Last week’s selloff in AI stocks was painful for the mainstream crowd—and an opportunity for us contrarian income investors.

AI darling NVIDIA (NVDA) dropped 8.5% on the week. Others took bigger hits: Micron Technology (MU), for example, fell 16.6%.

The result? A chance for us to pick up our favorite AI-focused dividend funds on the dip—starting with one suddenly cheap “all-in-one” play from the portfolio of my CEF Insider service.

That would be the Columbia Seligman Premium Technology Growth Fund (STK), which holds key AI providers like Microsoft (MSFT), NVIDIA and Alphabet (GOOGL), as well as AI-infrastructure plays like Lam Research (LRCX) and Bloom Energy (BE).

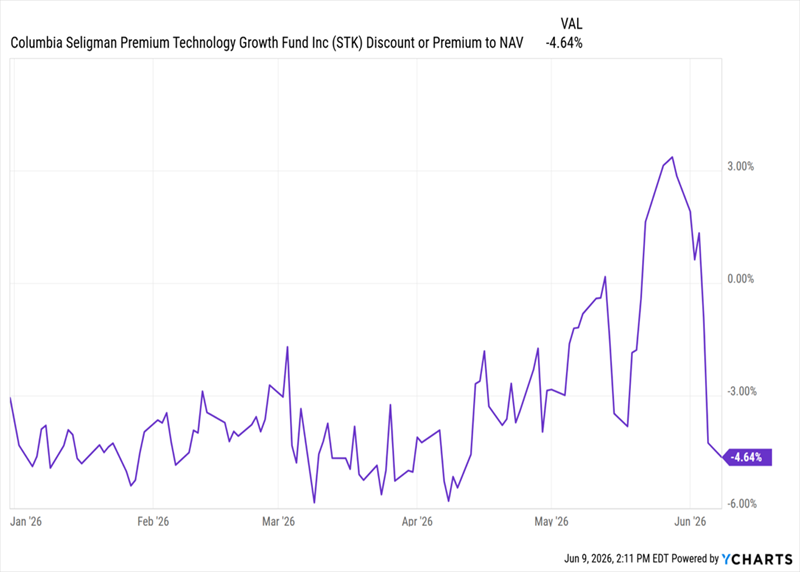

STK is on our radar now because the fund suddenly trades at a 4.6% discount to net asset value (NAV, or the value of its underlying portfolio), after averaging a 2.3% premium over the last decade.

And when I say this one is “suddenly” on sale, I mean it:

STK’s Speedy (and Likely Temporary) Drop Into the Bargain Bin

That’s a big decline for a fund that’s returned a hefty 42.8% for us since we added it to our portfolio in the November issue. I see that gain as just the start—and STK’s drop into discount territory as a brief “intermission” we’re going to take advantage of. Here’s why I say that.

Investors Sell Because the Economy Is … Too Strong?

Truth is, this latest stock-market selloff was not what most people thought it was. That’s because the reason behind it is, frankly, pretty wild: The economy is too strong.

The selloff came in response to the latest jobs report, which showed that the US added 172,000 jobs in May, nearly double economists’ expectations.

The logic behind that is as follows: If the economy is heating up, the Fed is more likely to hike interest rates. So stocks fell because higher rates weigh on their profits. Tech stocks are particularly rate-sensitive.

This all sounds straightforward enough. But there are some problems with this thesis.

For one, expectations of a rate cut had largely disappeared before the jobs report came out. In fact, talk of a potential rate hike was already in the air. All in all, the rate outlook didn’t change all that much after the report was released, so its effect on the overall state of play was pretty minimal.

So why, then, did stocks—especially tech stocks—pull back? The answer is straightforward: Investors were simply taking profits after the market’s strong run, particularly since the end of March.

They did this all at the same time for the same reason. With the blowout jobs report, a new narrative is about to take root in the press: Interest rates will rise, and stocks could suffer as a result. That will cause uncertainty and, as a result, higher volatility. Selling into that trend is a way to lock in profits.

But the savviest of these investors also unloaded some of their holdings (and again, tech holdings in particular) for a reason that means more to us: so they’ll have cash freed up to buy when the market gets overly panicky, as it always does.

These canny investors know (as do we!) that we’ve seen this movie before—not just in history, but just within the past few months!

On February 22, a firm called Citrini Research published a note on Substack warning of an impending economic collapse due to AI.

Investors used the fear created by that report to take profits, as well. But of course, that didn’t last long: All of these stocks had fully recovered by the beginning of April. And they probably would’ve recovered faster if the Iran conflict hadn’t begun on February 27.

So, what we have in front of us today is a case of history repeating itself. But of course, history never repeats exactly.

Here’s the twist: The February crash was based on Citrini’s view that over the next two years, corporations would see their profits surge as machines took over white-collar jobs. So we’d see a jump in unemployment due to AI.

In other words, just a single Substack post was enough to prompt investors to sell and take profits at that time. We’ve got a similar situation today, but for the opposite reason: Investors are selling because AI is creating jobs.

We’ve already seen many economists make the argument that “AI will create more jobs, not fewer,” as Apollo Global Management Chief Economist Torsten Slok put it.

Back in May—before the blowout employment report—Slok also noted that there is “zero evidence of AI-related job losses” and shortly after that documented the increase in new US businesses formed in part due to AI.

This is not a new position. Goldman Sachs made the same argument in 2023; MIT professor David Autor said much the same in 2024; and Stanford economics professor Erik Brynjolfsson said it again in 2025.

There are dozens more examples, but I’ll spare you the list.

That’s why we’re looking to CEFs like “suddenly cheap” STK today. Buying now locks in the fund’s (very well covered) 3.6% yield and sets us up for a second round of gains as mainstream investors realize their mistake and bid these AI stocks back up.

This idea—rotating into CEFs when they’re oversold and then selling when they’re overbought—is the heart of our CEF Insider philosophy, and a proven way to build wealth over time. And even if we have to wait for the next surge in our holdings, that’s fine, because we get a passive income stream while we do.

These 10% Payers Are Primed for AI’s NEXT Wave—and They’re Cheap (for Now)

Other top AI CEFs have seen their discounts widen in the last couple of weeks, too, and many of these funds offer much higher yields than STK, to boot.

In fact, the four funds I’m pounding the table on now yield a hefty 10% on average. They not only get us in on the Microsofts and NVIDIAs of the AI world at a discount—they target other non-tech companies primed to be supercharged by AI, too.

One of these funds, for example, holds the most innovative pharmaceutical companies out there.

As AI spreads through the drug business, it’ll slash development times, giving these companies years more of sales on their most profitable drugs before their patents expire.

We’re talking billions of dollars in extra revenue here—but our 13% (!) paying pharma fund is still off the radar, trading at a ridiculous 9.7% discount as I write this.

It’s the same story at our other 3 funds, all of which stand to gain from the coming “pivot points” in the economy as AI unleashes growth in surprising ways.

Click here and I’ll tell you more about these 4 “stealth” 10%-paying funds, including how each stands to gain on the ongoing AI buildout. You’ll also get a free Special Report revealing their names and tickers.