Dividend raises mean something right now.

These are companies saying that they are going to make more money in the year ahead in the face of everything that is happening around the globe.

Let’s review six upcoming dividend raises—stocks paying up to 7.2% today!—dished by companies with the audacity to continue collecting cash regardless of what the world has in store for them.

“Frontrunning” these announcements, by the way, can be an excellent way to generate returns. As these dividends pop they will act like “magnets” pulling these associated stock prices higher. Post-raise we’ll often see that the current yields are unchanged. Why? Because the stock already rallied in tandem with the payout hike.

Nasdaq (NDAQ)

Dividend Yield: 1.3%

2025 Increase: 12.5%

Projected Q2 Distribution Announcement: Late April

Nasdaq (NDAQ) is the eponymous company behind the Nasdaq Stock Market exchange and the Nasdaq Composite index—and quite a bit more that most investors might not know. It also operates the Philadelphia and Boston stock exchanges, as well as seven European stock exchanges. And it’s the name behind Verafin (financial crime management solutions), AxiomSL (risk data management and regulatory reporting), and Calypso (capital markets and treasury solutions).

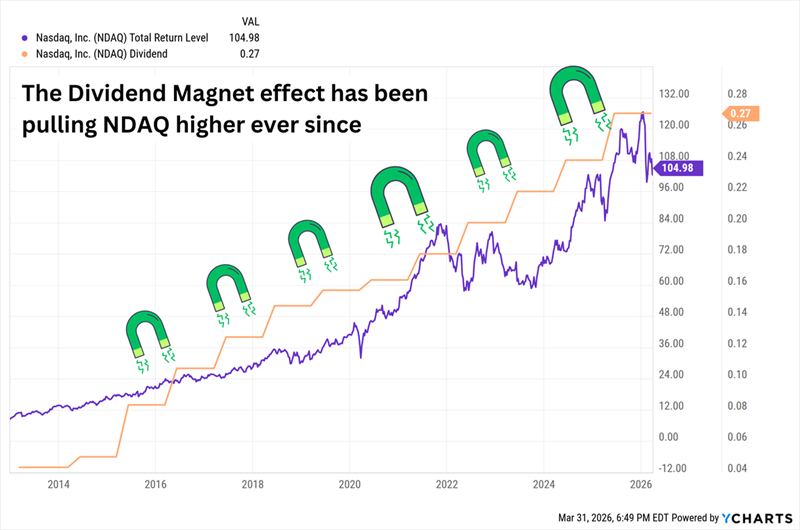

Despite being all of the above and more, NDAQ’s performance over the very long term has looked mighty similar to its tech-heavy market index—which is, to say, outstanding. That success finally translated into a dividend starting in 2012.

And NDAQ Has Increased That Payout Every Year Since 2014

That dividend growth has largely been brisk, and included a 12.5% boost a year ago, to 27 cents per share quarterly. That amounts to less than 30% of Nasdaq’s projected profits for this year—plenty of runway to keep the pedal down should it raise again, which based on past announcements would happen sometime in late April.

The 1.3% yield isn’t much to look at, but that’s largely because of the aforementioned stock success. But it’s relatively elevated currently thanks to a double-digit decline in 2026, courtesy of the AI-linked clobbering of software stocks this year. NDAQ might have been thrown out with the bathwater. The Nasdaq is working on launching 23/5 stock trading, tokenizing markets, adding daily expirations for single-stock options, and more—and is looking to incorporate artificial intelligence into its own solutions. All of this led the company to raise its medium-term Solutions guidance from 8%-11% average annual growth to 9%-12% growth while keeping its expense forecast level.

Synchrony Financial (SYF)

Dividend Yield: 1.8%

2025 Increase: 20.0%

Projected Q2 Distribution Announcement: Late April

Synchrony Financial (SYF) is a credit company that’s happy to work in the limelight. Once a subsidiary of General Electric (GE)’s GE Capital until its 2014 spinoff and initial public offering (IPO), Synchrony provides credit cards, commercial credit products and consumer installment loans.

It does virtually all of this under other brands: Perhaps most notable is the CareCredit health and wellness credit cards, but it also provides payments and financing solutions for companies including Walgreens (WBA), American Eagle (AEO), Dick’s Sporting Goods (DKS), Polaris (PII), and more.

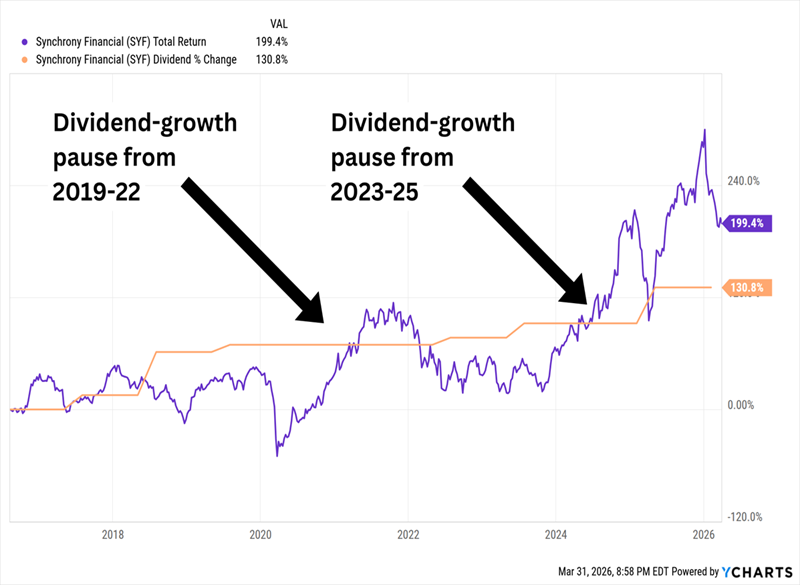

Synchrony’s dividend has more than doubled over the past decade, but SYF is hardly a habitual dividend raiser. In fact, it failed to increase its distribution as recently as 2024; when it did in 2023, it did so in July. But its 2025 hike came in late April, so that’s where I’ll be looking for another potential hike.

SYF’s dividend history doesn’t really turn up any patterns, but there’s still reason to believe that any raise could be substantial.

Synchrony Is Happy to Reward Shareholders—But to the Beat of Its Own Drum

For one, Synchrony is paying out just 13% of estimated 2026 earnings as cash distributions. SYF’s profits can be highly variable, so management is likely to keep a conservative payout ratio—but even then, the company has plenty more room to expand that dividend.

Also, most of Synchrony’s largest hikes have occurred in and around its most profitable years, and SYF is coming off a strong 2025 that admittedly saw modest growth but still produced elevated top and bottom lines near the top of its long-term range.

Victory Capital Holdings (VCTR)

Dividend Yield: 3.0%

2025 Increase: 4.2%

Projected Q2 Distribution Announcement: Early May

Victory Capital Holdings (VCTR) is an investment manager that provides specialized investment strategies to institutions, retirement platforms and individual investors.

Specifically, it offers mutual funds, ETFs, separately managed accounts, alternative investments, private funds, brokerage services and more. And it does so through a variety of brands it has picked up through its acquisitive history, including Integrity Asset Management (acquired through the purchase of Munder Capital Management) and WestEnd Advisors, among others. Perhaps most notable, though, is Victory Income Investors—the rebrand of USAA Asset Management Company, which it acquired in 2019.

VCTR was on the precipice of another blockbuster this year, making an $8.6 billion bid to acquire Janus Henderson in February, then sweetening the deal in March. But it ultimately withdrew, ceding Janus to a bid from Trian Fund Management and General Catalyst.

That’s not to say Victory is going to take all the cash earmarked for that acquisition and push it into the dividend—VCTR is a habitual buyer. But it is due.

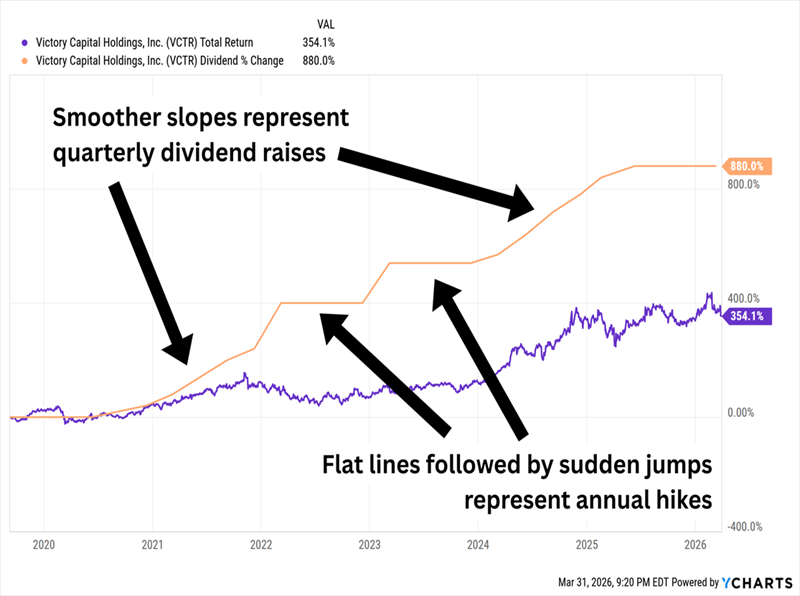

I last looked at Victory Capital a year ago, and at the time, it was still in the midst of a yearslong streak of consecutive quarterly dividend hikes. It kept on that schedule for one more quarter … but the dividend has remained flat since then. That said, we’re nearing the one-year mark, and VCTR has never gone longer than a year without raising the payout.

In Fact, VCTR Has Had Multiple Periods of Quarterly Dividend Growth

The time to keep our eyes peeled is early May.

Paychex (PAYX)

Dividend Yield: 4.7%

2025 Increase: 10.2%

Projected Q2 Distribution Announcement: Early May

Paychex (PAYX) is one of the world’s largest payroll companies, operating not just in the U.S., but also Europe and India.

It’s best known for providing payroll processing, employee payment and payroll tax administration services, but it also offers employee benefit administration services, human resources (HR) support, insurance services, and more.

Paychex has a longstanding dividend dating back to 1988, with a long history of “good behavior” from a Dividend Magnet perspective.

But Over the Past Year, PAYX Shares Have Lost the Plot

The drivers of this drop should be no surprise. As the job market goes, so goes Paychex, so investor fears of a “white-collar” recession have hammered PAYX shares.

Bottom-line growth did stall out in 2025, and in fact, earnings actually tapered off for the full year. But the top line continued to grow, and the company has still managed to exceed estimates over the past few quarters. Meanwhile, Wall Street is forecasting high-single-digit to low-double-digit earnings expansion for this year and next, so it’s possible the bear market in PAYX is more vibes than substance.

What’s more curious—and why I’ll be watching Paychex in early May, when it tends to announce its dividend increases—is its payout aggression. Last year, it hiked the dividend by a little over 10% … when doing so put its payout ratio above 85% based on 2025 estimates. It’s a little under 80% of 2026 targets, so a slowdown in payout growth would be a safe assumption anyways. But PAYX’s next dividend announcement could still tell us much about management’s confidence in the current employment environment.

Gaming and Leisure Properties (GLPI)

Dividend Yield: 7.0%

2025 Increase: 2.6%

Projected Q2 Distribution Announcement: Mid-May

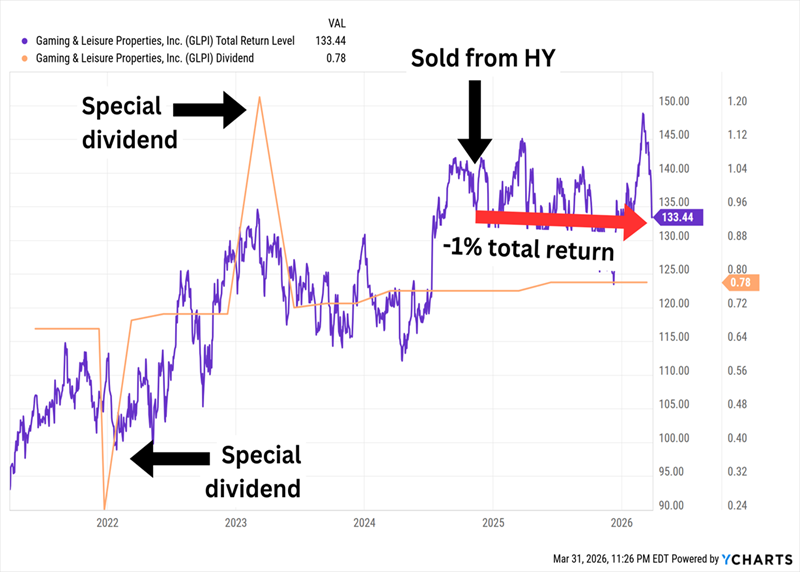

Subscribers to my Hidden Yields service might be familiar with Gaming and Leisure Properties (GLPI)—a casino and gaming REIT with 71 assets under brands such as Caesars Entertainment (CZR), PENN Entertainment (PENN), Boyd Gaming (BYD), and more.

Gaming and Leisure Properties stands out from other gaming names in that it has extremely little exposure to the hub of American casinos, Las Vegas. Its only Vegas chip was the Tropicana—which Bally’s knocked down last year. (However, GLPI still owns the land, which now is the site of an under-construction stadium for Major League Baseball’s Athletics). Instead, its land is spread across 21 states, from New Mexico to Ohio to Rhode Island.

We held GLPI for a little more than a year between 2023 and 2024 before collecting a tidy profit. And despite selling just as the Fed started cutting its target rate (generally good for REITs), the stock—even including its sizable dividend—has been just under breakeven since then.

GLPI Hasn’t Hit the Jackpot, But It Hasn’t Lost Its Shirt, Either

GLPI’s portfolio is well-diversified in the gaming space, and the company added to it in February with the $700 million purchase of Bally’s Lincoln (Rhode Island), which could offer additional growth. The dividend, meanwhile, is easily covered at 76% of adjusted funds from operations (AFFO) estimates.

We’ll likely see whether the REIT’s short five-year dividend-growth streak continues later this quarter, as its next dividend announcement should come in mid-May.

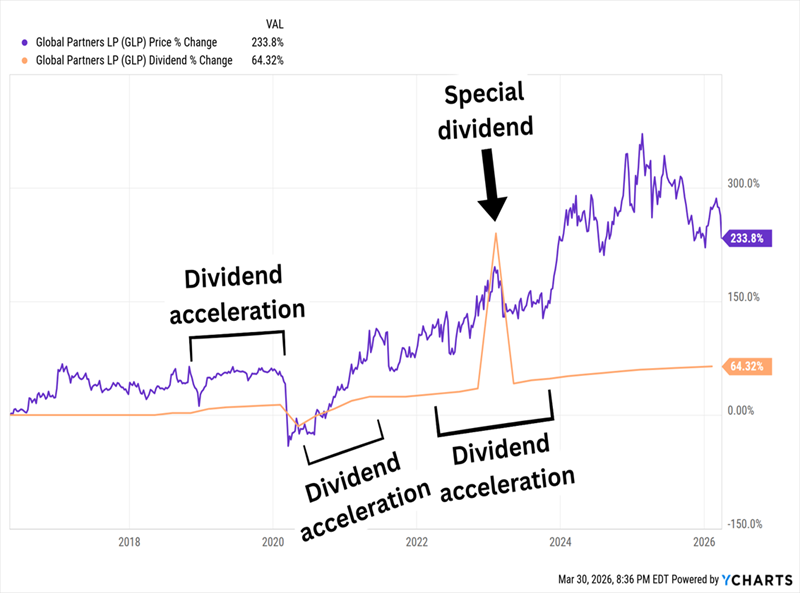

Global Partners LP (GLP)

Dividend Yield: 7.2%

2025 Increase: 5.0% (across four hikes)

Projected Q2 Distribution Announcement: Mid-April

If we drop the “I,” we get our final potential dividend raiser: Global Partners LP (GLP).

Global Partners LP is a smaller, niche energy midstream and downstream name that works in liquid energy terminals, fueling locations and “retail experiences.” It operates across five divisions: Commercial, which provides fuel to commercial and government customers; Wholesale, which delivers fuels to resale customers; Retail, which includes more than 300 convenience markets under the Alltown, Alltown Fresh, JiffyMart, and other brands; Terminals, which involves 55 owned and operated terminals; and Real Estate Ventures, which develops properties.

GLP is a brand that’s sure to feel at least some pinch—that is, rising fuel retail prices could hamper its Gasoline Distribution and Station Operations (GSDO), which likely were looking at a weak Q1 anyways given a worse-than-usual winter.

I’m curious to see whether a more difficult environment further slows an already decelerating dividend. Global Partners is a quarterly raiser, but the rate of growth has dwindled from 2 cents per quarter in 2023, to 1 cent in 2024, to half-cent hikes across 2025.

The Good News? GLP’s Previous Dividend-Growth Slowdowns Weren’t Permanent

Also, any improvement upon what is already a 7%-plus yield is certainly a welcome one.

5 “Dividend Magnets” Cut Through the Chaos

The Dividend Magnet is our guide in times like these. When external events drive a stock off its dividend-growth path, we contrarians know it’s time to pounce—because sooner or later, that Dividend Magnet will overwhelm investor panic and yank the share price back up.

It’s proven.

I’m high on 5 stocks with powerful Dividend Magnets that are poised for snap-back upside because their dividends simply keep marching higher—ratcheting up the pressure on their share prices as they do.

Their next big bounce could come any day, so the time to buy is now. Click here and I’ll give you a rundown on each of these 5 oversold income plays and a free Special Report revealing their names and tickers.