There’s a clear “disconnect” happening in the US economy right now. And most investors are on the wrong side of it.

Funny thing about it is, it’s pretty obvious. We hear about both sides of it in the news daily, but few people truly see it for what it is. And the 10.5% dividend we’re going to discuss today is the perfect play on this misconception.

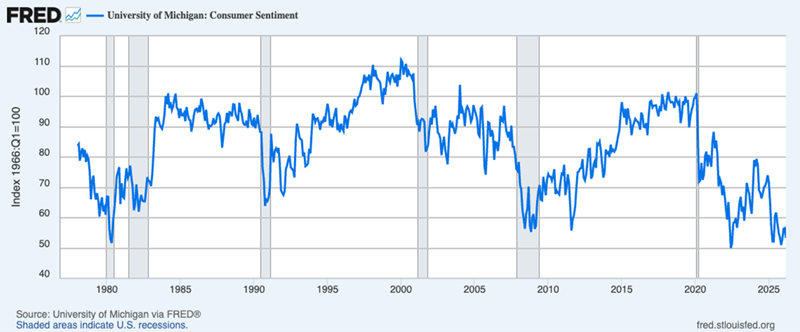

The first part of our opportunity? Consumer sentiment, which I’m sure you’ve heard is in the tank:

Here’s the University of Michigan consumer-sentiment survey over the last 50 years. At the right side of this chart we see that the current level is the lowest it’s been in all of that time.

In other words, Americans today feel worse about the economy than they’ve felt in a couple of generations, more or less. Which is where the other side of our disconnect comes in: In the last year alone, the S&P 500 has returned 25%.

That, of course, is good news for those of us who own stocks, but keep in mind that stocks do return around 10% per year including dividends, on average, so this strong gain clearly shows the value of buying for the long term and being patient.

But the disconnect between stocks’ brilliant performance and lousy sentiment raises another question: Are we headed for a correction?

That’s not what we see in the data. Not even close.

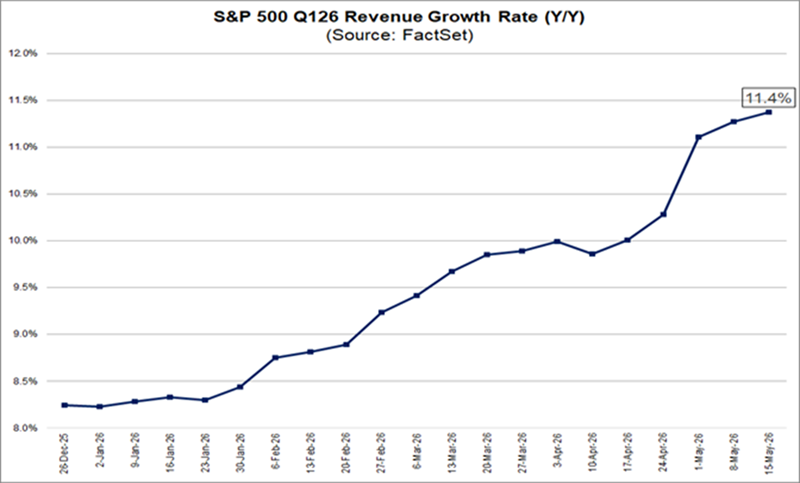

As you can see above, S&P 500 firms booked year-over-year gains north of 11% in Q1. That’s the highest since 2022, and it’s historically very high indeed.

Note also that sales growth has been accelerating for years. That’s in part due to businesses benefitting from the AI boom.

Whatever feelings we may each have about AI, there’s no denying the fact that the AI buildout is benefitting utilities, energy, infrastructure, construction, transport, retail and other industries. That’s showing up in US companies’ bottom lines—even those of some of the riskiest firms out there.

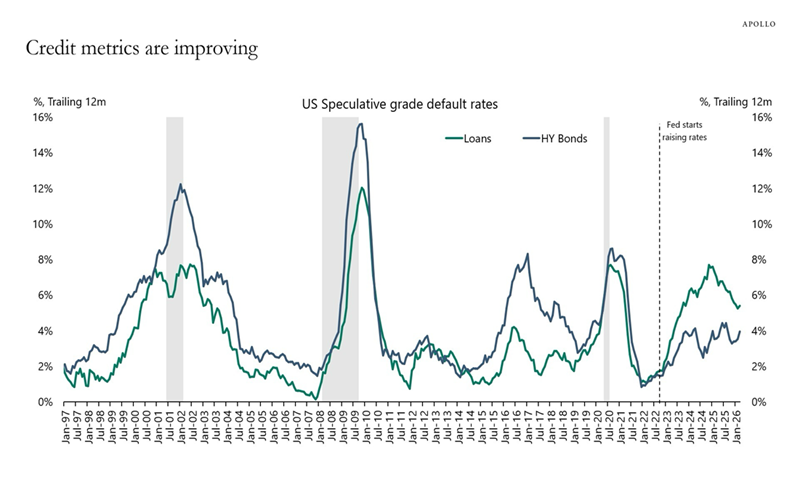

In the speculative credit market, we’re seeing default rates fall significantly. Most crucially, they’re falling fastest in the loan market, which was behind the private-credit panic late last year and earlier this year.

The bottom line is that US companies are, on the whole, doing well. But where does that leave everyday Americans?

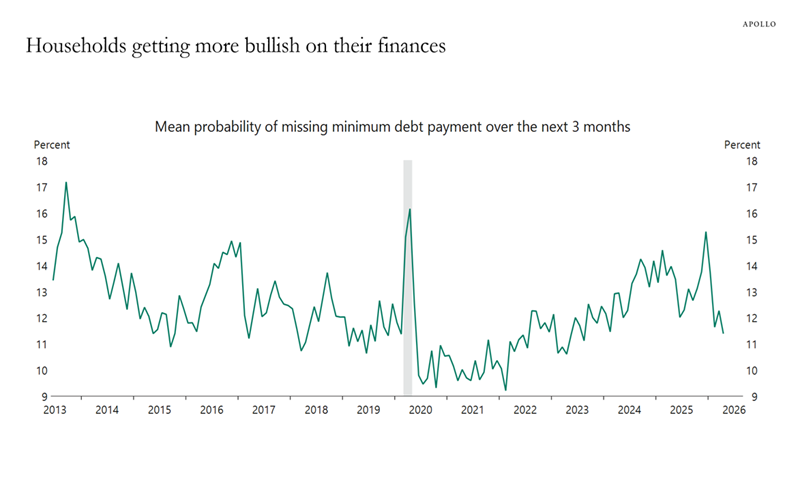

Despite their dour mood, American families have largely been financially healthy throughout this decade. As we can see above, they’re less likely to default on their debts than they were in the 2010s.

There was a trend of rising defaults earlier this decade, as pandemic-relief efforts from the Fed and US Treasury faded. But there’s been a sharp drop in defaults since early 2025. This shows that Americans’ financial health is improving. Part of that may be due to increased opportunities due to the aforementioned AI buildout.

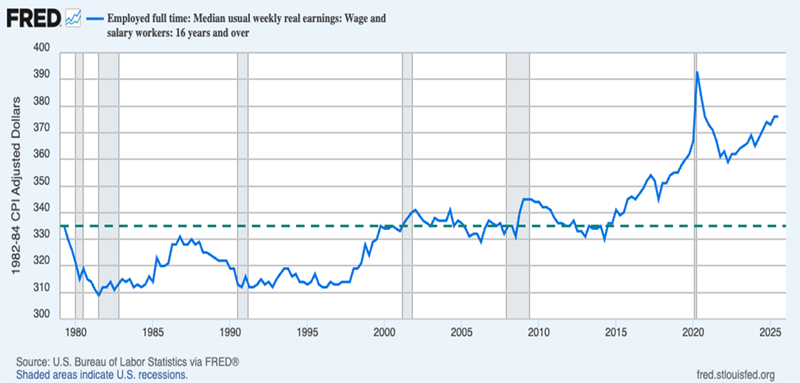

Finally, the chart above shows inflation-adjusted earnings for workers. Note how from 1980 to 2015, wages didn’t really grow at all. Then they began to gain ground in the late 2010s and have continued to rise since.

Funny thing is, Americans generally started making more money in the late 2010s, just when sentiment began to slide. That trend continues to this day, setting up an odd dynamic: People are generally getting richer—and they’re not happy about it!

It’s an odd situation, to be sure, and it sets the stage for euphoric jumps and steep drops in stocks as rising earnings and lousy sentiment battle it out. We saw the dips around a year ago, when the Liberation Day tariffs were announced, and again this year, due to the Iran conflict (and if you go further back, the deep selloff in 2022, on inflation concerns).

All of those moments were buying opportunities, and I firmly believe that will be true of any future pullbacks, too.

This 10.5% Dividend Is a Smart Play on the Earnings/Sentiment Mash-Up

This is where a closed-end fund (CEF) called the Liberty All-Star Equity Fund (USA) comes in. It’s a 10.5%-yielder that holds large cap S&P 500 stocks.

Its top holdings are NVIDIA (NVDA), Microsoft (MSFT), Alphabet (GOOGL), Amazon.com (AMZN), Capital One Financial (COF), Meta Platforms (META), Visa (V) and Wells Fargo & Co. (WFC).

And because USA is a CEF, we can get access to its holdings at a discount to net asset value (NAV, or the value of the fund’s underlying portfolio). That’s a deal that just doesn’t exist with ETFs.

It’s particularly timely in USA’s case because the fund’s already-steep discount means we don’t have to wait to buy the dip here: USA already trades at an 11.3% discount, well below the 7.5% it’s averaged in the last year and far below the 0.7% it’s averaged over the last five years.

Deals like this are difficult to track down in a rising market like this one.

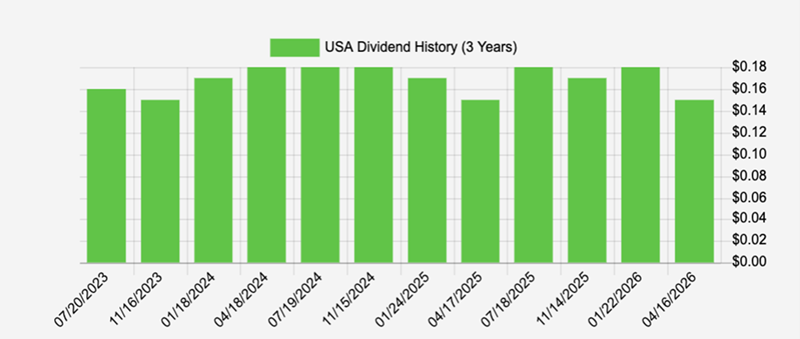

But the most exciting part is that 10.5% dividend, which USA generates by taking the returns on its holdings and “converting” them into an income stream for us. It manages that by linking the dividend to its NAV and committing to paying out roughly 10% of NAV as dividends every year.

That does mean the quarterly payout floats a bit, but we’re okay with that, since the result has been a pretty consistent dividend over the last three years:

Source: Income Calendar

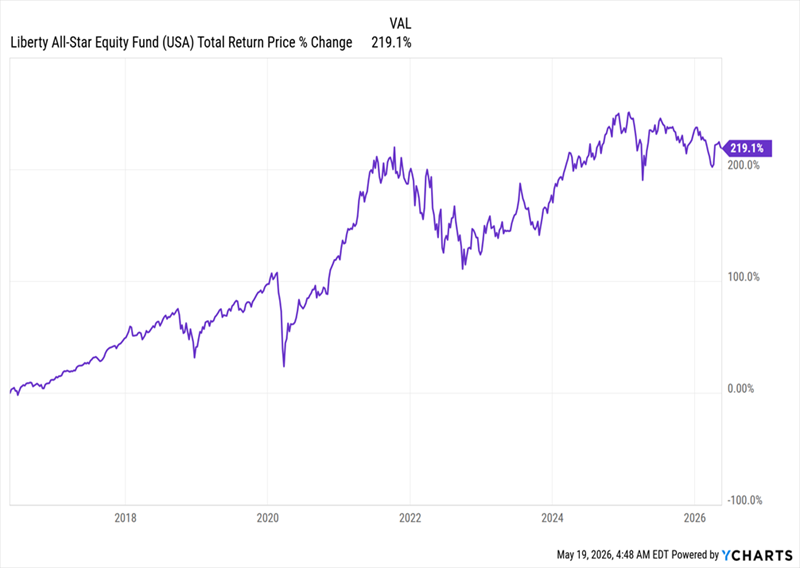

And then there is the fund’s overall performance, which has been strong:

USA Delivers a Steady Long-Term Return

USA has delivered a 12.3% annualized total return over the last decade, and it’s done so consistently, thanks to that strong portfolio.

And since the fund gives out most of its price gains as dividends, you can reinvest in USA and grow your income (and portfolio value) further. Or you could withdraw your dividends and use them to finance your lifestyle, as many retirees do.

The choice is yours, and strong CEFs with proven track records, like USA, make that flexibility possible.

Beyond USA: 5 Funds Paying Reliable Dividends Every Month (With a 9.3% Yield)

ASG is a strong fund (especially at its current discount), but for a truly reliable income plan, we need to temper it with funds that pay steady, reliable and ideally monthly dividends.

That way we always know, down to the penny, what we’re getting in dividends every month.

To that end, I’ve hand-picked my 5 top monthly paying CEFs and placed them in a “mini-portfolio” all their own. I call it the “60-Paycheck Dividend Plan” because with these 5 funds you get 5 dividend checks a month, or 60 on the year.

They’re perfect for paying your bills and smoothing out your quarterly payers, or funds like USA, whose payouts can float a bit.

Kickstarting this silky-smooth income stream couldn’t be simpler. Simply click here and I’ll spell it all out for you in detail and give you a free Special Report revealing these 5 monthly payers’ names and tickers.

With that in hand, you’ll be set to collect the first of your 60 yearly “dividend paychecks” in short order.