The year isn’t even four months old, and we’ve already been hit with three events that would normally send markets tumbling:

- The Iran conflict.

- The hit to software stocks, after AI raised concerns about their business model.

- The private-credit collapse.

We’re going to zero in on that third point today, because while the Iran situation is an ongoing tragedy, it will be resolved at some point. When it does, the relief rally will likely be significant.

The software story is similar. Over time, I see these stocks as winners in the AI race, not victims.

But the private-credit tale is different, because what it’s actually telling us about the economy—that it’s stable and growing—is the exact opposite of what most people think it’s saying.

That disconnect sets up equities for growth—including the equity-focused funds in our CEF Insider portfolio (which yield 9.9% between them). We’ll touch on one trading at a ridiculous 89 cents on the dollar in a moment.

Under the Hood of the Private-Equity Panic

Let’s take a walk through the private-equity situation so we can get a better sense of what it means for us as investors.

It actually ties back to the software situation, with the basic idea being that a lot of software firms borrowed from private-credit funds, which, as the name suggests, lend money directly to companies. And now that AI appears to be threatening software firms’ profits, the concern is that they could struggle to repay those loans.

This worry has caught on with the media. It even led a New York Times columnist to refer to it as “a slow-motion bank run” in an April 6 piece.

My take? That’s more than a little overdone. But we’re fine with that. Because whenever the media overplays its hand in a situation like this, the resulting panic sets up bargains for us.

The Data Doesn’t Support the Private-Credit Panic

To unpack this further, let’s look at the default rate in private credit, which stands at 5.8%, according to a recent measure taken by Fitch Ratings. Now we do need to note that Fitch only began taking this reading 2024. Since that’s quite new, we don’t have much history to compare it to.

However, Fitch also measures leveraged-loan defaults, which are very similar to private credit in their risk profile. The last reading saw that default rate at 4.9%, so not too far from private credit. But more important, it’s down sharply from the 5.7% rate seen in late 2025.

In other words, the risks in corporate credit are going down, not up.

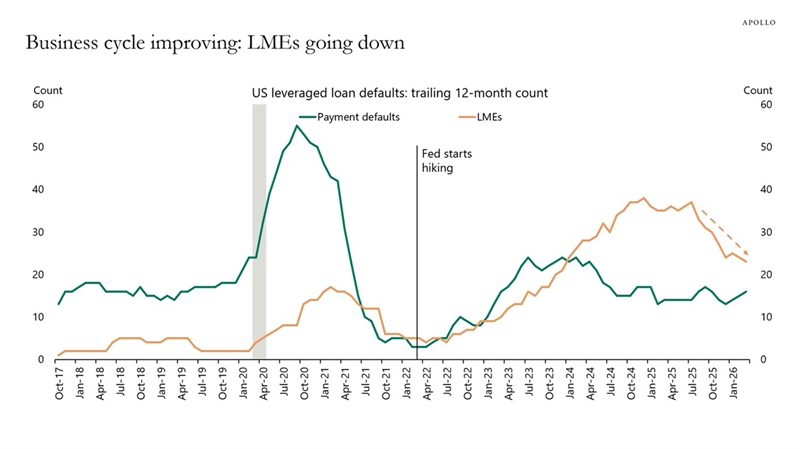

Apollo Global Management, one of the biggest players in private credit, has also pointed out that defaults on these loans have stayed pretty flat for two years now, and the default rates on “liability management exercises, or LMEs, are starting to come down, as well. Both trends are visible in the chart below:

LMEs are a way for a creditor and a borrower to work together to avoid a default or bankruptcy. The fewer of these there are, the better the credit situation for the marketplace as a whole.

And, as the orange line in the chart above shows, LMEs are fading after peaking in early 2025. That’s yet another sign the private-credit panic is overblown. Not only that, but taken as a whole, these indicators tell us the opposite of the panicky narrative we’re getting from the media: that the economy is not only stable—it’s getting better.

Of course, we’re not buying private-credit funds to take advantage of this disconnect. Many are structured badly, and some still have complications and subtleties that make them overvalued.

Instead, as I hinted at earlier, we’re looking to add to our holdings of funds in our CEF Insider portfolio’s equity bucket. We’re especially focused on those with overly wide discounts, like the Liberty All-Star Growth Fund (ASG).

Right now, ASG trades at an 11.2% discount—or about 89 cents for every dollar of its holdings—far below the 3.7% average discount it’s posted over the last five years.

ASG is also well-positioned because it not only holds large cap stocks—especially large cap techs such as Microsoft (MSFT), Amazon.com (AMZN) and NVIDIA (NVDA), but also mid-caps from across the economy, such as aerospace firm Curtiss-Wright (CW) and property manager FirstService Corp. (FSV).

That’s a diversified mix that nicely positions us to benefit as investors’ risk appetite picks back up. The healthy dividend—8.5% as I write this—doesn’t hurt, either.

Forget Private Credit: This Will Change Everything (in 18 Months or Less)

Most people know AI is going to affect pretty well everything about modern life.

But few people truly get just how deep these changes will run.

According to leading AI labs, the coming shifts will be far bigger than most people think. And they’re coming fast—we’re talking within 18 months here, at the outside.

We’re tracking this shift day by day at my CEF Insider service. And we’ve baked it down to 4 key drivers of dividends and upside in the near (and longer) term.

We’re buying into all of them now.

I call these 4 areas “pivot points.” And I’ve hand-picked 4 funds (paying 10% dividends on average) that are dialed straight into each one.

One pivot point, one fund. And a collective 10% dividend across all four.

All 4 of these funds are cheap now, as most investors have no idea what’s about to arrive. We do.