Using vanilla websites for your dividend research? Be careful.

Many of these mainstream sites miss the most important payment of the year for “special” dividend companies!

This oversight could have us overlooking thousands of dollars in potential yearly income. And yields up to 14.6%!

Would you believe what this 14.6% payer is listed at on these lame sites? 0.2%. Zero-point-two percent.

Yup. Which is why we contrarians do our research with a focus on special dividends.

Specials uncommon enough that many investors don’t know much (if anything) about them. In short, they’re one-time cash payouts, usually the result of a massive capital boost—say, selling off a piece of the company or delivering blowout annual profits.

At least, usually that’s the case.

Some stocks pay out so-called “supplemental” dividends that they pair with regular distributions. Let’s say a company pays out 50 cents per share quarterly, but at the end of the year it pays out half of its free cash flow as a supplemental dividend. That might be an extra $1 in one year, $3 in another.

In some cases, it’s a tidy little “top-up” that makes a nice dividend a little nicer. But sometimes, these special dividends take a decent to even modest yield and turn it into an eye-popping payout in the high-single or even double digits.

Just check out this seven-pack of “special” payers. While financial dividend sites would tell us they’re paying a collective 6% on average, in reality, this mini-portfolio’s true average yield is a mouth-watering 10%.

Retailers

Let’s start with an unlikely pair—two mall names most income investors wouldn’t touch with a ten-foot pole.

I wouldn’t want to share a foxhole with Dillard’s (DDS, 0.2% headline yield) and The Buckle (BKE, 2.9% headline yield). They’re both mall plays—the former is one of the few remaining department-store chains, while the latter is a fashion retailer, which is as fickle as a business gets. Economic shivers give both the fits, and a pressured consumer has both well in the red so far this year.

But to their credit, they’ve been two of the better mall names in recent years, and their practice of topping up modest regular dividends with large specials as profits allow is a great model for their cyclical businesses.

They’re also both sterling examples of just how much yield is “hidden” from us. Just look at what a top data provider lists for each, and what their actual yields are.

Dillard’s

That microscopic payday only factors in Dillard’s 30-cent quarterly dividend. But DDS has been paying enormous special dividends for years—$15 per share in 2021 and 2022, $20 in 2023, $25 in 2024, and $30 in 2025. Including that last special, Dillard’s true yield is 5.9%.

The Buckle

The Buckle’s regular payout is at least respectable at just shy of 3%. But that’s a far cry from the real number, because like Dillard’s, BKE has been handing out large specials to start each of the past few years. Add 2026’s $3-per-share special on top of its 35-cent quarterlies, and Buckle’s true yield is 9.1%.

Fair warning: Management isn’t promising us those fat specials. But they’ve clearly signaled they’re willing to share the wealth when times are good. And that’s a nice potential bonus for anyone who was already planning on taking a flyer in the retail space.

Insurers

Insurers are basically in the business of pricing chaos, so it’s almost strange that so many of their dividends are the same year in and year out. Regular-and-special systems make a lot more sense given their cyclical earnings.

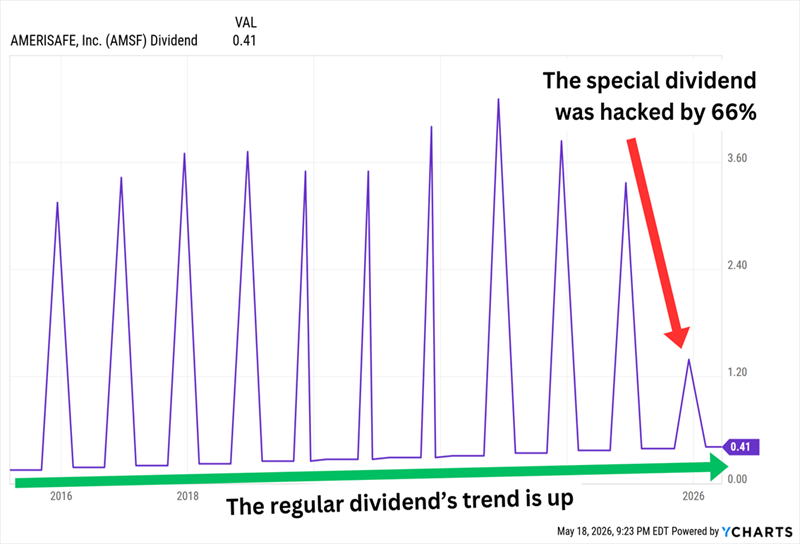

Amerisafe (AMSF, 5.2% headline yield)—a workers’ compensation insurer with a focus on small to midsized employers in “high-hazard” industries such as construction, trucking and agriculture—is something of an outlier in this area in that its bottom line is much more stable than the average insurer.

But that doesn’t mean its profit situation is necessarily good.

I mentioned in 2025 that anyone interested in AMSF’s big special dividends should keep a close eye on Amerisafe’s bottom line. While Amerisafe has been able to grow its top line consistently, the company’s profits have declined in each of the past two years. Wall Street analysts covering the stock believe that’ll happen again in 2026, and that 2027 earnings will merely remain level. One of the biggest culprits has been slowing job growth, which has become downright anemic in the past year or so.

This has really cramped Amerisafe’s special distribution. AMSF has been writing regular dividend checks since 2013 and specials since 2014—and 2025’s extra payout, while still enough to boost the true yield to 8.4%, was the smallest in a decade.

The Only Good News? The Modest Regular Dividend Continues to Grow

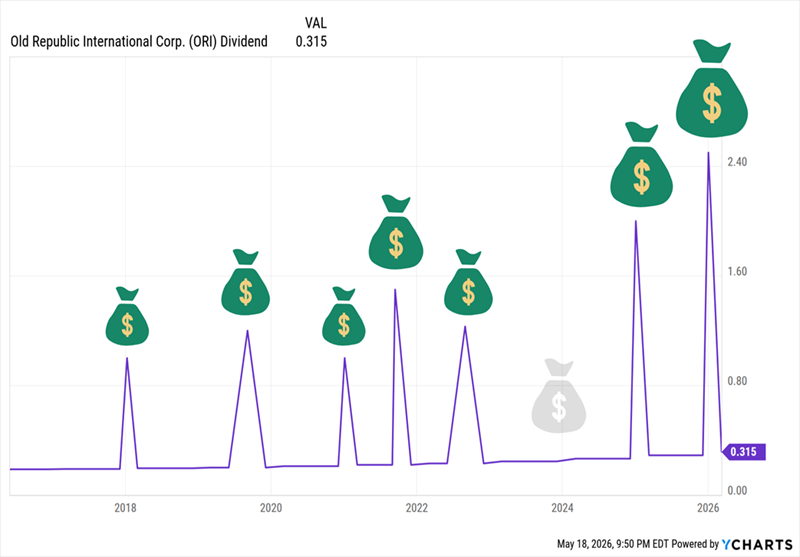

Old Republic International (ORI, 3.1% headline yield) is a specialty and title insurance company that operates in the U.S. and Canada. The title segment of the business provides protection against losses over real estate disputes, and provides escrow closing and construction disbursement services. The specialty insurance segment is much wider, including commercial auto, commercial property, travel accident, aviation, environmental, cyber, and numerous other coverages, offered up to a variety of industries, including transportation, healthcare, education, retail, energy and more. It also plays in Amerisafe’s workers’ comp sandbox.

ORI’s top line has generally trended higher for decades, but its bottom line is the erratic mess we’d expect out of an insurer—even one as well-diversified as Old Republic.

So we have to tip our hats to management, which has made ORI one of the most prolific dividend growers on the market despite this uncertain profit footing. Old Republic boasts a full 45 years of consecutive annual distribution hikes. Management is quick to throw extra dividends at shareholders when profits allow, too—and those special dividends can be massive. A $2.50-per-share special on top of its 31-cent regulars comes out to a true yield of 9.4%.

But because ORI’s business is more unpredictable than the likes of an Amerisafe, the specials are spottier.

Timing Is All Over the Place, And ORI Skipped a Special in 2023

Business Development Companies (BDCs)

In general, “normal” stocks that pay regular dividends tend to offer up decent-but-not-great regular dividends, then blow us away with fat specials when they can.

Business development companies (BDCs), which provide financing to smaller firms, take a different tack. That is, they pay regular dividends that in and of themselves put almost every other sector to shame—and when net investment income is sufficient enough, they’ll sweeten them even further with top-up specials.

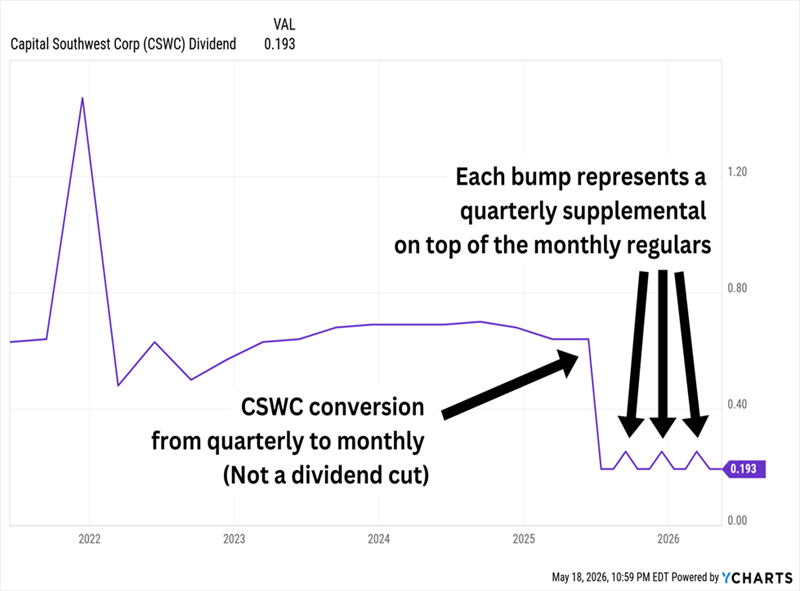

Take Capital Southwest Corp. (CSWC, 10.0% headline yield) for instance.

CSWC provides capital to lower middle market firms with EBITDA (earnings before interest, taxes, depreciation and amortization) of between $3 million and $25 million. The vast majority (90%) of its deals are first-lien loans, most of the rest (9%) is equity, though it has sprinklings of second-lien loans and subordinated debt. It has a diversified portfolio of 131 companies representing a couple dozen industries; healthcare services, consumer services, media/marketing and consumer products are the best-represented right now.

The BDC industry is a difficult one where losers greatly outnumber winners. But I’ve said before that CSWC is a standout—it has moderate leverage and a well-covered dividend. Meanwhile, special dividends add a full percentage point, for a true yield of 11%.

Better still? Capital Southwest recently converted its payout system from quarterly to monthly distributions.

It admittedly makes for a bizarre chart.

But the Recent Dividend Cadence Is Pretty Steady

The only glaring weakness here is a premium valuation to match CSWC’s premium performance. Right now, Capital Southwest’s shares trade at a whopping 40% above the BDC’s net asset value (NAV).

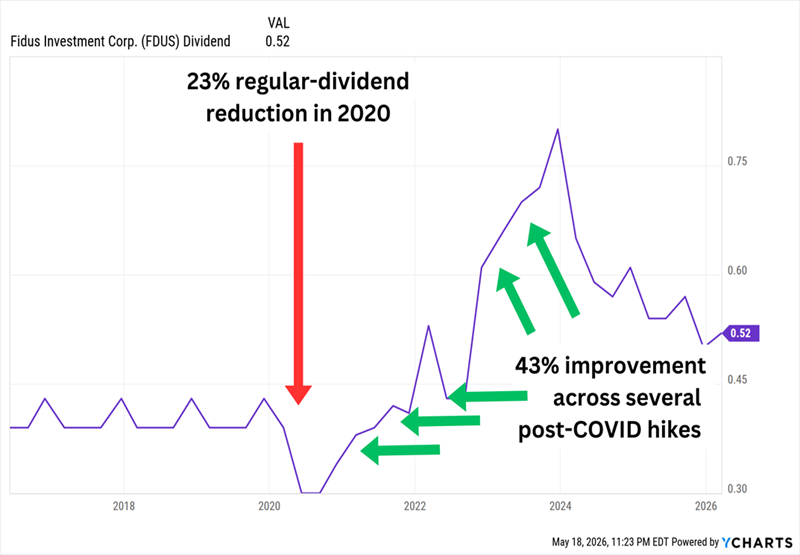

Fidus Investment Corp. (FDUS, 9.2% headline yield) invests in a wide range of lower middle market companies, preferring firms with proven business models and strong free cash flows. Target companies typically have annual EBITDA of $5 million to $30 million. Its deal mix is more diversified than CSWC, with about 80% in first-lien debt, 7% in each of subordinated debt and equity, and the remaining 6% in second-lien loans.

Fidus has 97 portfolio companies at the moment. And while they’re spread across a couple dozen industries, FDUS leans heavily into information technology service firms, which make up more than a third of the portfolio at cost. However, while tech exposure has been an anvil tied to the ankles of numerous other BDCs, AI seemingly hasn’t been weighing on its holdings—Fidus has outperformed the sector by about 15 percentage points over the past year.

FDUS does have a dividend strike against it in that it cut its regular payout during the pandemic. But it quickly worked to restore the distribution to—and eventually past—pre-COVID heights. The pandemic also marked a shift from annual top-ups to quarterly top-ups.

Fidus’ Quarterly Specials Vary Widely

The specials over the past 12 months take Fidus from a headline yield of 9.2% to a true yield of 11.8%.

Unlike with CSWC, we’re not being forced to overpay for FDUS’ relative business strength. Shares currently trade at a modest 5% discount to NAV.

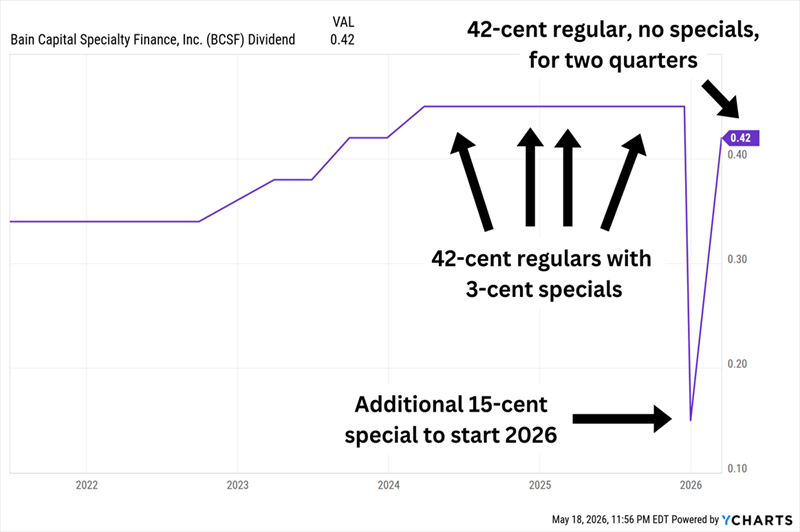

Bain Capital Specialty Finance (BCSF, 12.8% headline yield) is one of the more geographically diversified BDCs, providing a variety of financing solutions to over 200 companies not just in North America, but also Europe and even Australia. It primarily deals in first-lien debt, which makes up a little more than 80% of its deal mix. Equity and preferred equity each make up about 7% apiece, but it also works with subordinated debt (3%) and second-lien loans (1%).

Bain Capital has delivered mixed results since its initial public offering (IPO) in 2018. It had caught its stride in recent years, but took a step back in 2025 before getting back up to speed this year. Non-accruals (loans not accruing interest because they’re past due, usually by 90 days or more) of just 1.4% are well below the BDC average of nearly 4%. Software makes up 13% of the portfolio, but CEO Michael Ewald said in the Q1 conference call that a recent review showed “the majority of our software investments carry a relatively low risk of AI-driven disruption.”

BCSF is also easily the cheapest of the three BDCs here, trading at a steep discount to NAV of 22%.

But There Are Signs of Trouble in the Dividend

Bain Capital pre-announced 3-cent specials across all of 2025, then ended the year by announcing an additional 15-cent special to be paid in early 2026. After that, however, it has announced two quarterly dividends with no specials.

Once we factor in specials paid over the past 12 months, BCSF’s true yield is 14.6%. But it’s possible that number is overshooting its future yield—and not only because we can’t count on specials. The pros are projecting that Bain Capital’s earnings will be barely enough to cover the dividend this year, and will fall well short of the payout in 2027.

My Favorite 11% Dividend Is a Cure for 2026’s Chaos

We’re drawn to double-digit dividends because they give us a way out.

A way out of panicking over massive daily swings. A way out of scanning headlines for the latest tariffs and policy changes. A way out of constantly wondering whether AI is going to obliterate our portfolios.

So if we’re going to take a swing on a double-digit yield, we want dividends we can count on—where special dividends are merely the cherry on top.

That’s exactly what we’re getting from one of my favorite home-run dividends: a heavily diversified, brilliantly built bond portfolio that yields 11% but is also set up for stock-like gains.

This fund checks off just about every income box I can think of:

- It pays a whopping 11% in annual income!

- It pays its dividends each and every month!

- It has increased its dividend over time!

- And hey—it has paid out multiple special dividends!

The manager’s credentials? About as good as it gets. Morningstar previously named him Fixed Income Manager of the Year. And he’s literally a hall-of-famer, honored by the Fixed Income Analysts Society Hall of Fame.

But the window on this home-run dividend is closing fast! Premiums on funds like these tend to rise as volatility ticks higher and as investors rotate out of growth stocks and into reliable sources of income like this. I don’t want you to miss your chance. Click here and I’ll introduce you to this incredible 11% payer and give you a free Special Report revealing its name and ticker.