“Dad?”

The question came from two seats to my left. I leaned over and looked into my oldest daughter’s inquisitive eyes.

“Bolte is better than Judge?”

She asked it with a look of pure disbelief. A kid who’d just made a discovery but couldn’t believe her conclusion.

Last Friday night, my daughter had spent the first couple of innings parsing the center-field scoreboard, which lists each team’s batting averages. Henry Bolte, the Athletics’ 22-year-old rookie, had just pushed his average over .300. The shiny number jumped off the big screen at her, especially after I’d mentioned an inning earlier that hitting .300 is good. In fact, very good these days.

(Hitters batted .300 more often in ‘ye olde 1900s, before everyone started swinging for the fences, creating the home-run-or-strikeout-trying strategy. Which I find monotonous. Now get off my lawn.)

Aaron Judge, the anchor of the New York Yankees’ lineup, usually hits for average. And power. He’s a three-time MVP, last season’s batting champion (he had the highest average in the American League), and he usually slugs 50 or 60 dingers a year—as many as anyone in the game. Judge is a modern-day Babe Ruth.

Judge is, Roughly, Twice the Size of an Average Person

Right now he’s hitting .248, mired in a slump. Yet when Judge steps to the plate, the cameras come out and you can hear the opposing fans gasp. When Bolte steps in? Let’s be honest—nobody outside of Northern California’s A’s faithful has a clue who he is.

That said, we’re numbers people here at Contrarian Outlook. So let’s ask my daughter’s question out loud: is Bolte actually a better hitter than Judge?

Batting average measures how often a hitter reaches base safely on a hit. It’s a snapshot—one metric—but it doesn’t capture the totality of how much a hitter helps his offense score runs. Judge is a run-making machine. Bolte? We shall see.

My bet is that Judge will soon “hit his baseball card” and create more runs for his team this year than Bolte. Sounds obvious, perhaps—but consider the overrated number that many vanilla dividend investors chase: the big, shiny headline yield. The .300 hitter of Dividend Land! Big yield, good. Small yield, skip it.

But that yield doesn’t tell you the total-return picture for a stock—and total return is what matters when we buy a dividend stock. We want to lock in that yield and, at minimum, watch the price grind sideways. Better still if the price climbs, because then we bank gains on top of the dividends we collect. What we don’t want is a price that sinks while we pocket that dividend—that’s two steps forward, one step back.

It’s an expensive trap to fall into.

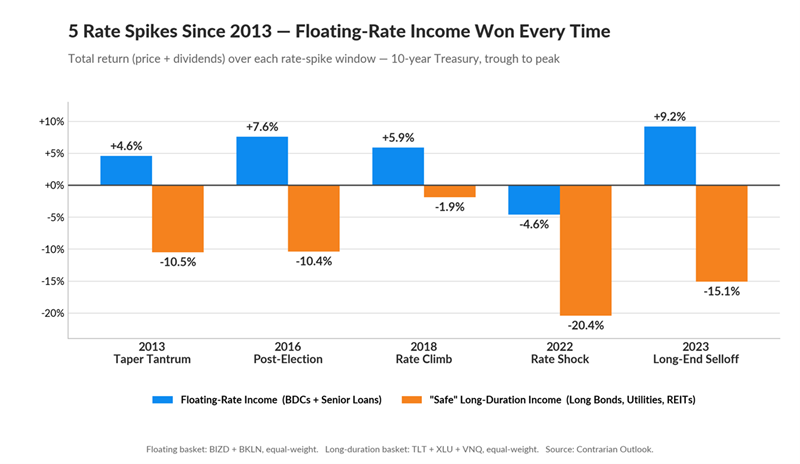

Here’s what’s happening on the investing field. The 30-year Treasury yield jumped near 5.2% last month—back near the highest levels the long bond’s seen since 2007. Long rates are climbing as stubbornly high energy prices keep near-term inflation sticky and Washington floods the market with fresh debt. But retirees stick with their headline-yield affinities and buy long-term bonds, utilities, and REITs (real estate investment trusts)—all “long duration” assets that lose value when rates rise.

Now, regular readers know my long-term call: AI is a deflation machine. Cheaper, faster, more productive—it pulls inflation, and eventually interest rates, lower. I haven’t budged. But “eventually” carries a lot of weight in that sentence. Rates don’t glide down a gentle ramp—they lurch. The road lower runs straight through spikes like the one we’re in now, and every spike clobbers long-duration income.

So I ran the numbers on every rate spike of the past dozen years—every stretch since 2013 where long-term rates jumped a full percentage point or more. Five of them. And the scoreboard is as lopsided as the game I took my daughters to. (Our Yanks hung four in the first, capped by a Goldschmidt three-run shot off Severino, and coasted to an 8-2 win. Much to the delight of the NY-based heckler behind me, who proclaimed “Goldy” a “great bleeping hitter.” This dad was not deterred by his preschooler in tow.)

Back to long rates, we’ve seen five spikes since 2013. Floating-rate income beat long-duration income all five times—by roughly 8 to 24 points each spike. The blue and orange bars below are blended baskets of popular floating and long-duration (fixed) income investments:

Look at the worst of the bunch: 2022, the ugliest stretch for bonds in 40 years. The floating basket dipped only 4.6%, while the long-duration basket fell about 20%. And that 20% average hid the real carnage inside it. The long bond alone—the “safe” bedrock of every retirement account—cratered about 37%.

The floating side? That 4.6% dip came with a raise: the payouts actually grew about 11%, because the loans inside reset higher as rates climbed.

So who earns income that rises with rates? We’re talking business development companies, or BDCs. Picture a BDC as a bank you buy on the stock exchange: it lends money to small and mid-sized American companies, mostly at floating rates. When rates jump, the interest it collects jumps—and the fat dividend it hands you holds up.

The one-click way to own the whole group is the VanEck BDC Income ETF (BIZD)—a single ticker holding the major BDCs in one basket, yielding about 9.3% today. As the bars show above, it beat the pants off popular income names the last five times long rates jumped like this.

For an individual blue-chip, my Aaron Judge is Ares Capital (ARCC), the largest BDC on the board—and at 10.1% today, it out-yields the basket while trading cheaper than usual thanks to some current hysteria in BDC Land. ARCC finished the entire terrible 2022 rate wipeout up 1.6%.

Main Street Capital (MAIN) is my other favorite floating flavor, paying 8.5%. MAIN doesn’t just lend money. It takes equity positions alongside its debt in many deals. That dual-engine structure is unusual among public BDCs—and lucrative.

In 2025, those equity stakes threw off $77 million in realized gains plus $150 million in fair value appreciation. That’s the source of MAIN’s monthly dividend growth and the periodic special dividends on top.

These are the run producers of the income world.

Now, BDCs aren’t magic or immune from pain. They lend to leveraged companies, and a long run of elevated rates eventually strains some borrowers. The one thing that breaks the BDC trade is a genuine wave of defaults—the kind that forces these lenders to mark down their loans and collect less interest. We sit nowhere near that today. But we watch credit quality like hawks. And as I said, I don’t expect rates to stay elevated forever.

My oldest now understands the difference between a batting average and a run producer. Will the investing herd, however, internalize the difference between long duration and floating-rate plays? If and when they do, we’ll have our positions first!

They’ll figure it out eventually, which means we contrarians need to buy the best payers right now. The optimal floating-rate plays, bought at the right time, throw off double-digit dividends that hold their value when rates lurch—the kind that can turn $500,000 into a paycheck you don’t outlive. Here’s the $500K retirement dividend playbook.