The stunning thing about this year’s stock-market rally is that much of it has come in just the last couple of months.

That’s especially the case in tech: The NASDAQ has returned 33% just since March 30, as of this writing. The tech benchmark Vanguard Information Technology Index Fund (VGT) has done even better, spiking 48%.

That surge has, naturally, raised some concern. After all, isn’t the job market slowing? And aren’t inflation and interest rates staying relatively high?

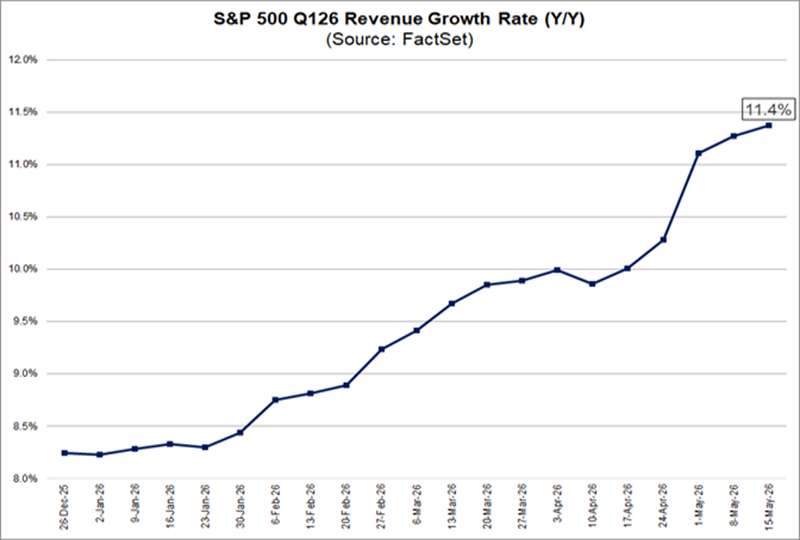

Those worries are valid, of course, but the fact is that over time, stocks tend to track back to corporate earnings and sales growth, and both are surging. In Q1, for example, revenues popped 11.4% year-over-year.

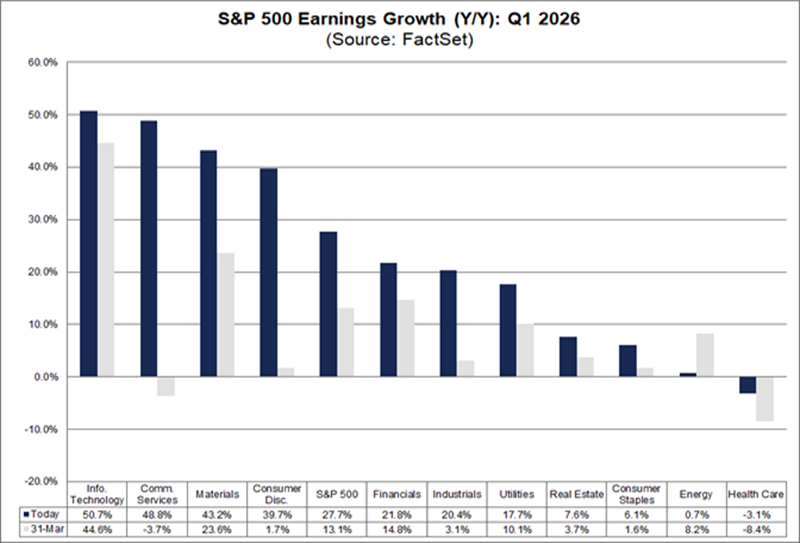

Meantime, earnings gained 27% for the S&P 500 as a whole, with the tech, communication-services, industrial and consumer-discretionary sectors all ahead of that baseline.

Those are all positives, with growth in consumer-discretionary, in particular, suggesting consumers are still spending at a healthy clip. Still-strong gains in financials and industrials support that spending, too.

The takeaway from all of this is that the stock market’s gains are, in fact, reasonable, even if the speed with which they’ve arrived is a bit startling.

But that, of course, does not mean every stock is a winner. Nor does it mean every closed-end fund (CEF) is. (These 8%+ yielding vehicles are my beat at my CEF Insider service.)

Let’s zero in on two CEFs—one I see as an overlooked bargain and another whose off-the-charts current yield (24.1%!) represents a risk, not a windfall.

This 24.1% Yield Is a Warning Sign

I covered a CEF called Oxford Lane Capital Corp. (OXLC) in a May 21 article. I bring it up again because in a rally this strong, speculative funds like this can be alluring.

My May 21 article gives you my full analysis of OXLC; here I’m going to touch on the major reasons why I see the fund as a sell before we move on to that other fund I recommend buying instead.

OXLC specializes in CLOs, or collateralized loan obligations. These are structured bundles of loans made to below-investment-grade companies. The issuer then sells fractions of the CLO to investors—or to funds like OXLC.

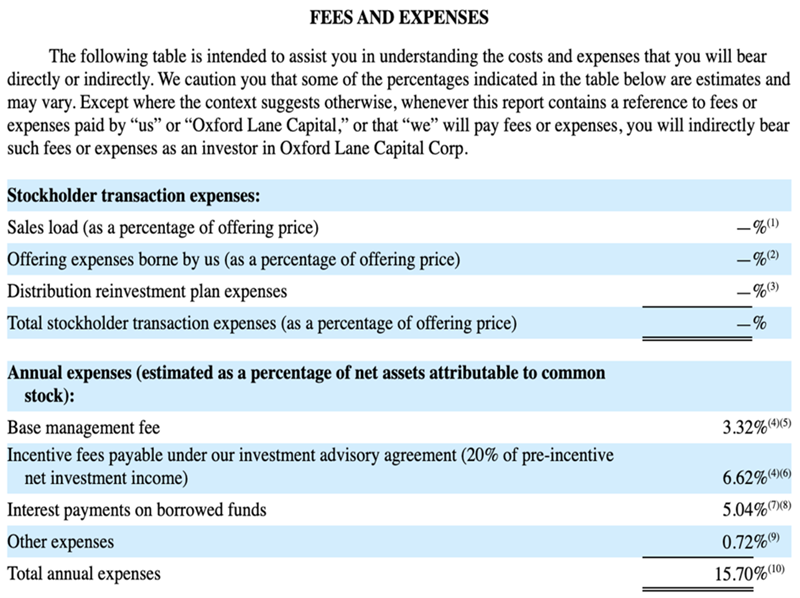

Setting aside the risks inherent in CLOs, I want to zero in on two bigger risks: OXLC’s fees and the fallout from a recent dividend cut. Let’s start with fees.

Source: OXLC SEC filing for year ended March 31, 2026

As you can see in the SEC filing above, including interest paid (OXLC employs leverage on around 42% of its portfolio, according to CEF Connect), fees amount to a whopping 15.7% of assets.

Those fees, in turn, come out of the fund’s net asset value (NAV, or the value of its underlying portfolio). That weighs on its long-term price performance. Beyond that, the fund’s dividend has been cut sharply, and is now down some 41% in the last five years. The share price has fallen sharply in that time, as well.

24% Current Yield Masks Share-Price Drop, Dividend Cuts

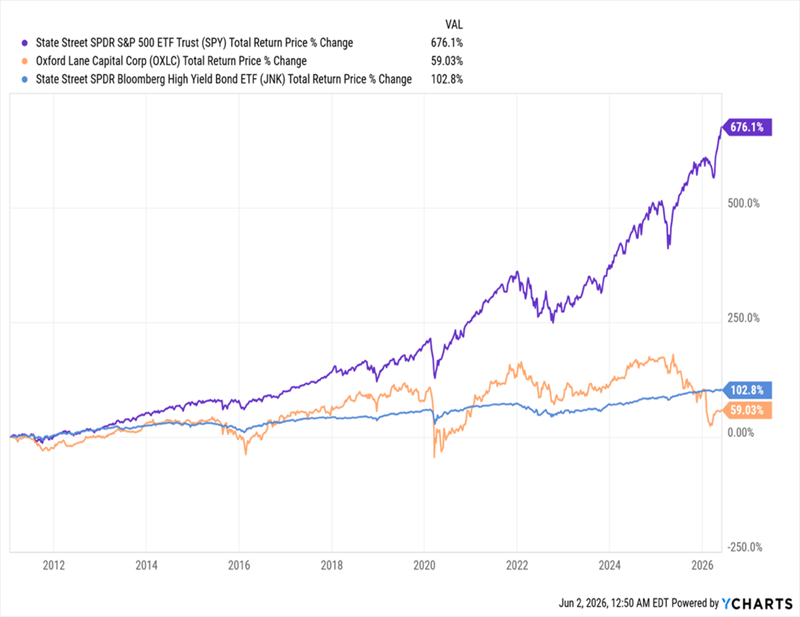

Now let’s look at the fund’s performance from inception in 2011.

A Long-Term Underperformer

To its credit, OXLC (in orange above) hasn’t lost money, but its performance is far behind the S&P 500 (in purple) and the benchmark ETF for high-yield bonds (in blue). That’s another reason why this fund remains a sell.

Now let’s move on to that buy I mentioned earlier, it’s the opposite of OXLC in almost every way.

This 8.3% Dividend Profits From AI’s Growth (and Much More)

One of my favorite equity CEFs is the Liberty All-Star Growth Fund (ASG). This fund, a CEF Insider holding, yields 8.3% as I write this.

ASG leans toward tech, but it also gives us access to stocks that haven’t been as caught up in the market rally, which makes ASG a strong diversification tool.

Familiar big-cap techs like NVIDIA (NVDA), Apple (AAPL), Microsoft (MSFT) and Amazon.com (AMZN) occupy the top four spots in the portfolio.

From there, things get a bit more interesting as other companies fill out the balance, like Monolithic Power Systems (MPWR), which makes integrated circuits used in the data-center buildout. Non-tech firms, like property manager FirstService (FSV) and Pennsylvania-based Ollie’s Bargain Outlet Holdings (OLLI), also appear.

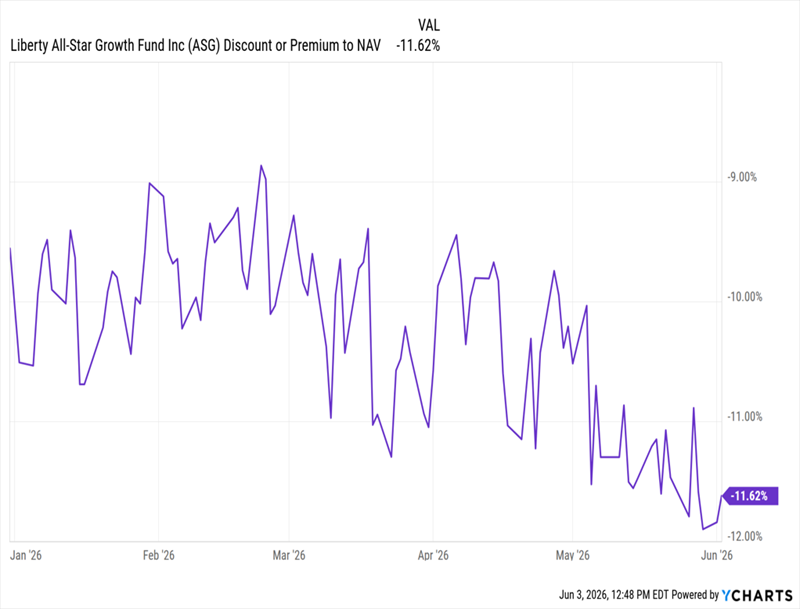

The fund is the definition of a steady grower, tacking on a 34% total return for us in CEF Insider since we bought it in May 2023, as of this writing. But I see that as just the start: Despite its diversified, growth-oriented portfolio, ASG’s discount to NAV has actually widened this year: This fund is now on the table for around 12% below its portfolio value:

ASG Gets Cheaper—as Its Main Holdings Rally

The result is that we can buy ASG’s diverse portfolio for around 88 cents on the dollar.

Finally, we like ASG for its dividend policy, as it ties its payout to the performance of its portfolio. So the bigger the portfolio’s gains, the faster the payout grows. That’s a nice setup in a market where corporate earnings, and sales, are marching higher.

4 More CEFs With Big Dividends (9.9% on Average) and Big Discounts, Too

CEFs are the perfect wealth-building tools in this soaring market because, thanks to their overlooked nature, there’s always a bargain somewhere in the space.

ASG is a prime example of that. And my team and I have identified 4 more high-yield CEFs we see as “must-buys” now.

All four of these funds have portfolios that are surging, yet discounts that are totally out of step with that performance.

The best part? These 4 overlooked gems yield 9.9% on average, with three of them paying monthly.

The time to buy them is now, before their discounts snap shut and their prices race away from us. Click here and I’ll introduce you to these 4 stout income plays and give you a free Special Report containing their names, tickers and my complete analysis of their portfolios.