Think it’s a good idea to ask ChatGPT to run your retirement portfolio?

(I know that you don’t, my careful contrarian. But we both have friends that are more than tempted to trust the bots! Here are the cautionary numbers that show AI models are not very good at running money.)

A startup called Nof1 recently ran an experiment. It handed $10,000 each to Claude, ChatGPT, Gemini, Grok and four other leading AI tools. The humans gave “seed capital” to the bots.

Here’s $10K. You have two weeks to trade US stocks. Make some money. Now GO.

How much do you think each bot turned its initial $10K into? Well, whatever you’re thinking, go lower.

The broader “bot portfolio”—all of the money given to AI—lost a third of its capital. Down 33%. In just two weeks!

What’d they do wrong? Uh, just about everything. First, they overtraded. Second, they each took the exact same marching orders but went off in completely different directions.

Grok, Elon Musk’s AI product, was (would you believe it?) the “calmest” of the bunch. Grok placed “just” 158 trades over two weeks. Usually, trading like that is a reliable way to shred money. If you and I decide we’re going to turn up the frequency of our moves to 75+ per week, our trades will be suboptimal. To put it lightly!

And, to add to the confusion, the bots moved money with different biases. Yes, even the robots have predetermined blind spots. Claude (from Anthropic) tended to go long. Gemini (from Google) shorted stocks! And Qwen, a Chinese model, leveraged up because, hey, when you’re losing money why not borrow more of it? (When you’re taking poison, who cares how much? Ha!)

The bots blew up their portfolios because they thought they knew more than they did. They pulled historical data, identified trends that worked in the past, and concluded that the future would be the same. In other words, they built trading systems on the fly that looked great in the lab but fell flat on their faces in real life!

It’s the Mike Tyson school of hard knocks. Everyone has a plan until they get punched in the face.

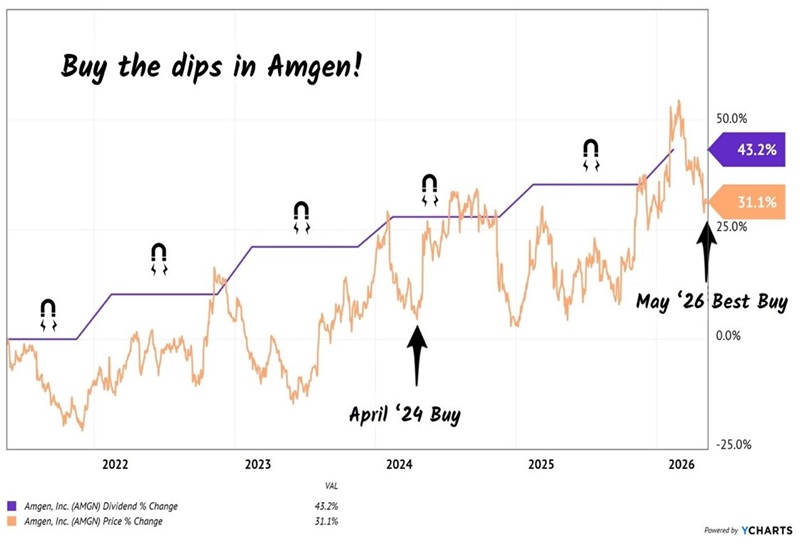

Eight bots took $10,000 down to $6,700 in two weeks — a pace that lands you at zero inside a year. Meanwhile, we contrarians have quietly compounded 30% on a blue-chip biotech the bots overlook. That stock is Amgen (AMGN).

The purple staircase below is Amgen’s dividend. The orange line is the share price, sometimes meandering but eventually racing to catch up with the dividend hikes. In April 2024, we bought the price dip and added Amgen to our Hidden Yields dividend growth service. Two weeks ago, we highlighted the latest dip as a Best Buy opportunity!

Amgen’s Divvie Magnet to the (Perennial) Rescue!

This is the powerful dividend magnet. Over time, a steadily rising payout drags the share price higher.

So, why can’t the bots model this? They can for short periods, but they lose focus. The robots draw too many conclusions, seeing patterns when they aren’t there—like reading tea leaves. They become too sure of themselves and fire off one thousand trades in a cool week or two.

We don’t need all that tail chasing. Amgen’s rising dividend is a surer bet than perceived (real but not repeatable) AI patterns. It is the cash cow of the biotech sector. The company boasts 70% gross profit margins, powered by a research engine that flows to the cash faucet.

Today, Amgen trades at 5-times sales. Compare it to NVIDIA, which runs on similar margins, but costs 22-times sales. NVIDIA is priced for perfection, which may continue to come true. But I’d rather bank the dividend-raising cash machine that quietly compounds without the “I hope earnings will be over the moon” type of drama.

Amgen also boasts a stock buyback machine that retired 29% of its share count over the past decade. Fewer shares to pay dividends on means more cash per remaining share, which feeds the next dividend raise, which feeds the dividend magnet. A virtuous cycle for us!

The growth engine underneath? Rare diseases. Amgen built its first fortune on pathbreaking red and white blood cell boosters for cancer patients, but its latest is a rare-disease segment. It didn’t have one just a few years ago. Then in October 2023, management dropped $27.8 billion on Horizon Therapeutics, the largest deal in company history. The prize: Tepezza, the leading treatment for thyroid eye disease, and a full rare-disease pipeline.

A disease may indeed be rare—have few patients—but put together breakthroughs and your combined revenues help people and… yes… your business.

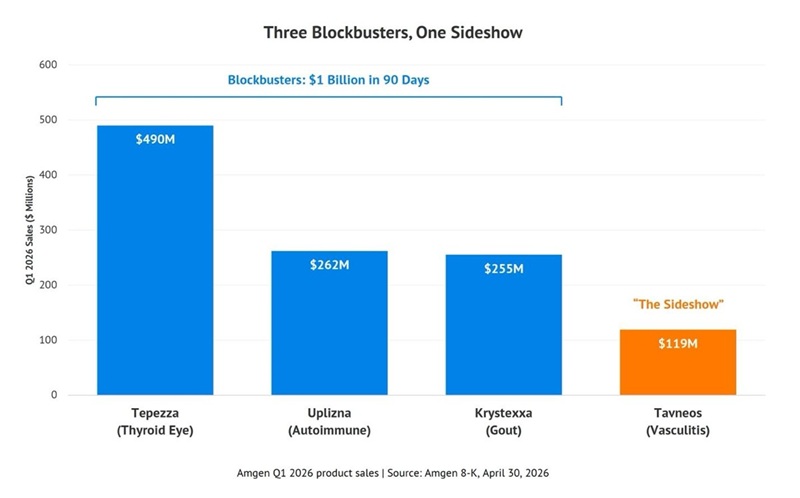

Of the more than 10,000 rare diseases identified today, only 5% have approved medicines, and Amgen has the R&D and manufacturing muscle to keep filling that gap profitably. Its Horizon acquisition bet is paying off. Amgen’s rare disease segment did $5.2 billion in revenue last year, growing 25% year-over-year in the most recent quarter. Tepezza alone brought in $490 million in Q1 2026.

Wall Street is waking up, but slowly (as always). Freedom Broker just upgraded AMGN to Buy with a $375 price target. That happens to be the exact buy-up-to price I raised for our Hidden Yields subscribers recently.

Nice of one suit to confirm our homework! There will be more rubber stamps on the way, as other shops still lag. BofA puts Amgen at $307. Guggenheim, $340. Morgan Stanley, $326. The full Wall Street average price target now sits around $357—above today’s price, but still short of where this dividend grower will land.

Earlier this year Amgen topped $388 but it has pulled back since over concerns about Tavneos, one rare-disease drug. True, this drug is a small revenue line, with $119 million in Q1 sales. But the forest for that tree? Amgen’s three rare-disease blockbusters—Tepezza for thyroid eye disease, Uplizna for autoimmune disorders, and Krystexxa for chronic gout—raked in over $1 billion. That’s 8-times Tavneos in 90 days. Uh, which do you think matters more?

Tavneos is a sideshow while the Horizon-era main act keeps humming. This presents us with a second-chance window to buy! The dip I flagged for HY subscribers two weeks ago hasn’t closed—yet. However, it’s likely only a matter of time because the dividend magnet keeps tugging. Let’s take advantage while the bots are frantically throwing trade tantrums!

Amgen is just one of many dividend magnets I track — and far from the only setup like it. The same pattern shows up across the dividend-payer universe: payout marching higher, price wandering before racing to catch up, Wall Street late to the party as always.

I just put my five favorite dividend magnet plays into a new research report, Yup, five stocks set up exactly like Amgen at our $280 entry point. Same year-after-year payout hikes. Same share price lagging the dividend. Same Wall Street suits asleep at the wheel.

The bots can’t find these names. The vanilla crowd misses them. We careful contrarians collect the dividends while the magnet does its work.

Click here for my 5 favorite Dividend Magnet stocks to buy right now. Yours free with a no-risk trial to Hidden Yields, my dedicated dividend-growth newsletter.