retirement without even factoring in Social Security!

- And if you have managed to stow away a cool million bucks to work with, the 9% Monthly Payer Portfolio would pay you a downright lush $90,000 in dividend income every year.

Better still? You’d be cashing dividend checks not annually, not quarterly, but each and every month. That means no “lumpy” payouts. No complex dividend calendars. No dumping money into certain stocks because you’re getting underpaid every third month.

Just paydays as smooth as when you were collecting a paycheck!

Don’t miss out on these terrific income plays while you can still get in at bargain prices. Click here for all the details, and turn your portfolio into a monthly dividend machine!